We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

US stocks have bounced back and the US dollar has picked up against the Yen.

https://soundcloud.com/user-291029717/china-helps-the-bounce-back?in=user-291029717/sets/the-morning-call

Risk sentiment stabilised overnight, helped along by the PBoC’s actions to stabilise the Yuan after it breached the “7” level on Monday. However, sentiment remains fragile and highly sensitive to trade headlines with Goldman’s the latest bank to “no longer expect a trade deal before the 2020 election”. Yields are little changed on net with US 10yr yields +0.3bps to 1.71%, gold has held at its six-year high, while oil is in a bear market with Brent now -21% from its April peak. Risk assets are more positive with stocks retracing some of their recent losses (S&P500 +1.3% to 2,882 after having fallen some -6.0% over recent days), while USD/Yen rose +0.5% 106.48. Other major currency pairs were little moved with EUR -0.1% to 1.12 and GBP 0.0% to 1.2161. Antipodean FX continues to trade with a weak tone with AUD -0.3% to 0.6760 and NZD -0.2% to 0.6529. There was only limited economic data overnight.

The PBoC helped steady the ship yesterday after the US Treasury designated China as a “currency manipulator”. The PBoC announced plans to sell 30bn of yuan bills in HK next week – draining liquidity and discouraging short-sellers in CNH, while it also set the CNY reference rate a touch stronger than some in the market feared (fixing 6.9683, but some feared something closer to 7). These were taken as signals that the PBoC was controlling the extent of downward pressure on the Yuan and that the “7” level was still a psychological level for the PBoC. Indeed, one could argue that while allowing the CNY to be slightly above 7 was intended as a warning signal to the US, Yuan stability is still a sacred cow for Beijing given the uncertainty a sizeable depreciation would bring. The PBoC played into that view noting China “has not used and will not use the exchange rate as a tool to deal with trade disputes”, and Bloomberg also noted that the PBoC convened a meeting with China-based foreign export companies and reassured them of its “consistent and stable” policy around the Yuan. This morning offshore CNH is 7.0538, down from yesterday’s high of 7.14; onshore CNY is 7.0198, down from a peak of 7.0585.

The US-China trade war though looks increasingly like it will be protracted. A number of banks have recently revised their outlooks with Goldman’s the latest to say they no longer expect a deal before the 2020 election. White House Economic Advisor said “the reality is we would like to negotiate” and they are still planning for Chinese negotiators to arrive in September. However, the sway of the moderates in the US Administration appears to be diminishing with reports from the Washington Post noting “Trump thinks that continuing to punish China will spur Beijing to negotiate. But some aides fear that his hard-line stance will backfire” and that “aides have brought Trump charts to convince him that the currency charge is untrue, but the president remains firm in his beliefs”.

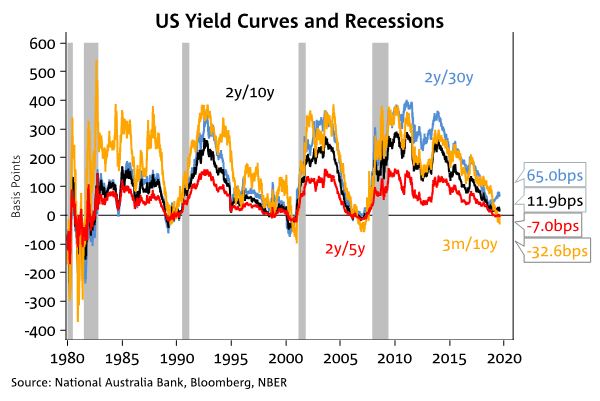

Fed’s Bullard (voter) tried to project an aura of calm overnight by noting “US monetary policy cannot reasonably react to the day-to-day give-and-take of trade negotiations” and that “particularly threats or counterthreats are only a manifestations of already high trade regime uncertainty”. From the remarks it is clear though that Bullard supports another rate cut, but is waiting to see how the economy may react to the uncertainty while also waiting for the effects of previous monetary policy easing. Bullard also made a few observations on the yield curve, noting “the slope of the yield curve contains important information for monetary policymakers” with anticipation of Fed easing preventing an “intensification of the yield curve inversion so far”. The key 3m/10yr curve though has been inverted for some time, which we at NAB have been taking as an amber warning for a US downturn over the next 10-18 months.

In FX, CAD was the biggest mover with USD/CAD +0.7% to 1.3274 as the market played catch-up to recent events after a public holiday. The recent outperformance of the Loonie relative to the Aussie is notable with both economies having similar headwinds to trade and Canada’s exposure to the oil price – will this outperformance be sustained? The other significant mover was USD/YEN +0.5% to 106.48 with some easing in risk aversion overnight.

Ahead of the RBNZ today, the NZD sits around 0.6527, losing its gains overnight from the stronger than expected labour market data yesterday (unemployment rate was 3.9% against 4.3% expected).

There was little economic news overnight with only German Factory Orders beating expectations at +2.5% m/m against 0.5% expected.

Yesterday the RBA kept rates on hold, but adopted a more explicit easing bias as well as reiterating recent forward guidance. The important last paragraph concluded “It is reasonable to respect that an extended period of low interest rates will be required in Australia’….and “will continue to monitor developments in the labour market closely and ease monetary policy further if needed”. There was little elaboration on the recent intensification of trade tensions, but we would expect the Governor to talk more about this when he testifies before the House Economics Committee on Friday morning (9 August 9.30am AEST). NAB still expects the RBA to cut rates again by November, with risks of an earlier move driven by labour market developments, whether recent tax cuts feed through to spending, and the state of the global economy.

Finally, yesterday Australia recorded another record monthly trade surplus at $8.0bn against $6.0bn expected. The record surpluses over Q2 suggests Australia may post its first current account surplus since 1975 (note the quarterly trade surplus was $19.7bn, while the net income deficit in Q1 was $16.5bn), though it is unclear how long such a current account surplus will last given iron ore prices have retreated from their multi-year high. The quarterly figure should also see the trade surplus make a small contribution to Q2 GDP.

The RBNZ meeting today takes top billing where a rate cut is fully priced by markets. There is also a smattering of mostly second-tier data including Australian Housing Finance, BoJ June Minutes, China Foreign Reserves, and German Industrial Production. There is also one US Fed speaker scheduled – Evans (voter, dove) who will be hosting a breakfast on the economy with Q&A.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

Economic and financial market update

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.