Total spending grew 0.9% in June.

In the US, the dollar, equities and bond yields have all risen on the news that China would rather talk than retaliate.

Sadly I didn’t I didn’t get to see the ‘Mac in Sydney last night but Rodrigo did, so doubtless he will be regaling you with the entire set list in Monday’s missive.

Monday will be a morning where, unless President Trump has a last minute change of heart, we will be greeted with the news that the 25% tariff rate on ~$250bn worth of Chinese imports had been lifted to 30% and that 15% (not 10%) tariffs have come into effect on about $110bn worth of additional imports, including agricultural products, antiques, clothes kitchenware and clothing.

Monday’s open will also be the first chance to react to the latest China official PMI data, due for release on Saturday.

Overnight price action has been driven in large part by news that hit the wires mid-morning London time that China indicated it wouldn’t immediately retaliate against the latest U.S. tariff increase announced by President Donald Trump last week.

China Ministry of Commerce spokesman Gao Feng told reporters in Beijing on Thursday that “China has ample means for retaliation, but thinks the question that should be discussed now is about removing the new tariffs to prevent escalation of the trade war,”. “China is lodging solemn representations with the U.S. on the matter.” According to Bloomberg, when asked if that meant China wouldn’t retaliate at all for the latest escalation by the U.S., Gao didn’t elaborate but repeated the same comments. China has hit back against each previous tariff increase by the U.S., so not responding in kind this time may signal a change in strategy, Bloomberg suggests.

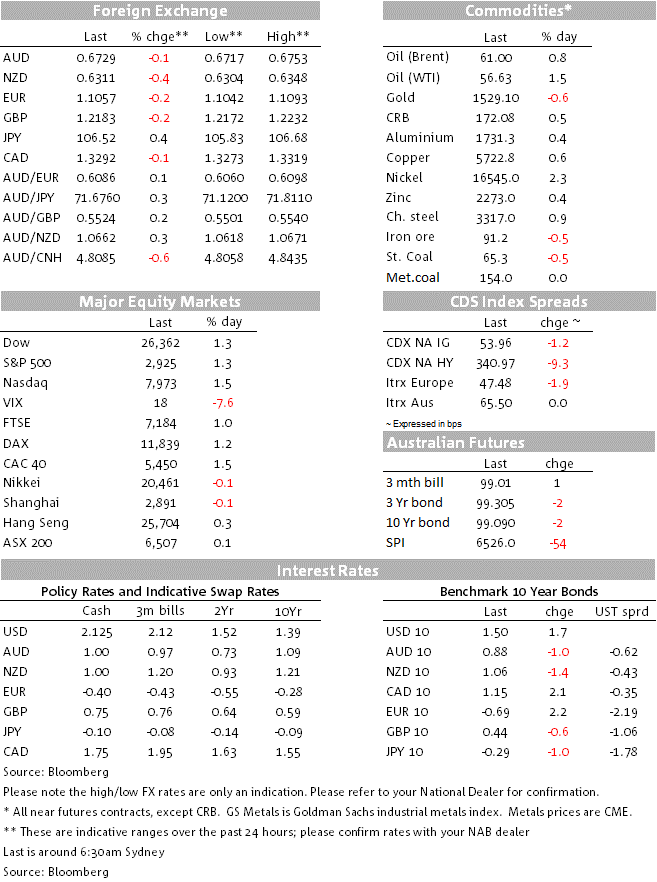

US stocks gapped higher at the Wall Street open on the back of this news, the S&P 500 by some 1.2%. Gains have held throughout the session (closing +1.3%) with similar gains for the Dow (+1.3%) and NASDAQ (+1.5%). IT and Industrials have been the best performing market sub-sectors

US bond yields are higher in tandem with improved risk sentiment, the 2-year note up 2.8bps to 1.53% and 10s by 1.5bps to 1.49%. The rise in US yields was given an additional boost by a very weak 7-year Treasury note auction, which was cleared 2bps higher than the prevailing secondary market yield at the time, tentatively suggesting investor demand might finally be starting to wane at these low yield levels. The bid-to-cover ratio was 2.16, its lowest level since the 7-year bond was reintroduced in 2009.

US data releases came and went without fanfare. These included the second vintage of Q2 GDP, revised down a fraction, to a 2% annualised rate from 2.1%, in line with consensus expectations. Personal consumption was revised up to 4.7% from 4.3% but this was offset by a decline in investment. Weekly jobless claims remained at very low levels (215k) while Pending Home Sales disappointed expectations at -2.5% m/m, reversing the 2.8% June gains and against an expected flat reading. The Advance July trade balance was a deficit of $72.3bn, down on $74.2b in June and the $74.4b expected, meaning that trade is not starting Q3 as a drag on GDP and with as yet no strong impression being made by tariff action to date.

In FX the narrow DXY US dollar index is coming into the close within a whisker of its year-to-date high on a closing basis (98.45 now vs. 98.52 on 31st July, the latter the highest since mid-May 2017). There really is no putting the big dollar down at the moment, slippage in the safe haven CHF and JPY the main contributors to latest gains, though in fact every G10 currency bar CAD (+0.1%) is weaker against the greenback, including a 0.1% fall for the AUD notwithstanding the China news and related improvement in risk sentiment. NZD is -0.4%, still struggling under the weight of yesterday’s particularly poor ANZ business survey.

EUR/USD is 0.2% weaker, having given back some intra-day strength that came off the back of comments from Dutch central bank governor Klaas Knot, who in an interview in Amsterdam said the economy does not yet warrant a resumption of the QE programme which, he says, would have no value added. He said if further stimulus is warranted then conventional policy would be the appropriate instrument to contemplate (funny how taking interest rates into deeper negative territory is now described as ‘conventional’).

We noted in our latest FX strategy publication on Monday that the earlier Olli Rehn comments about a comprehensive package of ECB easing measures in September described by the WSJ as a ’big bazooka’ were him just voicing a personal opinion, and Knot’s comments make clear they were indeed just that.

More than countering the positive EUR impact of Knot’s comments were subsequent remarks by incoming ECB President Christine Lagarde in written response to European parliamentary questions. Lagarde said that the economy faces downside risks, inflation is subdued and it’s “therefore clear that monetary policy needs to remain highly accommodative for the foreseeable future.” “The precise mix of instruments deployed will have to depend on the nature of the shocks affecting the outlook for inflation as well as on financial market conditions,” she wrote.

Yesterday Australian Q2 capital expenditure data was weak overall at -0.5% (mkt: 0.4%, NAB: -1%) but the underlying data were more positive. Importantly, spending on machinery and equipment – which is the component that feeds into GDP – grew by a solid 2.5%, implying a marginal 0.1ppt contribution to Q2 GDP. NAB’s current GDP forecast (due next Wednesday) is 0.5%

Australian July building approvals and private-sector credit, due at 11:30 AEST, are both likely to be weak. We expect approvals fell 1% (mkt: flat), as apartment approvals decline further. We expect monthly credit growth remained weak at 0.1% (mkt 0.2%).

Also due this morning is ANZ NZ Consumer Confidence (08:00 AEST) and Japan unemployment, retail sales and industrial production and Tokyo CPI.

Eurozone data highlight will be July CPI (seen 1% down from 1.1% but with core up to 1.0% from 0.9%). Last night’s German CPI data, which fell by 0.1% on an EU-harmonised basis against +0.1% expected, implies some downside risk here.

The US has the July personal income, spending and PCE deflator data, where the yr/yr rates for core and headline are expected unchanged on June at 1.6% and 1.4% respectively. Also Final University of Michigan consumer sentiment.

Official China PMI data is on Saturday

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.