Total spending grew 0.9% in June.

Friday marked a bad end to a tumultuous week for the markets, with equities, commodities and bond yields all hit hard.

https://soundcloud.com/user-291029717/chinas-manufacturing-crumbles-central-banks-ready-to-step-in?in=user-291029717/sets/the-morning-call

Powell pounds the global growth alarm, delivering an ‘emergency’ statement and signalling a likely rate cut at the upcoming March 17-18 FOMC meeting (see Statement for details). Markets now fully price a Fed cut, with a 30% chance of a 50bps cut. The move was made to calm markets (an echo of what happened in August 2007) which are selling off sharply on growing global growth concerns. The RBA also looks like it will join what seems to be a co-ordinated global easing effort, with noted RBA whisperer McCrann writing on Friday night “we will now all-but certainly get a rate cut from the Reserve Bank on Tuesday, if not also “other” action” and markets are now 97% priced for a March RBA rate cut (see Herald Sun for details). MNI also note the BoJ is likely to release a statement this morning, fearing the Yen could appreciate down through 105 (currently 107). Note the Bank of Canada also meets on Wednesday where markets are priced 82% chance of a cut. With policy rates so low, thoughts will now turn to how likely QE and negative rates are globally and also in Australia.

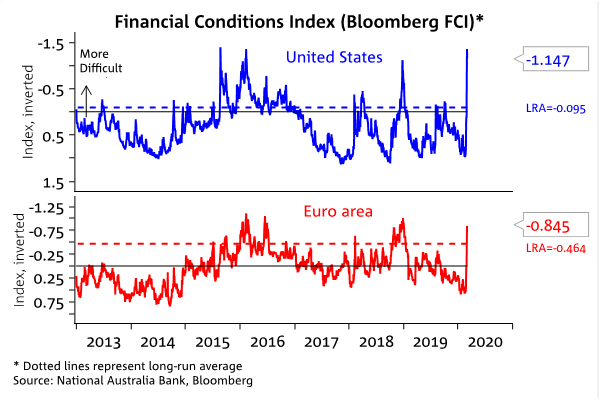

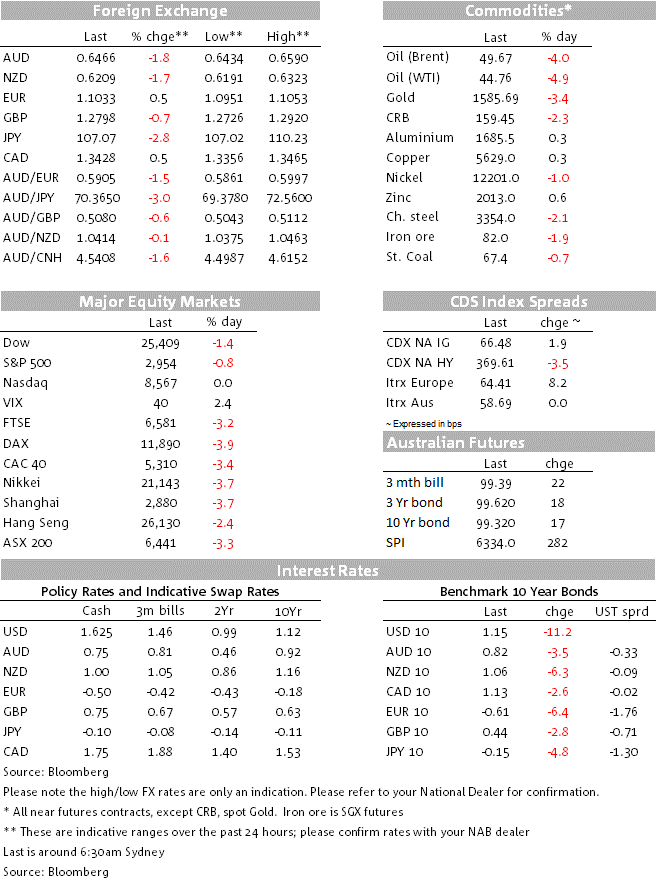

Despite smoothing central bank words, markets continue to see massive moves. The S&P500 fell -0.8%, though did pare losses from its initial -4.1% fall. Over the week though the S&P500 has fallen 11.5%. Yields also extended moves as equities sold off, and moved further lower on the emergency Fed statement. The US 10yr yield fell -11.2bps to 1.15%, while Australian bond futures indicate Australian 10yr yields will probably open at 0.68%, down from Friday’s 0.82%. Yield curves steepened slightly (2/10s +3bps to 23.6bps), though 3m/10yr remains negative at ‑11.8bps. Oil markets are fearful of a sharp fall in oil demand with WTI -4.9% to $44.76. G10 FX moves were also sharp with AUD (-1.8%) and NZD (-2.1%) continuing to be the global growth whipping boys. USD/Yen has recovered its preeminent safe haven status, -2.6% to 107.27 with MNI reporting the BoJ is worried about a move through 105. The USD in contrast fell -0.3% on Fed easing expectations with EUR +0.5%. As we open this morning, both the AUD and NZD look weak with a negative lead from China’s PMI on the weekend and ANZ’s NZ subsidiary calling for the RBNZ to cut rates 50bps at the March meeting, followed by another 25bps in May.

