We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

There was a strong risk-off mood on Friday due to the spread of the COVID-19 infections and the impact it's having on the global economy.

https://soundcloud.com/user-291029717/covid-19-jitters-hit-asian-currencies-aussie-dollar-at-11-year-low?in=user-291029717/sets/the-morning-call

I’m losing my edge

I’m losing my edge to the kids from France and from London – LCD Soundsystem

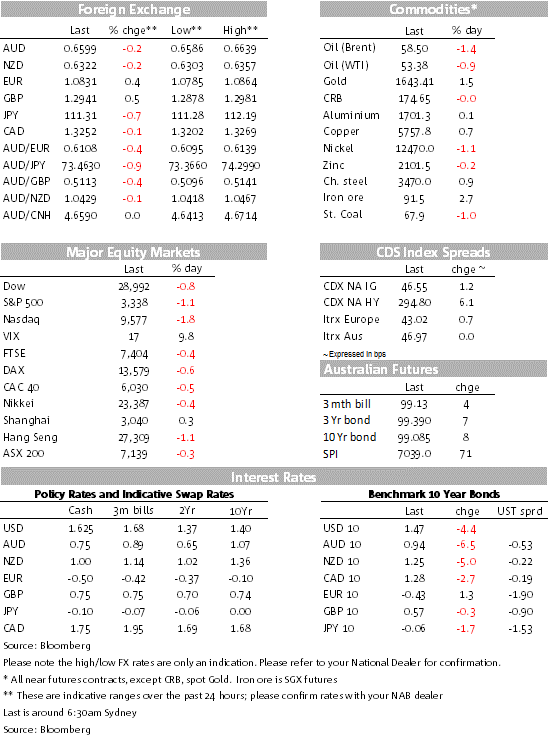

COVID-19 anxiety moves beyond China and takes on a global dimension with rises in reported infections from South Korea to Italy, China also reported a spike in cases over the weekend. Data on Friday night didn’t help sentiment either with US PMI prints disappointing, the Services sector is now in contractionary mode. UST Curve bull flattens with the 30y bond making a new low, the NASDAQ led the decline in US equities while the USD lost some of its edge underperforming across the board. AUD briefly trades with a 65c handle, but opens the new week just above 66c.

COVID-19 news remain front and centre in investors’ minds with a jump in news cases reported outside China, from South Korea, the Middle-East and Italy. News over the weekend will not have helped sentiment as we begin the new week, with the number of cases surging to over 600 in South Korea and over 130 in Italy. Extraordinary containment measures are being implemented, which will increase the hit to the global economy. Worryingly too, China reported 630 new cases in Hubei with new 96 deaths, effectively denting the recent narrative that China’s containment were showing to be effective.

Data on Friday night didn’t help the cause either. Japan’s manufacturing PMI sank to its lowest level in more than seven years to 47.6 vs 48.8 previously while the service PMI fell back into contractionary territory from 51 to 46.7. PMI data in Europe was better than expected with the German Manufacturing PMI printed at 47.8 vs 44.8 expected. So a bit better, but still in contractionary mode. Overall, there are signs of EC domestic demand and activity is finding a base, but exports remain challenged and clearly the full impact from COVID-19 to date is yet to be reflected in the data.

The above was just a prelude to the big data disappointment on Friday, both US PMI indices printed below expectations (see details below) with the Services PMI falling to 49.4 in February vs. at 53.4 print expected. The Markit PMI US composite, an indicator usually ignored by the market given the preferred ISM indicators, fell by nearly 4 points to 49.6. This was the lowest level in over six years and driven by the services sector, questioning the insulation of the US economy from the impact of COVID-19. Worth noting here, however, that the ISM Non-Manufacturing survey has a larger sample, it is the preferred index for the US, it was at 55.5 in January and the Markit PMI survey also has a bias for globally focus companies rather than domestic. The February ISM Non-Manufacturing is out March 5.

The data was a wake-up call for the US equity market, hitherto complacent about the impact of the virus. US equities fell, with the S&P500 down by over 1% and the Nasdaq index down by a greater 1.8%. Earlier in the session, the Stoxx Europe 600 Index fell 0.5% taking it weekly loses to 0.57%. Looking at the weekly performance, it was a bad week for most equity markets US, Europe and Japan all down for the week, making China a massive outlier with the Shanghai composite up 4.21%.

The US data disappointment bull flattened the UST curve with the US 30-year bond falling to a record low of just over 1.88%, before closing the week at 1.915%. The 10-year rate closed down 4bps to 1.47% after falling to as low as 1.435%, breaking previous support at 1.50%. The Fed Funds curve now prices in nearly two full rate cuts this year and the risk of another cut next year.

The move lower in UST yields weighed on the big dollar with the DXY index down 0.60% to 99.26 while BBDXY was -0.35% to 1214.22. The USD lost ground against all G10 pairs with SEK the big winner, up 1.00% followed by GBP up 0.64% to 1.2943 while the euro regained all of it prior losses for the week, closing around 1.0850 (now at 1.0832).

The NZD made a new year-to-date low of 0.6303, but the turnaround in the USD saw a sharp rise to close the week around 0.6350. The AUD followed a similar pattern, rising from an 11-year low of 0.6586 to close the week near 0.6625. AUD has started the new week just above the 66c mark.

We think it is probably too early to throw the towel on the USD. Yes, Friday’s data was disappointing and US equity markets were in need of COVID-19 wakeup, still we are likely entering a period of messy and potentially misleading data releases. The US had a bad data day, but we think that is just a taste of what is yet to come with other major economies likely to show bad economic numbers too. Unless hard economic data shows the US economy is underperforming others, USD weakness is unlikely to be a sustained theme over the coming weeks.

JN: CPI ex fresh food, energy (y/y%), Jan: 0.8 vs. 0.8 exp.

GE: Manufacturing PMI, Feb: 47.8 vs. 44.8 exp.

GE: Services PMI, Feb: 53.3 vs. 53.8 exp.

EC: Manufacturing PMI, Feb: 49.1 vs. 47.4 exp.

EC: Services PMI, Feb: 52.8 vs. 52.3 exp.

UK: Manufacturing PMI, Feb: 51.9 vs. 49.7 exp.

UK: Services PMI, Feb: 53.3 vs. 53.4 exp.

US: Markit Manufacturing PMI, Feb: 50.8 vs. 51.5 exp.

US: Markit Services PMI, Feb: 49.4 vs. 53.4 exp.

US: Existing home sales (m), Jan: 5.46 vs. 5.44 exp

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

Economic and financial market update

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.