A private sector improvement to support growth

Insight

The biggest moves across Global Markets have been seen in the US rates market, where break-even inflation rates have jumped by a full 10 basis points at both 5 and 10 years.

https://soundcloud.com/user-291029717/commodities-down-but-inflation-fears-stay-high?in=user-291029717/sets/the-morning-call

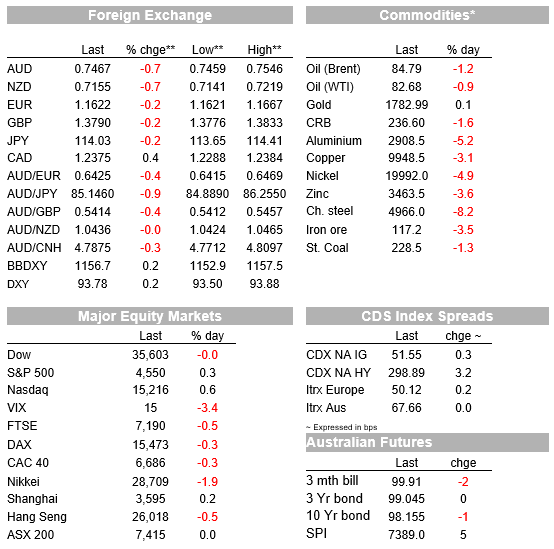

After looking somewhat punch-drink since the middle of last week, the USD has found its feet overnight, though not with any great alacrity, in conjunction with a significant (upward) re-pricing for Fed policy but which hasn’t done any great harm to US equity valuations where the S&P500 has just closed at a record high notwithstanding a drag from Energy and Materials stocks on sharply lower commodity prices. The AUD has gone from hero to zero in the last 24 hours, falling from an intra-day high during our session of 0.7546 to a low of 0.7459. If it ends the New York day below 0.7465 it will have completed a (bearish) key-day reversal.

Glancing across markets since the local session closed on Thursday, some of the biggest moves have been seen in the US rates market, where break-even inflation rates (implied from the difference between the yields on US Treasury nominal and inflation protected securities (TIPS)) have jumped by a full 10 basis points at both 5 and 10 years, to 2.91% and 2.66% respectively. This is the highest since September 2012 for the 10-year and highest on record for the 5-year. Nominal yields themselves see the 2-year up 5bps to 0.434% and 10-year a lesser 2bps up to 1.675%, its highest since May 20.

There hasn’t been any new Fed policy related commentary from officials overnight to drive these moves. The only Fed related development has been an announcement that henceforth policy makers and other senior officials will be banned from buying individual stocks and bonds and be restrict from active trading. This is after an ethics scandal which led to the recent departure of two regional presidents. Under the new policies, senior Fed officials – including regional bank presidents, Washington governors and senior staff – will be limited to purchasing diversified investment vehicles such as mutual funds, the central bank said in a statement Thursday.

US data was not really consequential for market price action either, but for the record showed initial jobless claims falling to 290K from 296K, a bit below the consensus, 297K and to a new covid-era cycle low, while the Philly Fed index fell to 23.8 from 30.7, marginally below the consensus, 25.0. Of more note here perhaps – and allied to the latest jump in market-implied inflation expectations – the prices paid index jumped again, to 70.3 from 67.3. We have also had Intel’s CEO out saying he expected the shortage of semiconductors, which has hampered auto and electronics production, will continue into 2023, while consumer products bellwether, Unilever, said it had increased the price of its products by an average of 4% during the third quarter, its CEO saying that it expected inflation pressures to continue through the first half of next year.

Also released, US Existing home sales jumped 7.0% to 6.29m from 5.88m, well above the 6.10m consensus. Following Tuesday’s weak housing starts and – more telling perhaps – the downtrend in building permits, then the juxtaposing of softening supply but still-strong demand can only one thing for house prices, can’t it?

Quite a last 24 hours in FX, where we witnessed a rapid reversal yesterday afternoon of morning gains for currencies – no more so than the AUD, an which have extended overnight. From an intra-day high of 0.7546 yesterday morning – to its best level since July 6, AUD/USD lost half a cent in short order in afternoon trade and losses have extended to a low of 0.7459 offshore . Its been a broadly similar story for other commodity -linked currencies, with the NOK, NZD and AUD all coming into the New Yok close down by 0.7% on the day. The JPY and CHF are the only two major currencies up against the USD and where the DXY is ending the NY day up about 0.25% at 93.80.

There was no obvious catalyst for the initial fall from grace yesterday afternoon, but looking across the commodity complex this morning, with the exception of the gold price (up $2.50) energy, metals and agri. are without exception lower with particularly large falls evident in aluminium (-5.2%) and copper (-3.5%). Oil is down $1 for the Brent benchmark and WTI by 80 cents. Maybe commodity markets are finally waking up to the implications of the travails of China’s property sector for hard commodity demand, in which respect Evergrande shares recommenced trading yesterday after a three week trading halt with its shares down more than 10%. This weekend sees the 30-day grace period on non-payment of its dollar bond obligations lapse, so come Monday we should be reading about its formal default.

Finally in news literally just in, the Bank of England newcomer Huw Pill is in the FT saying that UK inflation is likely to hit 5%, and that the November MPC meeting is ‘live’ with a decision ‘finely balanced’.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Read our NAB Markets Research disclaimer

A private sector improvement to support growth

Insight

Online retail sales growth accelerated 1.1% in April

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.