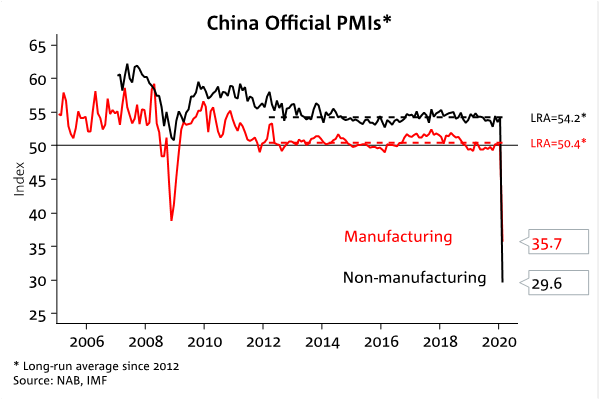

Global growth clouds darkened on the weekend with China’s PMIs plunging beyond GFC levels to be the lowest ever on record (see Chart below, also email Tapas.Strickland@nab.com.au if you would like to be subscribed to NAB’s China research). Manufacturing was 35.7 against 45.0 expected and 50.0 previously (GFC low was 38.8). Non-manufacturing was 29.6 against 50.5 expected and 54.1 previously (GFC low was 50.8). Worryingly for the rest of the world New Export Orders also declined sharply to 28.7 and at face value is suggestive of a global slowdown as currently priced by markets. (note China’s PMI has tended to lead the US ISMs by 2-3 months and suggests global PMIs could weaken considerably in coming months). Most firms expect to resume production by end of March, though the pace of a pick-up remains to be seen and high-frequency data continues to suggest activity running 15-30% below 2019 levels. Sourced headlines also suggest Chinese Q1 GDP will be sharply negative. Source stories suggest annual growth may be closer to 3% y/y, meaning Q1 GDP could be -1.5% q/q. A sharp rebound in activity would then be expected in Q2 as production comes back online and as stimulus gains traction. If China were to meet a 5.5-6.0% growth target, Q2, Q3 and Q4 growth would need to average 2.5% q/q – the strongest since the GFC stimulus of 2008-10.

Australia, the US and Thailand all reported their first death from the virus, while the virus appears to be spreading in Europe. Italy reported more than 500 new cases to 1,694 cases in total, while containment measures are being announced in a number of countries with France the latest in banning indoor gatherings of more than 5,000 people. The WHO raised its risk assessment to “very high”, but stopped short of declaring a global pandemic. The clear risk of COVID-19 spilling over to consumer and business confidence is very real and looks to be being realised. Media in Australia are reporting stockpiling and in many cases encouraging it, international firms are halting staff from travelling (Amazon the latest high profile banning all non-essential travel in the US and internationally), while travel bookings are down sharply (Asia-Pacific bookings are down ‑10.5% y/y excluding China/HK).

Data continues to take a backseat, being seen as dated. On Friday the US Core PCE Deflator was 1.6% y/y against 1.7% expected. The Chicago PMI rebounded more than expected (49 v. 46 expected), while German jobless claims fell unexpectedly with the unemployment rate steady.

Joe Biden had a landslide victory in the South Carolina primary, keeping his nomination chances alive (Biden was 48% to Sanders’ 20% and Buttigeig’s 8%). Total pledged delegates so far are Bernie with 56, Biden with 48 and Buttigeig with 26. Betting markets have pared slightly the chances of Sanders securing the nomination, falling to 52.6% with Biden at 28.5%.

A big week ahead where markets will be attuned to the potential impact of COVID-19 on the global economy and prospects of co-ordinated central bank easing. The PMIs and the US ISMs are the first off the block in this respect with the manufacturing versions out today. Domestically ANZ Job Ads will be closely watched for any potential impact of the virus on hiring intentions – anecdotes have some corporates suspending hiring plans. The RBA meets on Tuesday with markets 97% priced for a cut. Australia also has Q4 GDP figures on Wednesday, though this is likely to be ignored due to its dated nature unless there were to be a large downside surprise which would mean the economy was even weaker before potential COVID-19 headwinds. The Bank of Canada is another G10 central bank meeting this week, while the week ends with US Payrolls.

Key prints today:

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.