Total spending grew 0.9% in June.

US shares were doing well ahead of the news that trade talks would resume between the US and China next week.

https://soundcloud.com/user-291029717/bojo-wins-china-trade-talks-next-week?in=user-291029717/sets/the-morning-call

If leaving me is easy, and you know, coming back is harder- Phil Collins

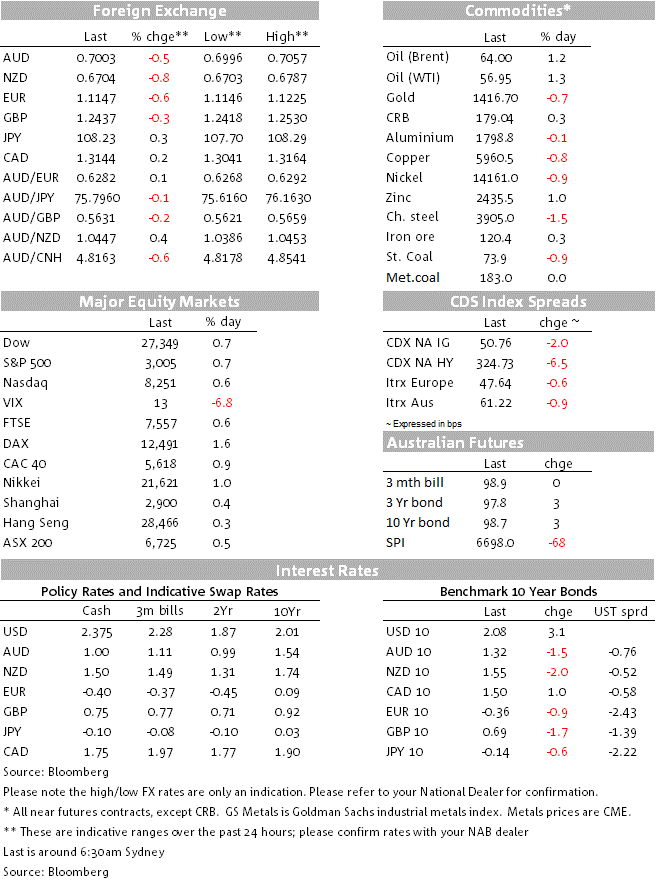

Solid earnings reports along with news that the US and China will have face to face trade talks next week Monday boosted US equities and lifted UST yields after the latter were temporarily weighed down by a soft Richmond Fed Survey. The USD has continued its broad ascendency with the NZD and AUD underperforming along with other G10 pairs. Boris Johnson will become the UK’s new Prime Minister and promises to deliver Brexit. After a brief uplift, GBP ends the day lower.

After a slow start, US equities were lifted by a strong end to the European session, a trio of solid earnings reports from Coca-Cola, Lockheed Martin and United Technologies and positive US-China trade news. Early in the overnight session, European equities were aided by solid earnings reports from UBS, Santander, Hermes and AMS, helping the Stoxx Euro 600 index closed the day 0.98%. Later in the NY session news that US Trade Representative Robert Lighthizer will head to China next Monday for a first face-to-face high-level US-China trade talk since Presidents Trump and XI agreed to resume negotiations late in June, boosted market sentiment and helped the S&P 500 move back above 3000 mark. The S&P closed 0.68% higher and the NASDAQ ended the day at 0.58%.

US Treasury yields ended the day higher after a small wobble around midnight courtesy of a very soft Richmond Fed survey revealing a 14 point drop to -12 against market expectations for a 3 point rise to +5. So far we have quite a mixed picture from the US regional manufacturing surveys, in July the Philly Fed survey soared, the NY Empire State index was steady and overnight the Richmond Fed tanked. The Chicago PMI is the next regional survey to watch, but so far the mixed regional picture means correctly predicting the ISM July reading is going to be a pretty difficult task. That being said, after the US-China trade news, UST yields ended the day higher with a mild steeping bias. The 2y rate gained 2.1bps to 1.834%, the 10y tenor climbed 2.5bps to 2.077% and the 30y bond rose 3.4 to 2.606%.

In FX land, the USD remains the big story continuing its ascendency which began on Friday last week. The DXY index now trades at 97.702, 0.47% higher on the day while BBDXY is 1199.34, up 0.4%. Higher UST yields overnight were one supporting factor while EUR weakness was another. The union currency has a big weight in USD indices (57.66% in DXY), thus its 0.53% decline over the past 24 hours has been one big factor for the rise in USD indices. Since early June, the 1.12 area has proven to be good support for the euro, but ahead of the ECB meeting on Thursday, the euro has now broken below 1.12 and trades at 1.1152. Focus today will be on the European July Flash PMIs ( see more below).

After being a big winner last week, the NZD has struggled with the turn in USD fortunes over recent days. The Kiwi has been one of the big underperformers over the past 24hrs, down 0.81% and now trades at 0.6704. AUD has also struggled (-0.47%) and after briefly trading at 0.6996 overnight, the pair is back above the 70c mark currently trading at 0.7004. Meanwhile the CAD has been the best G10 performer, only losing 0.15% against the USD, helped by another solid night for oil prices ( up around 1%).

GBP is down by only 0.2% to 1.2450, coming to little harm from Boris Johnson winning the Conservative party vote to become the new UK Prime Minister, with the result widely anticipated. Johnson won twice as many votes as Jeremy Hunt. His acceptance speech reiterated his goal of getting Brexit done on 31 October. His grip on power will be weak, given the status of a minority government and a number of Ministers immediately resigned following the announcement. In our view, Johnson’s desire to push for Brexit, deal or no deal, increases the chance of an early general election and some possibly nasty GBP outcomes.

In other overnight news, the IMF nudged down its global growth forecasts by 0.1% to 3.2% for this year and 3.5% next year, making 2019 the weakest since the GFC in 2009. It cited adverse developments including further US-China trade tariffs, US auto tariffs, or a no-deal Brexit that “sap confidence, weaken investment, dislocate global supply chains, and severely slow global growth below the baseline”.

Lastly tensions in the East China Sea is another geopolitical theme that we may need to keep an eye on. Late yesterday South Korean fighter jets planes fired warning shots at Russian planes. Russia has confirmed that it has carried out its first ever joint air patrol with China in the region, sending a very strong signal of a the developing military relationship between Moscow and Beijing. Japan has also protested both to Russia and South Korea over the incident.

Our BNZ colleagues expect an 8% growth in exports and a flat result for imports. This would generate a slight surplus of $NZ0.1b, trimming the annual deficit to $NZ5.1b.

Today’s data releases are expected to confirm both Germany and EU manufacturing activity remained in contractionary mode in July. The market is looking for the German manufacturing PMI to print at 45.2 vs 45 previously whilst the EU reading is seen at 47.7 vs 47.6 in June. France’s manufacturing activity has been the outperformer in recent months and more of the same is expected in July with its manufacturing PMI expected to remain in expansionary mode at 51.7 vs 51.9 prev.

Meanwhile, after drifting down to 51.2 in December last year, Europe’s services sector is expected to consolidate its move above 53 ( 53.3 exp. vs 53.6 prev.). If the data prints as expected, then the ECB could argue that whilst it is watching the EU economy really closely there is still no evidence that the manufacturing recession is spilling over to the broader economy.

Markets are slowly but surely paying more attention to the US PMIs, although the ISM readings are still the key ones to watch. The market is looking for the Manufacturing PMI to move back above 51 after spending the last two months with a 50 handle. If so that would still be well below the 55.4 average recorded in 2018. The services index is expected at 51.8 vs 51.5 prev. and down from the 54.9 2018 average.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.