On a seasonally adjusted basis, the NAB Online Retail Sales Index recorded a drop in growth in July

Insight

Markets have been hit with a triple whammy – disturbing COVID-19 numbers emerging from the United States, a worse than expected downgrade to global growth forecasts and a big rise in oil inventories.

“My my; At Waterloo Napoleon did surrender; Oh yeah; And I have met my destiny in quite a similar way; The history book on the shelf; Is always repeating itself” ABBA 1973

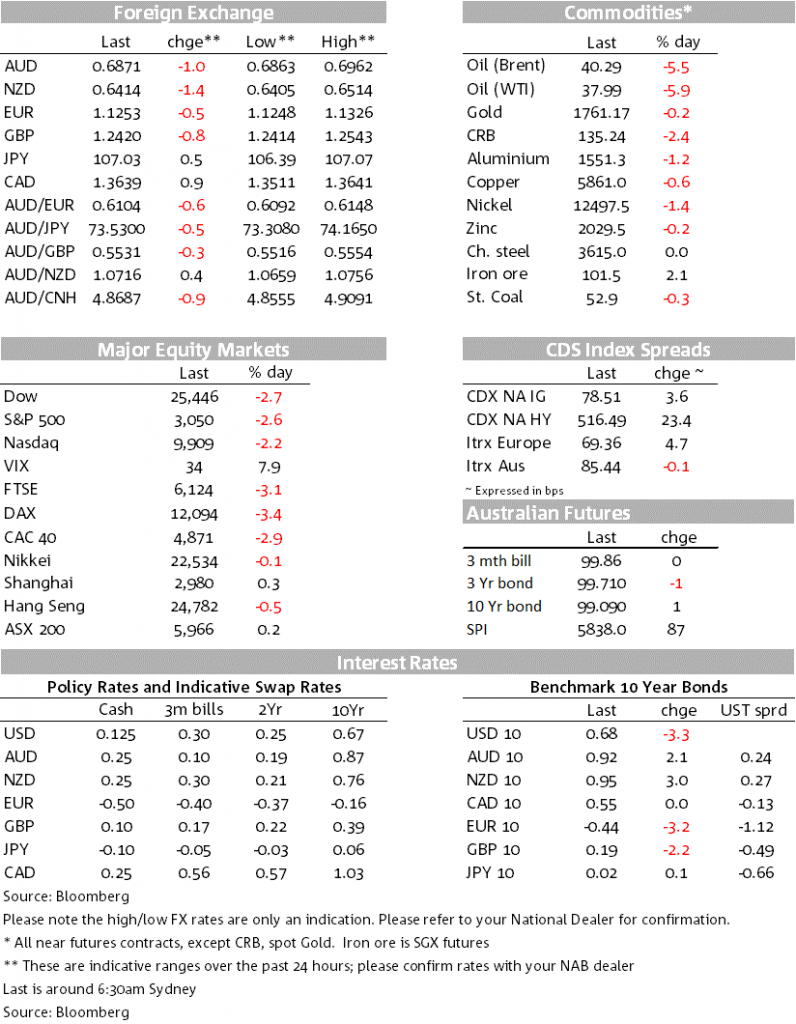

Risk sentiment reversed sharply overnight as virus cases rise in the US endanger the pace of the tentative recovery seen in the data to date. Also weighing were three other developments: (1) The US outlining $3.1bn in proposed tariffs on the EU in retaliation for Airbus subsidies (consultation period to July 26); (2) EIA oil inventories rose by 1.4m barrels v 0.3m expected and casting doubt on the speed of the recovery; and (3) the IMF downgraded global growth forecasts again to -4.9% from -3.0% in 2020, while also forecasting a less sharp bounce back with 2021 growth of 5.4% from 5.8% previously.

