Total spending grew 0.9% in June.

US equities are on the rise again driven by a flurry of M&A activity, alongside vaccine hopes and reasonable activity numbers from China.

https://soundcloud.com/user-291029717/china-shops-rba-waits-fomc-meets?in=user-291029717/sets/the-morning-call

“There’s a place for us; Sitting here, waiting for the sun; And it calls me back; Into the safe arms that I know”, Powderfinger 2001

With the S&P500 +0.5% as the tech rally continued, boosted by M&A activity (NASDAQ +1.2%). Helping boost sentiment was Chinese activity data yesterday which showed momentum picking up amongst Chinese consumers, while the industrial sector has moved beyond recovery and into real growth (YTD y/y now +0.4%).

The lack of progress on another US fiscal package continues to be ignored. There was also little reaction to other news flow or data ahead of the FOMC today – slightly weaker than expected US industrial production was largely ignored as was a WTO ruling that found the US violated trade rules when it imposed tariffs on China in 2018.

Markets are clearly waiting on the FOMC for direction with little movement in bonds with US 10yr Treasury +0.7bps to 0.68% apart from a slight bear steepening (10s30s +2bps), while G10 FX on net was little changed with the USD DXY +0.0%.

There’s a risk the market is underwhelmed by the guidance provided by the Fed. There is some expectation that with the US Congress unwilling/unable to agree to a new fiscal package, monetary policy may need to step in to fill the void. Accordingly markets will be focused on any changes to forward guidance and to any balance sheet adjustments.

We’re doubtful the Fed would signal a near-term increase in the pace of Treasury buying and instead the Fed’s focus will be on communicating the adoption of its “average” inflation targeting regime, where we expect Chair Powell to be pushed on what exactly that means for the outlook for rates.

Expectations of a technical adjustment to IOER have also mostly faded too amongst market participants. New projections will also be published that should show most participants see rates on hold through 2023 with one or two dots perhaps pencilling a hike further out.

