NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Risk-on continues in the wake of Wednesday’s FOMC meeting as investors price the aggressive monetary hiking cycle as being closer to the end.

Key event/headlines

GE: Unemployment rate (%), Oct: 5.8 vs. 5.8 exp.

UK: Bank of England Bank Rate (%), Nov: 5.25 vs.5.25 exp.

US: Nonfarm productivity (% an), Q3: 4.7 vs. 4.3 exp.

US: Unit labour costs (% an), Q3: -0.8 vs. 0.3 exp.

US: Initial jobless claims (k), 28-Oct: 217 vs. 210 exp.

US Factory Orders Sep: 2.8% vs. 2.3% exp.

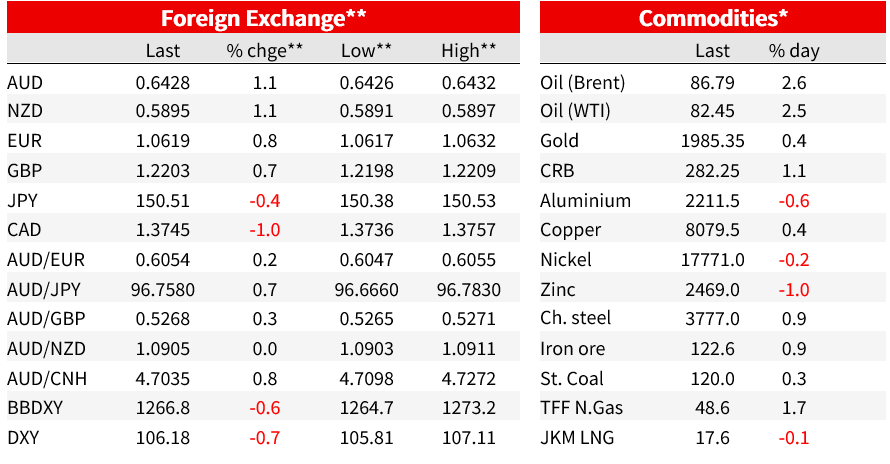

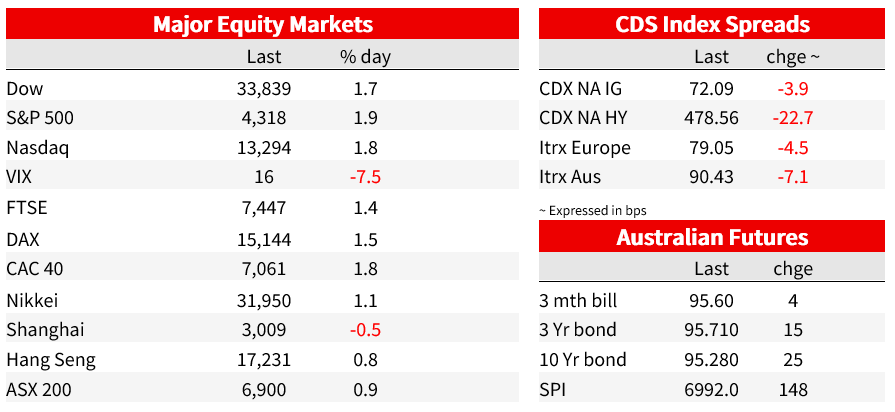

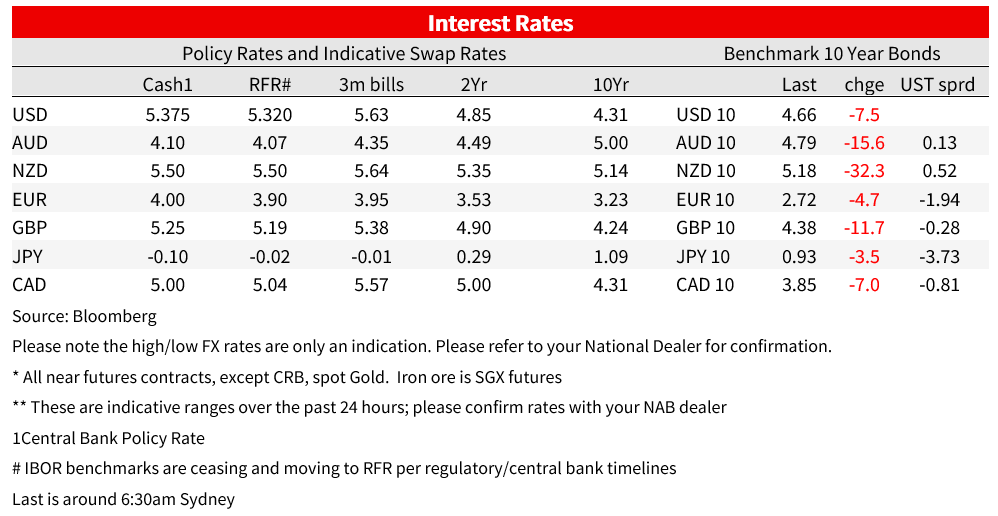

Markets have extended rate cut pricing in 2024 to ‑88bps from the ‑76bps seen on TuesdayM, while there is only a 31% chance of a rate hike by January 2024. The yield curve is bull flattening with 2/10s sitting at -30.7bps from the -16bps it was on Tuesday. Greater yield declines have been seen in 10yrs (-6.9bps overnight, and -23.1bps since Tuesday to 4.67%) than in 2yrs (+3.9bps overnight, but -10.9bps since Tuesday to 4.98%). Equities have rallied sharply with the S&P500 up 1.9% overnight, after having risen 1.0% on Wednesday. The USD (DXY) fell a further -0.7%, though pared moves a touch as front-end Treasury yields moved higher. The AUD (+1.1% to 0.6431), NZD (+1.1% to 0.5896) and USD/CAD (-1.0% to 1.3756) led gains amid USD weakness. Other majors: EUR +0.9%, GBP +0.8%, USD/JPY -0.5%. Commodities mixed (copper +0.4%, Brent oil +2.6%).

It was the BoE’s turn overnight with rates left on hold at 5.25% for the second consecutive month which was in line with expectation s. The central bank expects that policy settings will need to remain at restrictive levels for an extended period of time. The monetary policy committee vote was split 6-3 with the minority favouring a further 25bp increase. Governor Bailey said that the bank is ‘watching to see if more rates hikes are needed’ and that it is much too early to be thinking about rate cuts. Market pricing for the BoE base rate was little changed following the policy decision. There is about 7bp of tightening priced by February next year. The pound made modest gains against the euro in the immediate aftermath of the rates decision before retracing (EURGBP +0.1%, at one point +0.5%). The Norgesbank also met overnight, keeping rates on hold and although they signalled the potential of a December hike EUR/NOK rose 0.3%.