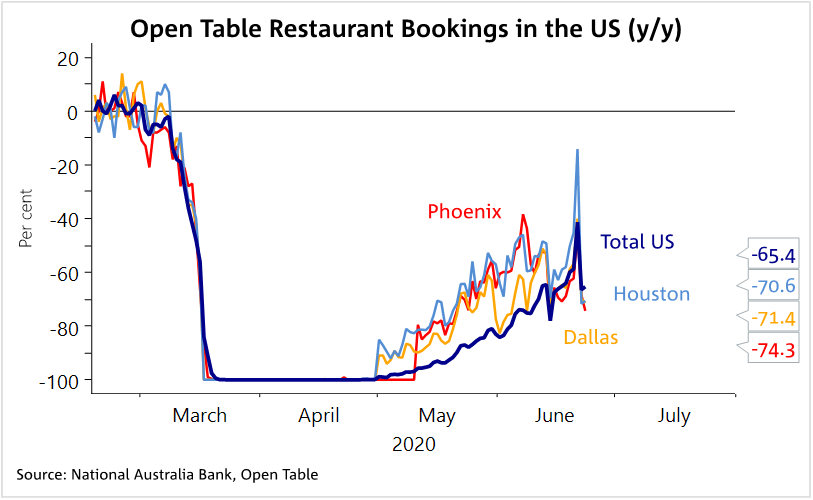

We had been noting for some time that markets were trying to grapple with the implications of rising virus cases given the high bar to re-impose restrictions. What changed overnight were signs of companies and consumers appearing to act ahead of officials with Open Table restaurant bookings diving in cities seeing a rise in the virus and Nike saying it was closing seven stores in the Houston area (see Chart above). State governors have also changed their rhetoric, becoming more worried on the virus – e.g. Texas Governor Abbott said there was a “massive outbreak” and that he was now “looking at greater restrictions and some could be localized…to make sure that hospital beds will be available”.

Equities fell sharply with the S&P500 -2.6% to 3,050. Energy stocks underperformed with the S&P500 energy sub-index -5.5% in line with the sharp decline in oil prices (WTI -5.9% to $37.99 a barrel). The USD rose with the DXY +0.5% with weakness seen across all pairs with EUR -0.5%, GBP -0.8% and USD/Yen +0.5%. G10 global growth proxies were down sharply with the AUD -1.0% and NZD -1.4% and reinforcing the high correlation between the antipodean currencies and risk sentiment as seen in the stock market. The NZD was also weighed down in the aftermath of the RBNZ announcement yesterday, and although inline with expectations suggests some in the market were looking for a more positive statement. As for the RBNZ an easing bias remains and is prepared to provide additional stimulus as necessary. More guidance on the outlook for the $60b QE programme and “readiness to deploy alternative monetary policy tools” will be outlined in the August Monetary Policy Statement. Comments on the NZD remained factual and non-judgmental about its value, with the Bank simply acknowledging its recent appreciation and negative impact on export returns.

Bonds rallied with the US 10yr yields -3.3bps to 0.68%. Also in rates news, there was strong demand for Austria’s €2bn 100yr bond with bids of more than €17.7bn and issued with a yield 0.88% (note the first 100yr bond have seen returns of up to 85% since 2017!) Fitch downgraded Canada’s credit rating to AA+ from AAA citing the deterioration in finances associated with the pandemic.

New case numbers of the coronavirus are accelerating across the US, with 33 states showing increased growth compared to two weeks ago, with notable rises in the South and West. While this is not new news, the pace of the acceleration is causing businesses and consumers to act with Open Table showing restaurant bookings have dived in the southern US (see Chart above). Officials are also starting to take action with New York, New Jersey and Connecticut now requiring visitors from hot spots to quarantine for 14 days. State governors in the southern states who have been reluctant to reimpose restrictions have also sharply changed their rhetoric. Texas’ Governor Abbott said there was a “massive outbreak” and that he was now “looking at greater restrictions and some could be localized…to make sure that hospital beds will be available”. These trends threaten the pace of the tentative recovery seen in the data to date. The US is of course not the only region showing increased growth in cases. At home in Australia Victoria has re-imposed some restrictions as well as asking for military resources. The increase in cases and the possibility of restrictions (even if localised) does threaten the recovery seen in consumer sentiment – panic buying has been seen in Melbourne and one supermarket in Sydney was empty of toilet paper and pasta last night.

The US has proposed new tariffs of $3.1bn on European goods, subject to a consultation period that ends on July 26. This comes ahead of a ruling by the WTO on whether the EU can legally impose tariffs on $11b of US goods in retaliation for US subsidies to Boeing. It is a reminder that US-EU trade frictions remain.

Data overnight was sparse with only the German IFO of significance, which rose broadly in line with expectations (business climate 86.2 v 85.0 expected). On a more negative note, the IMF downgraded its global growth outlook from its forecasts of just two months ago, picking a contraction of 4.9% this year (previously minus 3.0%) and a rebound of 5.4% next year (previously 5.8%), but now seeing both upside and downside risks around these forecasts.

Another quiet day in Australia with only second-tier job vacancies which are likely to be dated given the uptick seen in online job advertising over recent weeks. Across the ditch the NZ trade balance is out, while international focus will likely be on US jobless claims and durable/capital orders. Key releases in detail below:

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

On a seasonally adjusted basis, the NAB Online Retail Sales Index recorded a drop in growth in July

Insight

Firmer consumer and steady outlook

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.