Online retail sales growth slowed in May following a fairly strong April

Insight

China reported disappointing import numbers at the close on Friday.

https://soundcloud.com/user-291029717/us-share-hit-highs-china-trade-slows-earnings-season-kick-offs?in=user-291029717/sets/the-morning-call

I don’t like cricket oh no, I love it – 10cc

Having risen at 4am and caught the final acts of both Wimbledon and the Cricket World Cup, I was completely exhausted by 4.30am; coming it to write about markets seems almost trivial. Fiction writers couldn’t have credibly made up the finale to the CWC. Commiseration to the Black Caps – a hand each on the trophy would surely been a more fitting end, wouldn’t it? But to borrow from the great Sir Alex Ferguson: “Sport – bloody hell’.

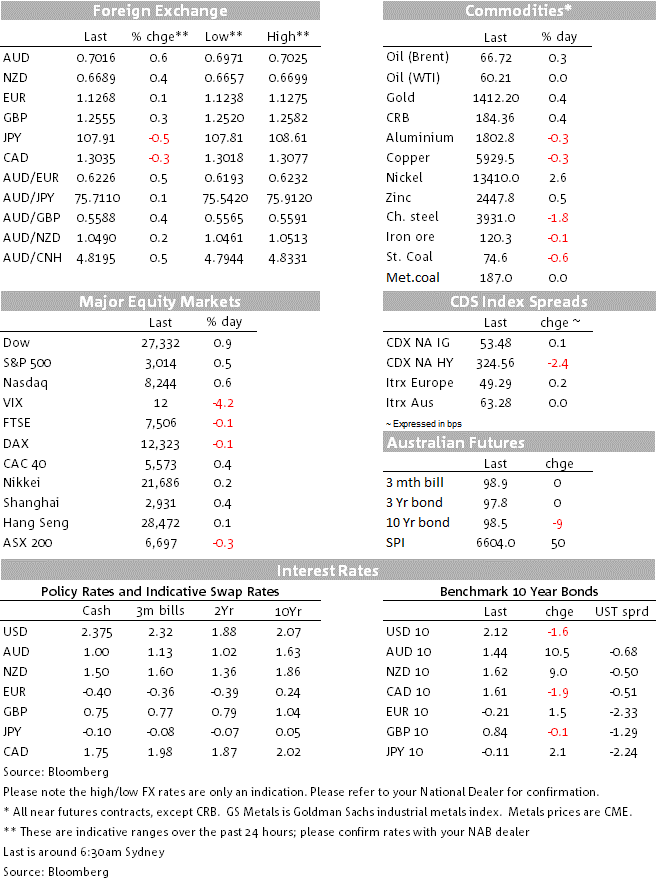

As for markets at the end of last week, all three major US equity indices posted new old time highs, the S&P 500 finishing above 3,000 for the first time ever (+0.5% to 3,014). And while US 10 year bonds – to which equities and currencies have proved ultra-sensitive of late – were up over 5bps last week, both 2 and 10 year Treasuries ended Friday 2bps down on the day (and 2s -1bp on the week). It’s the supreme market confidence the Fed will cut rates on July 31st that continues to drive stocks higher and where the US money market ended Friday still ascribing about a 25% chance to an end-month Fed move being 50bps rather than 25bps (and so flagging the risk of some minor disappointment assuming a cut is a ‘mere’ 25bps, as NAB expects)

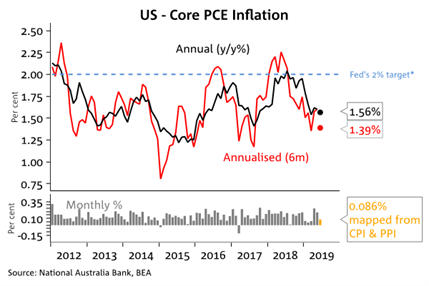

Lower bond yields Friday came despite an upside surprise to US producer prices, where the core (ex-food and energy) measure rose by 0.3% against 0.2% expected, the same as happened with CPI earlier in the week. But as illustrated in the ‘Chart of the Day’ below, mapping latest CPI and PPI data through to the more important – Fed targeted – core PCE deflator suggests we shouldn’t be expecting the latter to follow suit. Core PCE is still seen tracking no stronger than 1.6% and on a six-month annualised basis, less than that.