The dataflow was supportive for the notion of a soft landing and the end of the US hiking cycle being nearer . US initial jobless claims rose slightly more than expected to 217k vs 210k consensus, which is still at very low levels but is a seven-week high. Continuing claims, a proxy for people receiving unemployment benefits, increased to the highest level since April to 1,818k vs. 1,800k expected. Note the 2019 average for continuing claims was 1,699k so it may point to people remaining on benefits longer, even if inflows into benefits remain very low. The other interesting bit especially for the soft landing narrative was a pickup in Q3 productivity at 4.7% vs. 4.3% consensus and 3.6% previously. This meant unit labour costs declined in Q3 at -0.8% vs. 0.3% expected, after Q2’s more worrying 3.2%.

In Japan PM Kishida announced a stimulus package to reduce the impact of high living costs on households, help firms raise wages and offer also support for domestic investment and growth. The measures total more than 17 trillion yen (US$113 billion) and will be funded by a supplementary budget for the remainder of the fiscal year to March 2024. A Reuters article citing government sources that directly interact with the central bank indicated the Bank of Japan Governor Ueda will continue to dismantle the ultra-easy monetary policy settings. This follows the decision earlier this week to pullback from 1% being a rigid topside limit for 10-year JGBs as part of the yield curve control framework. The Yen was little changed on the news report while 10-year JGBs yields ended the day down 3bps at 0.91%.

Finally in Australia, some hints from RBA whisperers in the press of not to expect informed whispers ahead of RBA meetings. James Glynn of the Dow Jones/WSJ reported late yesterday: “another factor making the decision a ‘line ball call’ is that the bank is under new management, a change that has brought a significant shift in style. The new governor, Michele Bullock, appears much less likely to drop big hints about the direction of interest rates than her predecessor, Philip Lowe”. Overall “ board meetings from here on out are likely to be a little more uncertain as Bullock moves cautiously in public while–quite correctly–seeking to consult with and listen to other board members. A further rise in the cash rate next week is a possibility, but Bullock will let the board speak on the matter first”. (see WSJ: Glynn’s Take: RBA Policy Decision Seems Too Tough to Call With Cautious Bullock at the Helm). Meanwhile the government appears intent on banking most of the revenue windfall and thereby not adding further to inflationary pressure ( AFR: Albanese draws a line under cost-of-living assistance).

Coming up:

Market Prices

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Confidence and Conditions Lift

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.