Online retail sales growth slowed in May following a fairly strong April

Insight

The Australian dollar has lost ground as China threatened to ban imports of Australian coal.

This coming and going, Is driving me nuts

This to-ing and fro-ing Is hurting my guts – The Rolling Stones

US-China relationship continues to deteriorate with US Secretary of State Michael Pompeo announcing the White House can no longer certify Hong Kong’s autonomy from China. Equity markets have taken the news on their stride with both European and US equity indices closing higher. Early in the session, news of an EU fiscal plan including €500bn in grants buoyed sentiment helping the AUD and NZD print fresh new highs. US China news along with an FT report suggesting China is going cold on Australian coal weighed on the AUD with NZD falling in sympathy.

“No reasonable person can assert today that Hong Kong maintains a high degree of autonomy from China given facts on the ground.” These were the words from US Secretary of State Michael Pompeo as he announced that the Trump Administration could no longer certify Hong Kong’s political autonomy from China.

Following last year’s passing of the Hong Kong Human Rights and Democracy Act, the law requires a yearly certification on Hong Kong’s autonomy. Pompeo’s decision open the door for possible tariffs on imports from Hong Kong, visa restrictions or asset freezes for top officials. China has previously warned it would retaliate if the US interfered in its affairs.

The news only elicited a small negative blip in equity markets with both European and US equity indices ending the day with solid returns, the S&P 500 closed +1.48% with main European equity indices recording similar gains. Off some note the IT heavy NASDAQ was a laggard up “only” 0.77% with tech shares showing a higher degree of sensitivity to the heightening in US-China tensions.

Risk sentiment was buoyed by the the European Commission (EC) fiscal stimulus proposal. Speaking before the European Parliament, EC President von der Leyen unveiled a stimulus plan worth up to €750bn made up of €500bn in grants to EU member states and €250bn of loans. Sources suggest that Italy and Spain would be the big winners, getting around €80bn in grants under the proposal The plan is not a done deal, being subject to agreement from all 27 EU members and will be discussed at the next summit on 19 June. The so-called “frugal four” – Austria, Denmark, the Netherlands and Sweden have previously disagreed that grants should be part of the package. After the announcement, the Austrian Chancellor said that “this is a starting point for the negotiations”, while Sweden’s EU Minister told reporters that his country won’t accept the plan as it stands.

ECB President Lagarde suggested that the euro-area economy is faring worse than hoped, with the recession looking as bad as the ECB’s more pessimistic scenario, with GDP growth set to fall by 8-12%.

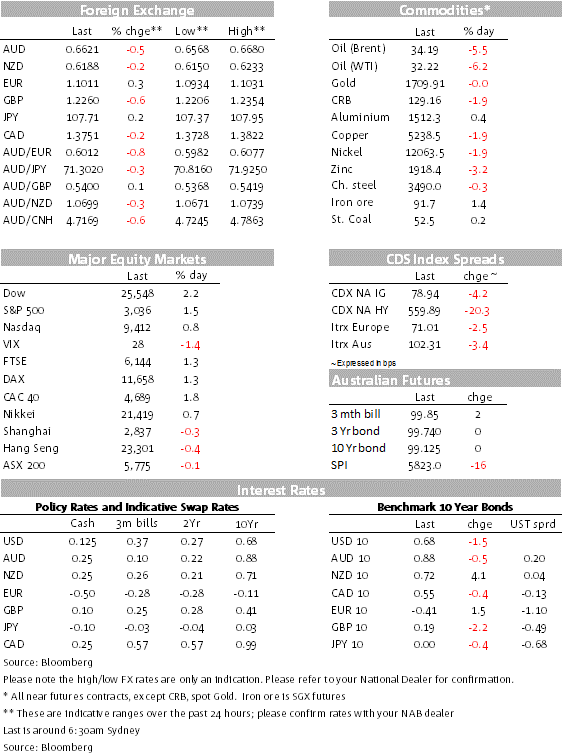

Unlike the rosy take evident in the equity market, the G10 FX performance reveals a set of mixed emotions from the overnight news. After breaking through range lows in BBDXY terms a day earlier, the USD experienced an up, down and then up again overnight price action ending the day marginally higher. BBDYX now trades at 1234.65 (+0.18%) and DXY is at 98.844, up 0.20%.

The Euro has been a marginal outperformer, up 0.10%, boosted by the EC fiscal stimulus news. The union currency rose as much as 0.5% to 1.1031, its strongest level since April 1, before paring its advance later in the session and now trades at 1.1006.

Late yesterday, the Aussie traded to a multi-month high of 0.6680 tracking the improvement in sentiment on the back of the stimulus news from Europe. But then the AUD fell over a cent to 0.6568 following the White House announcement on Hong Kong and a report from the FT suggesting China is expected to promote the use of domestic coal by tightening import rules, starting with shipments from Australia. Traders said China’s main state planning body, the National Development and Reform Commission (NDRC), had instructed five large state-owned utility companies not to buy Australian thermal coal. This report follows other signs of increased China-Australia trade tensions, with barley and meat exports under the spotlight. The buoyancy in the US equity market has played an infectious role on the AUD helping the pair recover a bit of ground over the past couple of hours. Over the past 24 hrs the AUD is down 0.74% and now trades at 0.6622. The NZD has followed a similar trading pattern to the AUD, reaching a fresh high of 0.6233 overnight, but it has since retreated back down to 0.6173, down 0.43% over the past 24 hours.

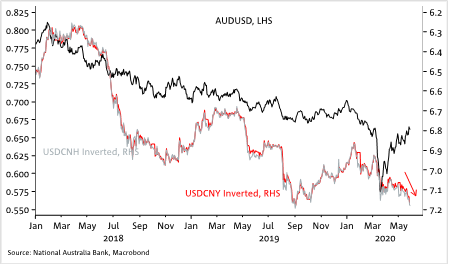

The US-CHINA news has also resulted in further weakness in the CNH and CNY. Looking at the overnight session, USDCNH traded to an overnight high of 7.1961, before regaining a bit ground to 7.18. Last year the during the US-China trade war, the introduction of US tariff coincided with CNY deprecation as the managed currency was allowed to lose ground against the USD, helping offset the negative impact form the tariffs. The market is closely watching whether Chinese authorities will allowed the CNY move above 7.20 as US-China relationship deteriorate again. As the chart of the day below shows, large CNY depreciation tend to be a headwind for the AUD (and NZD, but not shown in the chart)

GBP has also underperformed, not helped by the political scandal around Dominic Cummings, with calls for PM Johnson to sack his chief strategist after he broke lockdown rules. GBP is down 0.7% for the day to 1.2250.

Global rates are down slightly, reversing some of the upward pressure over the previous session, with the US 10-year Treasury yield down 2bps to 0.67%. The rate has climbed to as high as 0.73%, ahead of the White House announcement on Hong Kong.

NY Fed President Williams said that the FOMC was “thinking very hard” about targeting specific Treasury yields to keep them low, analysing how the policy has worked in other countries. The RBA’s yield-curve-control policy has been very successful, particularly when judged against the RBNZ’s QE policy. The RBA hasn’t needed to buy any bonds over the past couple of weeks to keep the 3-year rate at 0.25%, while the RBNZ is still near full-throttle, buying more than $1b of bonds per week, more than the government is currently issuing.

Oil is weaker after Russia looks determined to scale back on output reductions from July, in accordance with the OPEC+ supply agreement, according to sources. The market had been hoping that production cuts would be continued, given their success in holding up oil prices. Brent crude is down over 4% to USD34.50.

Big CNY/CNH deprecations tend to be a headwind for the AUD

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.