This is important for whether the Fed enacts just a couple of ‘insurance’ cuts against a deeper economic downturn between now and the end of the year, or has to keep going to re-enforce its determination to get inflation up to – and ideally up through – its 2% target, if this measure of inflation still isn’t showing much of a pulse come year-end.

Incidentally, the rise in PPI in June was driven entirely by services, with a particularly large rise in ‘portfolio management services’. Financial services prices in general can be highly volatile the way they are measured and arguably shouldn’t form part of a true core measure of inflation. But the latter, as reported, exclude only food and energy of course.

Fed-speak on Friday came from Chicago President and FOMC voter Charles Evans, arguing for more accommodation: “Inflation is probably going to require a little more monetary accommodation in order to get up to 2, and above 2” percent, Evans said Friday during a talk in Chicago. “I really think that it would be useful, it ought to be a part of our policy, to be aiming for inflation a little bit above 2% at this point, because we’ve been under-running for so long.”

“I think that with a couple of rate cuts, the trajectory for inflation could be looking like 2.2% PCE inflation in 2021, and that would be a perfectly acceptable, good outcome,” Evans said.

Ahead of today’s China Q2 GDP and June activity readings (see below) we had a couple of important China releases soon after the Australian market closed on Friday. The June trade data disappointed in so far as annual import growth came in at -7.6%, up from -8.5% in May but worse than the -4.6% expected. And export growth fell into negative territory, at -1.3% from +1.1% in May albeit this was 1/10% better than expected.

The AUD didn’t move on the trade numbers, but benefited slightly soon thereafter from the June China credit data that showed a better than expected rise in the broadest measure of credit – Aggregate Social Financing. This was ¥2.26bn up from 1.395bn in May and 1.9bn expected.

In FX AUD ended up as Friday’s best performing currency, +0.7% to a high of 0.7025 and NY close of 0.7020. The NZD was not far behind, +0.5% to within a whisker of 0.67 (0.6695 close). Ironically, these two risk/global growth sensitive currencies fared just about the same as the ‘safe haven’ CHF and JPY, each of the latter +0.6%. Broad based USD slippage was the main story Friday, alongside US yield declines (though there was also a bit of direct EUR/USD support drawn from better than expected Eurozone industrial production figures – up by 0.9% against 0.2% expected, albeit flagged earlier in the week by those very strong French numbers).

There is also heighted chatter about the possibility of the US intervening in the FX market to try weakening the greenback – something to which we ascribe very low odds but is being written back by several of the big US banks. Whether it was a factor on Friday is questionable, we rather think not.

China’s Q2 GDP and June activity readings take centre stage at the start of a week that also features latest Australian labour market data (Thursday) and June RBA Minutes (tomorrow); New Zealand CPI, US retail sales and industrial production (Tuesday); Fed Beige Book (Wednesday) plus the first consumer sentiment readings for July (Friday).

China GDP growth is expected to have slipped to 6.2% from 6.4% in Q1. For the monthly numbers, industrial production is usually the headline grabber (it certainly was last month when annual growth fell to 5%). A small rebound (to 5.2% is the consensus. Retail sales are seen having edged down to 8.5% from 8.6% and Fixed Asset (urban) Investment seen unchanged at 5.6% in YTD y/y terms.

The US earnings season kicks into gear today, with Citigroup reporting before the US market open. Notable household names reporting this week include JP Morgan, Wells Fargo, Goldman Sachs and Johnson & Johnson (all Tuesday); Alcoa Netflix and BAML (Wednesday); Microsoft and Morgan Stanley (Thursday).

Offshore the first of the regional PMIs for July comes courtesy of the Empire (NY State) survey. Remember this slumped in June with Trump’s threat to impose tariffs on Mexico seen largely to blame. So will it strike back this month?

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.