Long-term signal vs. Short-term noise

Insight

The fear of blood clots from injections means use of the Astra Zeneca vaccine has been suspended in an increasing number of European countries.

https://soundcloud.com/user-291029717/clots-slow-down-the-eu-vaccine-rollout?in=user-291029717/sets/the-morning-call

Calm like a bomb..Ignite, ignite… – Rage against the machine

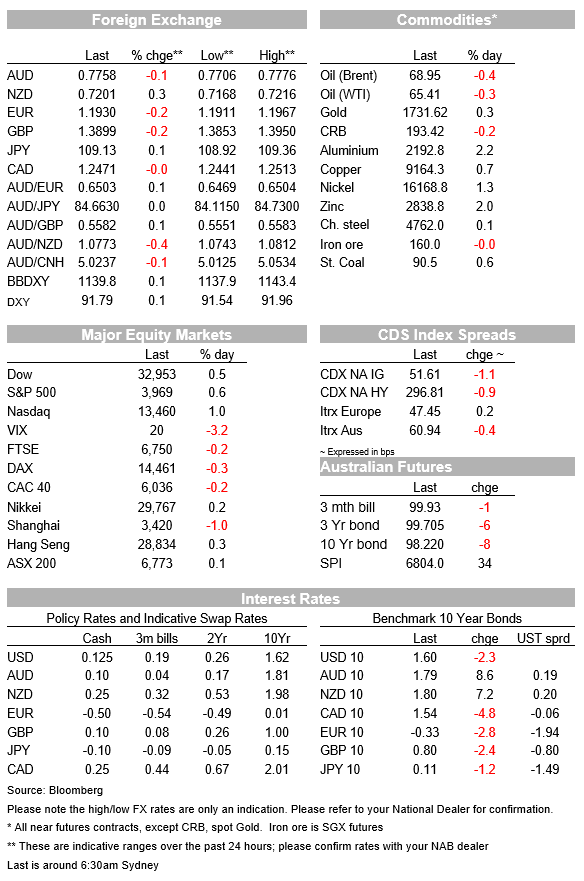

It has been a quiet start to the new week with markets essentially marking time ahead of the FOMC meeting early our Thursday. European equities are slightly lower weighed down by concern around the impact from European countries suspending the use of AstraZeneca’s vaccine while US equities are marginally higher after falling half way through the session. UST yields have drifted a little bit lower and the USD is broadly stronger with NZD and CHF the outperformers.

European equities erased early gains as sentiment in the region took a knock following news of several European countries’ suspension of the AstraZeneca’s Covid-19 vaccine amid concerns over a potential link with blood clots. After Denmark and Norway stopped giving Astrazeneca shot last week, Iceland and Bulgaria followed suit and Ireland and the Netherlands announced suspensions on Sunday. Overnight Germany, France and Italy said they were also pausing the AstraZeneca’s COVID-19 vaccine to investigate possible side-effects. The AstraZeneca suspension compounds the slow vaccine rollout in Europe and reinforces the market’s belief that the European recovery will be slower to get going than the US and UK, which have been far quicker in rolling out vaccines. Italy went back into lockdown today amidst a resurgence in new cases. Major regional equity indices closed marginally in the red while the Stoxx Europe 600 Index ended the day unchanged, after advancing as much as 0.7% during the session.

After initially following European equities lower, US equities are now marginally trading in positive territory with the NASDAQ up 0.50% while the S&P 500 is 0.13%. The better than expected Empire State survey released overnight didn’t elicit much of a market reaction.The survey’s headline index rose to 17.4 from 12.1, slightly above the consensus, 15. The report’s details were less impressive, however, with the new orders and employment indexes dipping by 1.7 and 2.7 points respectively while the prices paid index jumped 6.6 to 64.4, its highest since May 2011.The US tax agency started distributing the $1,400 stimulus cheques on the weekend and market participants expect at least a portion to be parked in the equity market. This has helped maintain positive sentiment.

The European vaccine news probably also played a factor in the move lower in core European yields, with 10y Bunds down 2.8bps to -0.336% while 10y UK Gilts fell 2.4 to 0.795%. UST yields have also drifted lower with the flattening of the curve led by the back end of the curve. The 30y Bond eased 3.5bps to 2.345% while the 10y Note is 2.5bps lower currently trading at 1.601%.

The FOMC policy decision and new forecasts early on our Thursday are undoubtedly another factor keeping investors a little bit cautious at the start of the new week. There is a lot of focus on whether the new forecasts and dots plot will vindicate the current lift in Fed hike expectations.

Moving onto currencies, the USD is mildly and broadly stronger with the BBDXY and DXY indices up 0.09% and 0.18% respectively. The EUR and GBP are down about 0.2%, with the AstraZeneca news slightly weighing on both currencies (AstraZeneca has been the main source of vaccines in the UK). Bank of England Governor Bailey was the latest central banker to look at the rise in bond yields with a ‘glass half full’ lens, telling the BBC that the increase in yields was “consistent with the change in the economic outlook.” The BoE’s monetary policy meeting is later this week.

NZD along with CHF are the only pair showing gains against the greenback, up 0.35% and 25% respectively . NZD gains which now sees the pair trading at 0.7202, are hard to explain, although looking at the intraday chart the AUD/NZD underperformance might have smoothening to do with it. The cross opened the new week just above 1.08, but then came under pressure following the underwhelming China activity readings and softness in the CSI 300. The AUD typically shows more sensitivity to China’s economic fortunes and after trading to an overnight low of 0.7706, the AUD now trades at 0.7757, down 0.13% over the past 24 hours.

The monthly batch of Chinese activity data was a mixed bag, with weaker-than-expected fixed asset investment (as the authorities clamp down on property developers) and stronger-than-expected retail sales. The headline year-on-year numbers in all cases were flattered by base effects from the lockdown 12-months ago. China’s CSI 300 equity index fell 2% yesterday, bringing its cumulative decline from its recent peak to 13%. Meanwhile the PBoC injected 100 billion yuan ($15 billion) through its medium-term lending facility on Monday, matching the amount maturing Tuesday. The restraint provision of liquidity by the PBoC has brought back concern the Central Bank liquidity tightening will continue.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Long-term signal vs. Short-term noise

Insight

Join us as we discuss interest rates, general economic conditions, and the NAB AUD/USD forecast

Webinar

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.