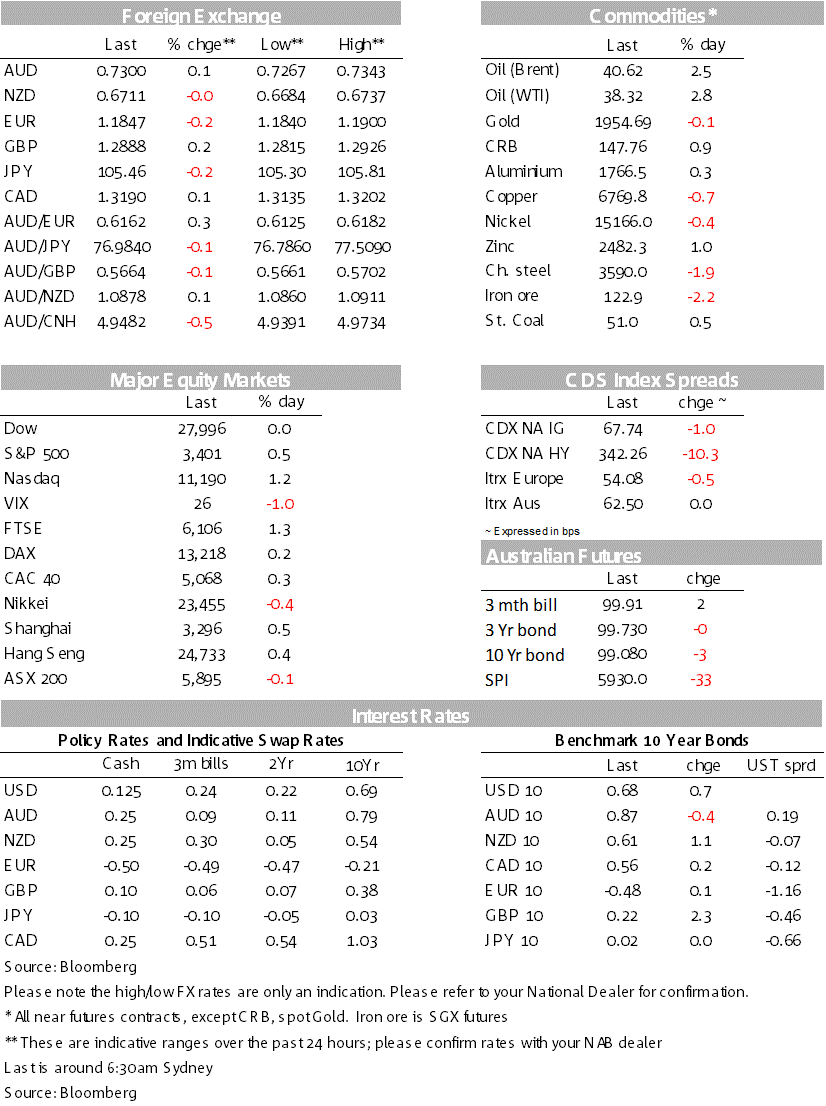

Major G10 FX was little changed on net (USD DXY +0.0%). The AUD and NZD gave up most of yesterday’s gains to finish little changed over the past 24 hours. GBP recovered a little, up 0.2% to 1.2888 and largely unperturbed that the internal markets bill got through its first reading in the UK Parliament yesterday.

Helping somewhat was the more moderate language used by the PM, stating the powers of the bill “are an insurance policy, and if we reach agreement with our European friends – which I still believe is possible – they will never be invoked”, and adds to the view the recent developments have been about brinkmanship as negotiations come to ahead by October 15.

Particularly CNH with USD/CNH -0.4% to 6.7787 and the strongest since May 2019. Helping drive CNH overnight and broader risk sentiment was the Chinese activity data for August which was much stronger than expected across the board.

Retail sales growth picked up with the y/y number in positive territory for the first time since the pandemic began (+0.5% y/y v 0.0% expected), while the monthly seasonally adjusted number suggests there has been a step-up in the pace of retail sales growth (1.3% m/m, up from 0.6% in July). Starbucks also reported its same store sales growth in China, suggestive of stabilisation with flat same store sales growth flat in August after a 10% fall in July.

Industrial production also remained strong (5.6% y/y v 5.1% expected) and the YTD y/y at +0.4% suggests the industrial sector has now moved beyond the recovery phase. Fixed asset investment also beat (-0.3% y/y v -0.4% expected). Given the recovery the PBoC seems to be showing more tolerance for a stronger currency with the CNY fix yesterday at 0.6882.

The RBA Board Minutes repeated the easing bias from the September meeting, though gave little hint on what it could do. There was only slightly more dovish commentary around the currency (“broadly aligned with its fundamental determinants”, but “a lower exchange rate would provide more assistance…”) and the supply of credit (“tightened somewhat”). The Minutes though did repeat the dovish post-meeting Statement line of “the Board…continues to consider how further monetary measures could support the recovery”.

That dovish line and a recent AFR article has re-ignited speculation that the RBA Board “is” actively considering what more it could do. Unfortunately the Minutes did not shine much more light on that debate.

The AUD initially rose on the news to a high of 0.7343, but reversed those moves overnight to end at 0.7300.

The RBA could announce additional QE for 5-10 year bonds (government and semi) and this could limit steepening pressure on the curve from government debt issuance. The RBA could reduce the cash rate to 10bps (from 25bps), though the impact would not be great apart from also flowing onto the 3yr YCC target and the TFF as the cash rate is already trading close to this level.

NAB’s view remains the RBA will keep the cash rate and 3-year yield target unchanged for the foreseeable future, though should the RBA wish to ease policy further there is a potential to extend the yield curve target or adopt a more formal bond purchase program to push long dated yields lower.

Vaccine news remains positive with the UAE giving emergency approval to China’s Sinopharm vaccine which it has been testing since July (see link). While details of those phase 3 trials are yet to be published, there had been “no severe side effects” amongst the 31,000 participants.

A quiet day domestically with most international focus on the FOMC Decision and on US Retail Sales:

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.