We expect growth in the global economy to remain subdued out to 2026.

Insight

The breaking news this morning is that Italy’s premier designate Guiseppe Conte has stepped aside, unwilling to form a government.

https://soundcloud.com/user-291029717/conte-out-oil-down-talks-on

This time yesterday, there seemed to be every chance that Monday morning’s market re-open would see some fresh pressure on all things Euro following Friday’s night’s news that Moody’s had placed Italy on watch for a possible downgrade to its Baa2 long term sovereign rating (the latter already just two notches above sub-investment grade, or junk).

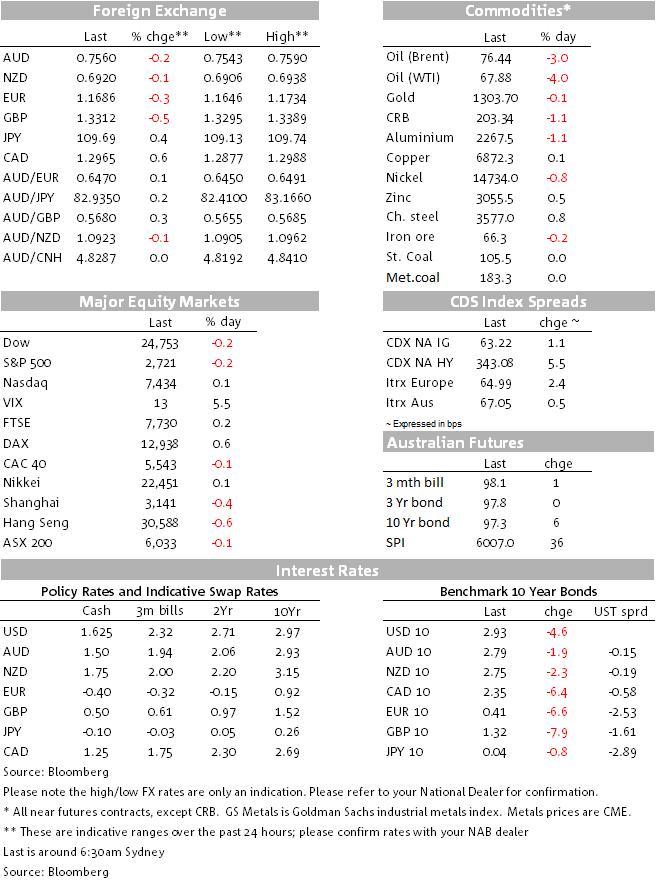

24 hours on and news that Italian president Sergio Mattarella has rejected PM-designate Giuseppe Conte’s proposal for Italy’s new finance minister – the known Eurosceptic Paulo Savone – has produced exactly the opposite market response at the Wellington open. EUR/USD is currently 0.3% up on Friday’s New York closing level and AUD/EUR 0.2% lower, with AUD a touch firmer on the back of this and other risk-positive news. The latter includes ‘on again’ indications regarding the Trump-Kim Summit in Singapore originally scheduled for June but abandoned by President Trump late last week.

The Italian news has met a furious response from 5-Star with shrill comments about seeking the impeachment of the President, while League – 5-Star’s putative collation partner – is out saying fresh elections are the only answer. The latter may well be so and the obvious risk is that populist parties fare even better than in February on what many may see as an affront to democracy. At the same time, we know there remains popular support for the Euro (and EU membership) inside Italy and Mattarella’s rejection of Savona precisely because he would not countenance a finance min sure who risked taking Italy down the path of ‘Italexit’, might work the other way.

For now, the Euro’s recovery is likely to continue and Italian bond spreads over the Euro-core will compress. Also supportive might be ‘source’ reports from both Reuters and Bloomberg on Friday saying the ECB is still determined to end its APP (QE) by the end of the year and that guidance to this effect could come as early as the June 14th Council meeting. One report says that some ECB GC members will be revising up their CPI forecasts in June based on higher oil prices and now EUR slippage.

This Euro-positive news aside, Spain is also on the radar after the Socialists – the largest opposition party in Spain, tabled a no-confidence motion in Prime Minster Rajoy on Friday, but this is not expected to succeed without the support of all other opposition parties. The more reform minded Ciudadanos party reportedly won’t side with the Socialists but will likely later table its own no-confidence motion. On some accounts, they could emerge as the biggest party if there are fresh elections

The bigger news since we went home on Friday – and the pretext for an Elvis Costello track being awarded today’s titular honour – is oil. Brent crude lost 3% or $2.35 to $76.44 and WTI 4% or $2.83 to $67.88 on seemingly firm indications from Saudi Arabia that OPEC members and Russia will boost oil output next month. The FT on Saturday reported quite categorically that OPEC and Russia are set to lift oil output by up to 1m barrels a day, in a move to curb a rally that had taken prices above $80 a barrel and prompted calls for restraint from the US. The FT says the decision to raise output, though not to be finalised until next month, is a stark reversal for the oil cartel and its allies who have been reducing supply since the start of last year. The increased production is seen replacing lost supply from Venezuela and Iran once sanctions are imposed.

A crunch in energy shocks was enough to pull both the S&P500 and Dow Jones down by 0.25% (NADSAQ outperformed, off only 0.13% while the Russell 2000 was virtually unchanged). On the week, significantly contrasting fortunes between U.S. markets (up) and European and Asia bourses (both down) where Italian politics, rising EM angst and a re-strengthening JPY undermined non-US markets:

In bonds, the fall in oil prices produced a 4-5bps decline in 5-10yr Treasury yields of which roughly half was via a drop in the break-even (inflation-related) component of nominal yields. On the week, 5 and 10yr UST yields are both over 12bps lower and 2s down 7bps, the mid-week FOMC minutes one driver of the fall in front end yields:

In FX, NOK and CAD were predictably the biggest casualties of the oil price plunge while EUR/USD made a fresh year to date low of 1.1648 as Spain joined Italy in adding political uncertainty into the mix (and proving a modicum of additional support to CHF). JPY was slightly softer despite the fall-back in UST yields. Continued lack of clarity on the U.K.s Brexit position continued to chip away at GBP. NZD outperformed AUD, the latter undermined by falling base metals prices as well as oil. On the day, DX was +0.5% and BBDXY a smaller 0.3% due to its lesser EUR weight. This is much more apparent on the week, where BBDXY ends virtually unchanged but DXY +0.66%, to a new mini-cycle high of 94.28.

In commodities, as well as oil, all base metals bar zinc were lower while steaming coal out of Newcastle continues its rally, up the best part of another $1 to $106.50 a tonne and now some $13 higher on a month ago. On the week, it’s a very mixed performance for base metals that leaves the LMEX index flat. WTI crude ended $4.36 back from Monday’s highs.

Economic data failed to have much market influence on Friday. The final University of Michigan final May consumer sentiment index slipped to 98.0 from its 98.8 preliminary reading while US April Durable Goods Orders fell by a slightly more than expected 1.7%. The core numbers (ex transport and ex defence ex-aircraft) were though both modestly better than expected at +0.9% and +1.0% respectively.

Locally, the preliminary weekend auction clearance rate across the combined Australian capital cities was 59.7% up from last weekend’s final 56.8% (latter the lowest since 2013). Sydney cleared a preliminary 62.7% versus last weekend’s final 54.0% and Melbourne 60.9% versus last weekend’s final 62.0%.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

We expect growth in the global economy to remain subdued out to 2026.

Insight

Financial institution issuance has recorded another high-volume year in the Australian dollar bond market, with some key questions still to explore ahead of a fast start in 2025.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.