China’s efforts to contain the coronavirus calm markets, but reported death tolls doubles in less than 24 hrs

WTO to decide if the SARS like virus is a public health emergency

Trump wants trade deal with EU before election, but EU harder to deal with done China

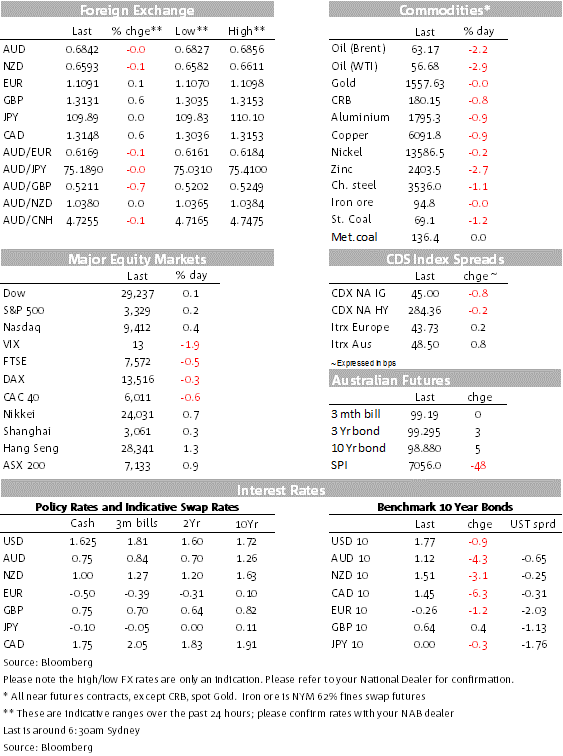

GBP is again the G10 outperformer as the CBI business optimism index jumps post Bojo’s election win

CAD is the big underperformer. BoC stands pat as expected, but delivers a dovish message

NZD and AUD are little changed

AU labour force report today’s highlight ahead of ECB tonight

Ooh that’s why I’m easy, I’m easy like Sunday morning

That’s why I’m easy, I’m easy like Sunday morning! – Commodores…note Faith No More cover renamed the song as “I’m Easy”, the latter is my preferred rendition

A sense of serenity has taken over markets following China’s efforts to contain the coronavirus infection and its openness in sharing developments on the outbreak (compared to apparent cover-ups during previous pandemics). US equity markets are back on the green with tech shares leading the move up, helping the NASDAQ climb to yet another new record high. The USD is little changed, but solid data sees GBP as the G10 outperformer again while a dovish BoC message sees CAD as the underperformer. AUD and NZD have been bystanders while core global bond yields are also little changed. Trump wants trade deal with EU before election, but notes EU is harder to deal with done China, more tariffs remain a negotiating option. WTO to decide later today if the SARS like virus is a public health emergency.

Main US equities indices are losing ground as we type, but remain on the green for the day. IBM beat revenue estimates and Tesla market value spiked past $100bn, topping Volkswagen AG for the first time. Earlier in the session, all major European equity indices closed with negative returns for the day, notwithstanding a positive start which saw the Stoxx Europe 600 Index climbed as much as 0.4%, before closing the day at -0.1%.

China efforts and transparency in terms of developments on the virus outbreak provided a boost to Asian equities with European equities embracing the feel good vibes at the open. This positive lead however lost momentum as the session unfolded as EU as automakers wilted following poor results from Daimler and the threat of US tariffs.

On his second day at Davos

President Trump said that he is hoping to strike a trade deal with the EU before the US election in November, however the President reiterated the option to impose tariffs on EU cars and parts if negotiations stall. He also announced a new plan to reform the World Trade Organization and confirm the deal with France on digital taxation, which hopefully leads to a global solution instead of unilateral tax regimes. On the latter worth noting US Treasury Secretary Steven Mnuchin remarks, noting that the US could use tariffs on automobile imports against countries that institute their own taxes on technology companies. “If people want to just arbitrarily put taxes on our digital companies, we will consider arbitrarily putting taxes on car companies,” Mnuchin said. “We think the digital tax is discriminatory in nature.”

