Coming in for landing in a heavy cross wind

Insight

There’s a positive vibe about this morning, pushing equities higher and Treasury yields have seen a sharp rise too.

https://soundcloud.com/user-291029717/chinas-pmi-high-australias-gdp-bounce-the-brexit-tunnel-opec-delays-and-a-us-stimulus-deal?in=user-291029717/sets/the-morning-call

“Baby we can make it if we’re heart to heart; And we can build this thing together; Standing strong forever; Nothing’s gonna stop us now”, Starship 1987

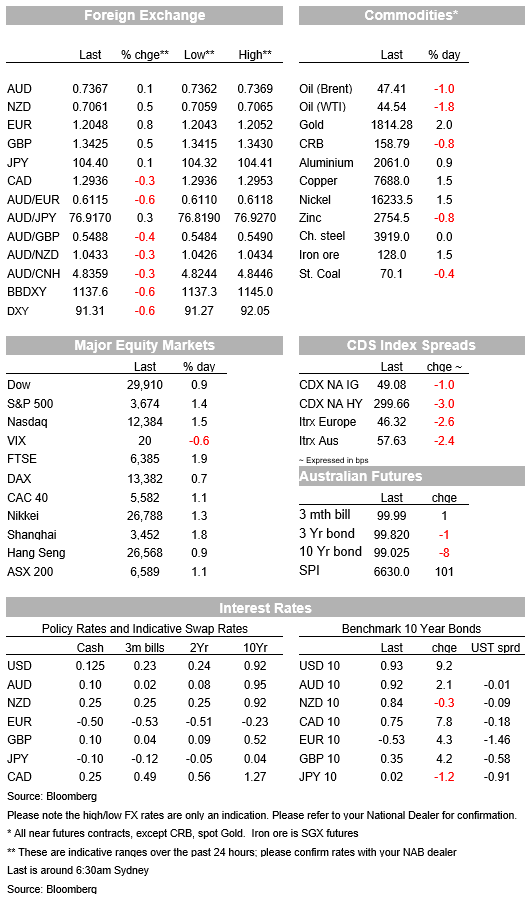

US 10yr yields rose 9.5bps to 0.93%, with the implied inflation breakeven +3.6bps to 1.8251% and the highest since May 2019. Note the US 30yr is also at its highest since May 2019 at 1.9459%. Equities also rose with the S&P500 +1.4% with all 11 sectors in the green. Driving moves overnight were continued vaccine hopes, the possibility of a US fiscal stimulus deal during the lame duck session, as well as strong economic data even with the rise of COVID-19 cases in the US.

Pfizer and BioNtech formally submitted a request for EU approval for their vaccine with an assessment due on December 29th (note Moderna is pencilled in for January 12th) with distribution of the vaccines possible from January. Both companies have already submitted their emergency use authorisation in the US with Trump’s chief science advisor noting that the entire US population could be vaccinated by June. Dr Sloui said Moderna and Pfizer will likely have between 60-70m dosses by January, enough for 30m people and that the US could begin supplying more than 150m dosses a month by March once other vaccines are authorised. Given the vaccines are 90-95% effective, markets are looking for a very quick return to pre-COVID activity in the US with Dr Sloui’s timeline suggesting that return could happen in H1 2021, instead of H2 2021 as many had pencilled in.

Fiscal stimulus hopes also returned overnight with a bi-partisan proposal for a $908bn stimulus plan. House Speaker Pelosi is said to have delivered a new stimulus proposal, while Senate Majorty Leader McConnel said he is also circulating his own revised plan which has the support of President Trump. There appears to be added momentum this time to the negotiations with McConnel stating “waiting until next year is not an answer”, “I’m focused on accomplishing as much as we can”. Meanwhile President-elect Biden also called on Congress to pass a “robust package” and that any package passed during the lame duck session would be “at best just a start” and thus seemingly greenlighting a slimmed down stimulus with a more comprehensive plan coming after inauguration day. One possible complication that suggests it isn’t a straight up shot, is the Georgia Senate run-offs on January 5 which will determine who has effective control of the Senate. Democrats need to win both of these run-offs with PredictIt ascribing a 29% chance.

Given the positive risk backdrop, the USD was firmly on the backfoot with DXY -0.6%. The major drivers were EUR (+0.8% to 1.2048 and the highest since 2018) and GBP (+0.5% to 1.3425) with positive UK-EU headlines and the ECB’s Schnabel hinting December’s QE announcement may not be a blockbuster (“It is appropriate to focus on preserving these conditions rather than easing much further”…“ If it’s necessary to do something that doesn’t meet market expectations, we have to do that nevertheless.”).

On UK-EU trade headlines, The Times reported that talk had entered the “tunnel” with EU negotiator Barnier having stopped internal debriefs. The tunnel is the radio silence that precedes the final deal making. Hopes are said to be high and markets are also trading with this view with GBP close to the 1.35 level where we though it would trade upon the confirmation of a deal (currently 1.3425).

The AUD has underperformed in this risk-on environment, up just 0.1% to 0.7367. Also underperforming at the oil-linked currencies (USD/CAD -0.3%) with the oil price down overnight with OPEC talks continuing and no closer to an agreement. Brent fell 1% overnight. In contrast the NZD rose 0.5% with the AUD/NZD cross -0.3% to 1.0433.

The Caixin manufacturing PMI rose to 54.9 from 53.6 in October, the highest in 10 years. The US ISM shook off the rise in COVID-19 infections, printing close to expectations at 57.5 against the 58.0 consensus. Export orders were reported to be rising at their fastest pace since March 2018, suggesting of positive global momentum despite COVID-19 cases in the northern hemisphere. Once a vaccine starts to distributed, it is likely there is still a lot of pent up demand which could buoy factory production for some time.

Reflecting the run of better than expected data globally over recent months, the OECD upgraded its near term outlook. It now projects the global economy to contract 4.2% this, up from 4.5%. Australia’s outlook was also upgraded, with the economy now expected to contract 3.8% this year, up from the 5% contraction pencilled in previously.

Yesterday’s RBA meeting was a non-event with little impact on markets. One surprise that might have been seen was the slight downplaying of the recent run of data that has surprised sharply to the upside, with a continued emphasis on the recovery being “uneven and drawn out” with the unemployment only expected to decline “slowly”. One area currently under debate for markets is the $100bn QE program which expires in five months. Markets are likely to speculate over whether the program will be continued, tapered or even stopped. That debate will likely be closely tied to the trajectory for the unemployment rate as it should. Not surprisingly, the RBA did not broach the subject today, noting that “the Board will keep the size of the bond purchase program under review, particularly in light of the evolving outlook for jobs and inflation” but equally stating that the Board is prepared to do more.

Domestically all focus on Governor Lowe who is giving Parliamentary Testimony (10am AEDT) and then onto the Q3 GDP figures. Offshore it is also central bank focused with RBNZ’s Orr speaking at an ANU lecture and the Fed’s Powell speaks to the House after having already spoken before the Senate on Tuesday. Key details below:

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Coming in for landing in a heavy cross wind

Insight

Conditions again fell in Q2, but confidence stabilising

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.