NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

There are reports the US Treasury Department will no-longer consider China a currency manipulator.

https://soundcloud.com/user-291029717/china-cured-of-currency-manipulation

Take you pick as the inspiration for today’s title from either the Queen’s endorsement of her youngest grandson’s wish for a more independent family life or the reports that the United States Treasury will drop China’s ‘currency manipulator’ designation – as vacuous as this is – ahead of the formal signing of the Phase 1 US-China trade agreement on Wednesday.

It’s been a ‘risk on’ offshore session, the S&P 500 currently trading above last Thursday’s record closing highs (+0.6%) benchmark bond yields higher in the United States and Europe (ex-UK) and commodity/growth linked currencies all up on Friday’s New York close, albeit AUD and NZD are both back a little from where we left them last night.

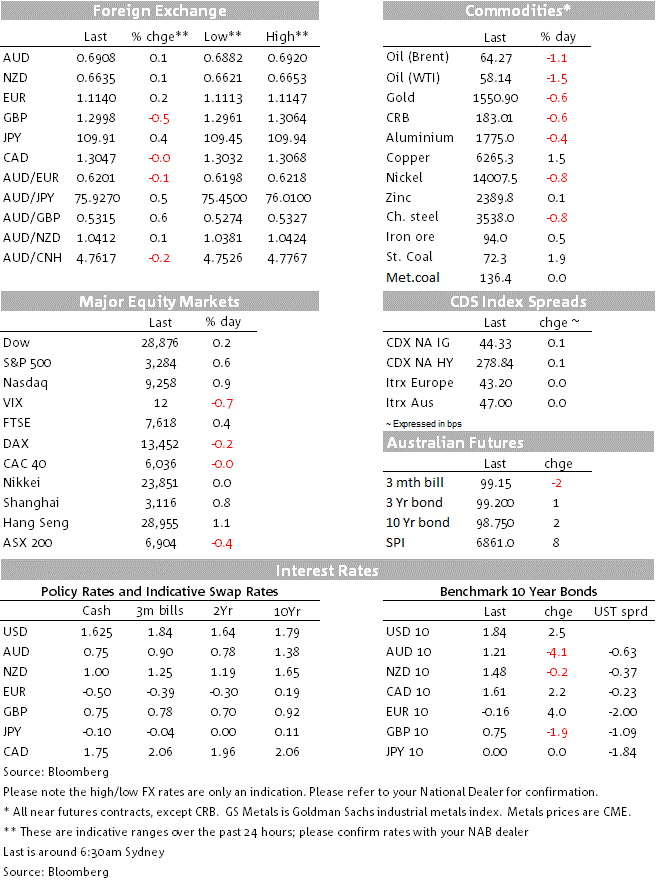

Probably key to the good showing of the Aussie and Kimi so far this week has been the strengthening in the Chinese Yuan alongside broader EM FX gains and where the drop in USD/CNY to just below 6.90 during our time zone on Monday has slightly extended offshore (USD/CNH down to 6.88). At just above 0.69 (0.6909 now) AUD/USD is bang in the middle of our ready reckoner ‘tram lines’ that relate the level of the CNY to the AUD. At the same time, AUD continues to trade well to the low side of fair value estimates linking it to interest rate differentials, commodity prices and risk sentiment. So too is the NZD and to a much greater extent, but this now been the case for six months or more, validating one of John Maynard Keynes’ most famous adages, viz that ‘markets can remain irrational longer than you can remain solvent.’

Sterling and the Japanese Yen has been vying for the wooden spoon in the G10 FX league table, GBP currently owning the dubious pleasure. Yesterday’s FT interview with MPC member Gertjan Vlieghe in which he indicated he would vote for a rate cut on January 30 if the economic data did not show signs of a post-election recovery in the interim – he cited survey (PMI) data in particular – took at a bite of GBP at our open yesterday. Losses have since been compounded by very poor November GDP and industrial production figures (-0.3% and -1.2% respectively), albeit pre-dating the Dec 12 UK general election.

JPY weakness, that has seen USD/JPY have a look up at ¥110 (109.94 high) and AUD/JPY just above ¥76 (76.01) is fully consistent with better risk sentiment and higher US treasury yields, where 10 the 10-year noire is 2bop higher at 1.84% and 2s +1bp to 1.58%. Eurozone benchmark 10-year bonds earlier rose by between 3 and 5bps, but equivalent UK gilts 2bp lower on heightened expectations for lower policy rates and where a January 30 25bps BoE cut is currently priced at close to 50% versus nearer 25% on Friday.

The German press has reported that Germany ran a budget surplus of some €13bn last year, that’s the equivalent of 3.5% of GDP, highlighting just how much scope Europe largest economy, currently in virtual recession – has to stimulate its economy without having to abandon its so called ‘Schwartz null’ (black zero constitutional ban on running budget deficits.

Oil prices have continued to fall back, Brent crude off another 70 cents or more than 1% to $64.26. Base metal are mixed with copper up 1.5% and Tin almost 1% but aluminium, nickel and lead down, while iron ore is up 0.5%. Gold has lost another $12 to be just back below $1,500 after briefly spending time above $1,600 at the peak of the military aggression between the U.S. and Iran last week.

Weekly ANZ-Roy Morgan consumer confidence will get closer scrutiny than usual at 9:30 ET as analysts continue to grapple with the extent to which the economy is being hurt by the bushfires and after last week’s reading came in at the lowest since mid-2014

NZ has the QSBO survey which should reveal a significant lift in business confidence, as the timelier ANZ survey showed at the end of last year.

China trade figures for December are due at some stage today (time not given) with the market consensus looking for a rise in both exports and imports in yr/yr terms versus the -1.3% an 0.3% recordings for November – to +2.5% and 9.6% for exports and imports respectively.

US CPI is expected at 0.2% in ex-food and energy terms, for an unchanged 2.3% yr/yr change.

US earnings season kicks into gear tonight with JP Morgan, CitiiGroup and Wells Fargo all reporting prior to the NYSE market open. The FT notes analysts and investors are travelling with hope with corporate America will report its first quarter of earnings growth since the end of 2018. It quotes Goldman Sachs figures that 92% of the S&P 500’s market’s appreciation in 2019 came from multiple expansion not earnings (largely a product of the flood of liquidity represented by the Fed’s three quarter point rate cuts).

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Confidence and Conditions Lift

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.