NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

The US dollar is down again with equities up and touching new highs again.

One of our traders yesterday was remarking that perhaps for the first time in as much as six months, incoming economic data was starting to matter, for currency markets in particular. He was referencing in particular the (negative) reaction of the EUR/USD exchange rate to the pull-back in most of the Eurozone ‘flash’ PMI data last Friday that was then followed by the better than expected US-equivalent Markit PMIs and outsized leap in US Existing Home Sales.

Have been seeing something of a wedge being driven between the hitherto slavish negative day-to-day correlation between the performance of risk assets (read the S&P and NASDAQ) and the performance of the US dollar. Certainly this was the case on both Friday and Monday, though overnight the USD is modestly weaker (indices down 0.2-0.3%) in what has for the most part been another risk-positive night, at least as far as the S&P and NASDAQ are concerned, the former finishing in New York +0.36% and the latter +0.76%.

It hardly needs saying, but these are both new record highs. Bond yields are also higher, 10-year Treasuries up to as high as 0.715% before dropping back to 0.685% in late afternoon US trade, still 3.5bps up on Monday’s US close. Not that the renewed yield back-up is (yet) having any noticeable impact on US risk asset performance.

Risk drew a little support during our time zone yesterday, and which extended into offshore markets, from news the deferred US-China six-month review of the Phase-1 trade deal actually took place on Monday night, bringing together via video conference U.S. Trade Representative Robert Lighthizer, Treasury Secretary Steven Mnuchin and Chinese Vice Premier Liu He. Following which, officials from both sides said they were committed to carrying out the Phase One trade accord between the two nations. The USTR office released a one-paragraph summary of the talks, which it said included discussions of “significant increases” in the purchases of U.S. products by China. “Both sides see progress and are committed to taking the steps necessary to ensure the success of the agreement,” the statement said.

To which the EUR/USD exchange rate has against proved sensitive. Thus the combination of an upward revision to the earlier Q2 German GDP number (from -10.1% to -9.7%) was quickly followed by the German IFO survey which somewhat contradicted the message from last Friday’s (service sector) flash PMI.

The overall Business Climate reading rose to 92.6 from 90.4, when markets seemed braced for a number below the 92.1 consensus. Following the release the IFO President said the German economic recovery was more or less on track. From pre-GDP to post-IFO, EUR/USD rose from sub-1.18 to a high of 1.1835 (and has made a high overnight of 1.1843, on a day when a move back towards important support near 1.17 was looking probable).

Yet more strong – and much stronger than expected – housing market data came in the form of July New Home Sales, up 13.9% on top of June’s 13.8% jump and well above the 1.8% expected. With 3% 30-year mortgage rates, tax deductable interest and no capital gains tax from currently strongly rising prices, what’s not to like about buying a house, as long as you can qualify for a mortgage of course?

Has been the Conference Board’s version of Consumer Confidence, which fell to 84.8 from 91.7. Both expectations and the present components of the confidence report took a knock; on the surface a disappointing read. Disappointment over the lack of another fiscal package supporting incomes, still choppy news on the virus and last week’s jobless news not that comforting either. The Conference Board measure has tended to follow the labour market over time, offering a partial explanation. This reading puts consumer confidence back to pandemic lows.

Was the Richmond Fed Manufacturing Index which rose to 18 rather than the (unchanged) 10 expected. So far on the manufacturing side of the US economy for August, the Empire State measure was quite a bit lower at 3.7, the Philly Fed index down to 17.2 from 24.1 and now Richmond Fed 18 from 10; a bit of everything so far. Recall the Markit PMI measure was up 3.3 points to 53.6. The Manufacturing ISM report is next Tuesday.

The USD is weaker against everything bar the JPY, USD/JPY getting a nice lift from the move higher in US Treasury yields, on top of yesterday’s decent showing by the Nikkei. Leading G10 moves against the USD has been GBP, recovering another 0.7% after last Friday’s hit on negative EU-U trade talk headlines. No hard news to justify the move hear, though optimism surrounding the potential early release of the Oxford University/Astra Zeneca covid vaccine is being mentioned in dispatches (the one President Trump is now seeking to fast-track). Other G10 currencies are up by between 0.4% and 0.5%, including a 0.45% rise in AUD/USD to see the pair back flirting with the 0.72 level.

Shows that jobs decreased by 1% over the four weeks to 8 August, with much of the move (-0.8ppts) occurring over the past two weeks. Keeping in mind that these data can be revised significantly, especially the last 2 weeks, crudely seasonally adjusting these data suggests a fall in employment of 50k in August. Unsurprisingly, the biggest declines were recorded in Victoria, with a 2.8% loss of payrolls jobs over the past month and 1.6ppts of that occurring in the past two weeks. This leaves Victorian payroll employment close to the previous lows recorded in April (nearly -8% on March), with overall Australian payrolls employment still down a massive 4.9% on pre-pandemic levels.

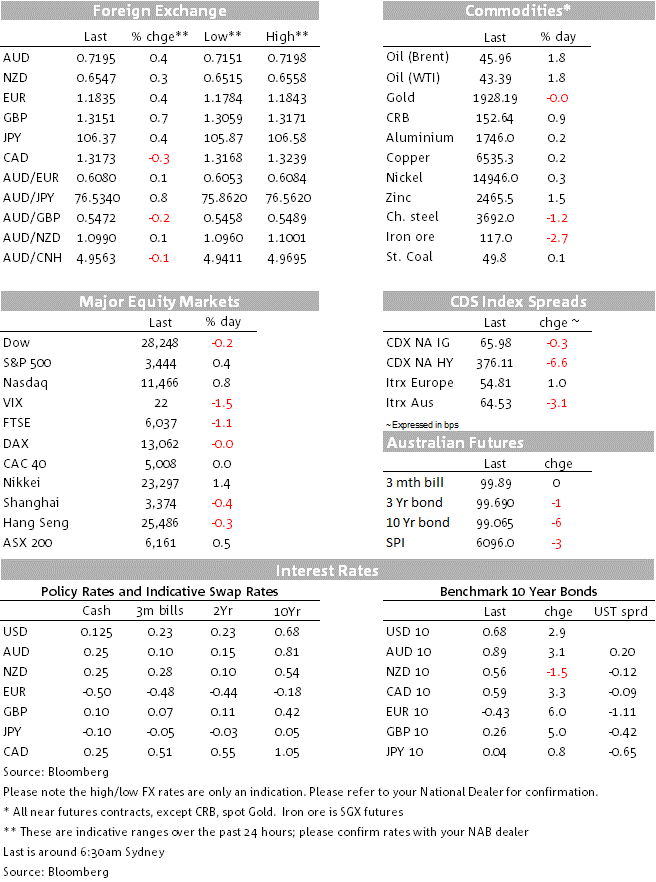

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Confidence and Conditions Lift

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.