Moving on to currencies

The USD is little changed in index terms with DXY at 97.534 as we type and BBDXY at 1194.20. GBP is the outperformer again, up 0.57% to 1.3135 following a much better than expected CBI business optimism print, the index jumped from -44 to +23, its highest level in over 5 years, setting the scene for a decent recovery in tomorrow’s PMI. Alongside upbeat labour market statistics and the bounce in housing data, the market is now more evenly balanced about whether the BoE will cut rates at the end of the month.

Meanwhile CAD has been the big underperformer, down 0.56% to 1.3140 after a dovish BoC meeting. While inflation data showed core inflation as expected, tracking just above 2%, the BoC kept its policy rate unchanged at 1.75% but removed its assessment that the current degree of policy accommodation was “appropriate”. The market took the view that the door was left open for a future rate cut and this was later confirmed by Governor Poloz, who indicated as much, with downside risks emerging for inflation. The market prices in almost a full 25bps cut by the July meeting, with Canada’s 2-year rate down 7bps to 1.54%.

The AUD and NZD are little changed relative to levels this time yesterday. The AUD now trades at 0.6843 and NZD trades at 0.6594. Early this morning, Fitch Ratings affirmed NZ’s long-term credit rating at AA but upgraded the outlook to positive, reflecting NZ’s sound fiscal management and low and declining government debt to GDP ratio. As typical, the announcement had little impact on the NZD.

While markets have shown a sense of calmness following China’s efforts on containing the coronavirus outbreak, we think the lack of a rebound in risk sensitive currencies, such as the AUD and NZD, reflects a sense of cautiousness. China’s efforts to be transparent is a reprieve for markets, but our suspicion is that cautiousness is likely to remain a near term theme nonetheless. Previous outbreaks such as SARS, suggest the base case should be for a temporary hit to activity, particularly those related to travel, transport and retail. Oil prices may also come under pressure as transport/travel activity decline. The news flow on the virus outbreak remains very fluid, the death toll has almost double in the past 24hrs from 9 to 17 and as we are about to press the send button, Chinese officials have announced a travel ban the city of Wuhan. So for now it remains to be seen if China has managed to contained the outbreak, particularly given the upcoming holidays.

On this score is also worth noting that the World Health Organization will decide later today/early on whether to declare the outbreak a public health emergency of international concern, a designation used for complex epidemics that can cross borders. The United Nations agency said it would meet again Thursday to determine a strategy.

Coming up

Australia’s December Labour force report is the domestic highlight today with the ECB rate decision tonight the other key event to watch. New Zealand gets net migration figures (Nov) and the All Industry Activity Index is out in Japan (Dec)

In November, Australia’s employment grew by a sharp 40k after falling 25k a month earlier. While the strong jobs result was welcome news, NAB continues to expect employment growth to slow over the coming months; employment conditions in the NAB survey, job vacancies and SEEK job ads and sub-par growth all suggest demand for workers is waning.

As such, NAB forecasts a weaker increase of 10k in December employment and a tick up in unemployment to 5.3%. Unemployment has been printing between 5.2% and 5.3% since April 2019 and we continue to expect weak private sector activity to result in a gradual rise in unemployment over 2020.

The ECB tonight is not expected to yield any surprises. This “in between forecast meeting” is widely expected to leave the current policy setting unchanged while attention at President Lagarde press conference is likely to be on the formal launch of the ECB monetary policy strategic review. That said, one theme to watch out for is whether or not the ECB inches up its optimism on the outlook following January signing of Phase 1 of the US-China trade deal and the signing of the Brexit Withdrawal Agreement.

Creating cost-effective choices for consumers while forging business success is nothing new for Chemist Warehouse co-founder Jack Gance. As special guest at a recent NAB Transaction Banking event series, he looks at a new way to pay for businesses and customers.