Our global forecasts are unchanged and we continue to expect soft global growth of only 3.0 to 3.1% between 2024 and 2026.

Insight

There was a reversal of fortunes on Friday as the NY Fed clarified comments from their President John Williams the day before.

https://soundcloud.com/user-291029717/cuts-out-of-context?in=user-291029717/sets/the-morning-call

Hey, what did you hear me say..Yes, I said it’s fine before, but I don’t think so no more…I’ve changed my mind, I take it back, Erase and rewind – The Cardigans

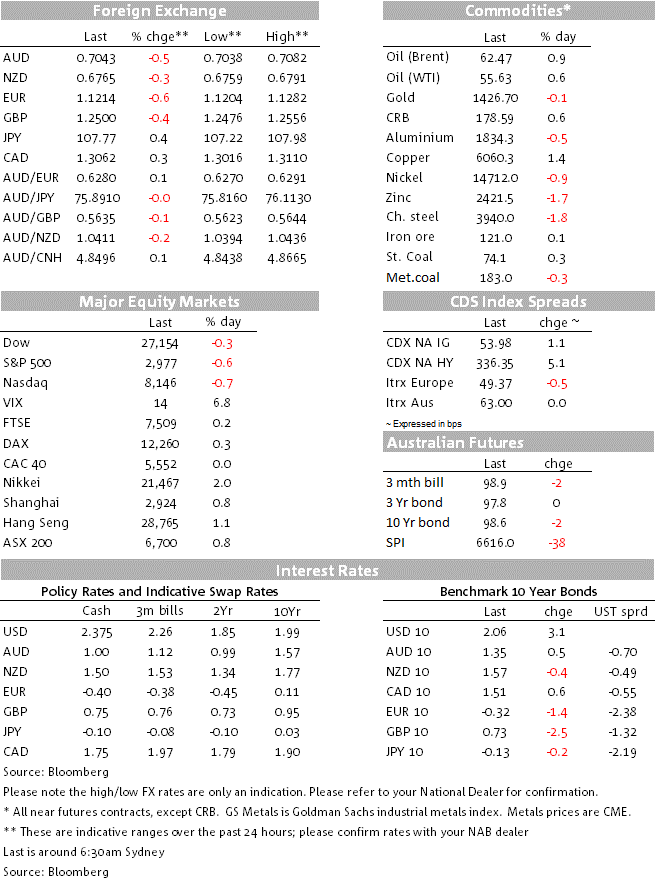

Friday’s overnight session was a game of two halves for US equities in particular. A relatively quiet first half with markets leaking their wounds following Fed Williams’ faux pas on Thursday, then a risk off second half courtesy of news Iran had seized a UK flagged vessel and a WSJ article asserting the Fed intentions of just 25bps of easing by the end of the month. The WSJ article contributed to a bear flattening of the UST curve that was already evident at the start of the session and the USD ended the day broadly stronger with the SEK and EUR the notable underperformers. AUD and NZD lost ground on Friday, but ended higher on the week, especially the kiwi. Oil prices were on a slide ahead of the Iran news but ended back on the black. After briefly trading above $1450 early on Friday, gold close the week at $1426.5

After falling heavily on Thursday following Fed Williams comments that “when you only have so much stimulus at your disposal, its pays to act quickly to lower rates at the first sign of economic distress”, the USD spent most of Friday clawing its way back to pre-William’s levels with the DXY index ending the week at 97.151, after trading down to just under 96.70 early in our Friday morning. The change in USD fortunes was triggered by a loud truck like reversing sound – beep, beep ! from a NY Fed spokesman aimed at clarifying that William’s speech was ‘not about potential policy actions at the upcoming FOMC meeting’ and that his speech today was ‘academic…based on research’. Fair enough, but once we consider the point that Fed Williams is one of the few inside the Fed inner circle along with the fact that we are entering a black-out period ahead of what it looks like an almost certainty that the FOMC will embark on a new easing cycle at the end of the month, then from a perfect hindsight perspective, it’s seems pretty obvious that a nervous market, grappling with whether or not the Fed will cut by 25 or 50bps, a “theoretical comment” like that was only going to end with market increasing the chances of a 50bps fund rate cut.

So the clarification triggered a repricing in UST rates and the USD with Fed President Bullard, one of the most dovish members on the FOMC, chiming in saying that he saw a 25 BP as the appropriate and likely outcome. Driving the case for a 25bps cut, the WSJ run a categorical article Friday night noting Fed officials are prepared to lower interest rates by 25bps later this month, adding that “officials aren’t prepared for bolder action now”. Not to be outshone , President Trump in a pair of Tweets said that he preferred Mr. Williams’s “first statement much better than his second.” , repeating his call for the Fed to cut rates aggressively: “Don’t blow it!

The UST curve bear flatten on Friday with shorter dated yields lifted on the back a repricing in Fed rate cut expectations. Early on Friday a 50bps Fed rate cut by the end of the month was priced around 70% priced, before easing back down to 30%. 2y UST yields, which closed at1.75% on Thursday, moved up to 1.83% at one stage on Friday morning before ending the day at 1.82% meanwhile the 10-year tenor rose 3bps to 2.05%.

The DXY and BBDXY USD indices, retraced all of their Fed Williams induced losses and ended the week back to levels seen just before the close on Thursday. From a technical perspective the DXY index bounce back above its 200DMA, easing some concern of over the potential for an acceleration in USD weakness. That said, Friday’s repricing was not strong enough to break the downtrend in the USD that has been in place since late May. Our sense is that the Fed will embark on a new easing cycle at the end of July announcing a 25bps cut to the funds rate, but key for the USD’s near term outlook will be the message imparted by the FOMC at its policy meeting. Any hint that more rate cuts are in the offing will likely keep the USD on the back foot, NAB sees the Fed cutting again in November with the risk that more will be needed.

The AUD fell 0.43% on Friday closing the week at 0.7042, but still showing a 22bps gain for the week. From a technical perspective the AUD remains in an uptrend, but the 200DMA currently at around 0.7090 remains a solid obstacle for significantly higher levels. Friday’s CFTC data revealed the speculative community unwound a little bit of its AUD short positioning, but at -52.2k there is still the potential for AUD upside from short covering. It’s a quiet week in the domestic data front and although RBA Governor Lowe speaks on Thursday, but we don’t expect to learn anything new in terms of near term policy from the Governor. Focus will remain on offshore events and on the USD performance ahead of the FOMC meeting at the end of July. See more below.

The NZD ended the week around 0.6760, after reaching as high as 0.6790 in the aftermath of the Williams speech. This capped off a weekly gain of just over 1%, making the NZD the strongest of the majors for reasons that aren’t all that convincing. Small gains were made on most of the crosses.

Looking at other major currencies, the euro lost 0.5% on Friday closing the week at 1.1214. The union currency remains in a 1.12-1.13 range and ahead of the ECB meeting on Thursday the market has increased the probability of a 10bps ECB cut to the deposit rate to 50%. GBP was little changed on Friday, but after trading down to 1.2385 midway through the week, cable is now back at 1.2491 ahead of what could potentially be a tricky week with the UK finally getting a new PM on Tuesday (see more below).

News that Iranian forces had seized a British-flagged oil tanker in the Strait of Hormuz also sour the mood before the NY close. According to Iranian official the British vessel had collided with a fishing boat. A second British vessel was also boarded by Iranian armed personnel, but later freed on Friday. Iranian action occurred only hours after a court in the British territory of Gibraltar extended the detention of an Iranian oil tanker seized earlier in July. Tensions between Iran and the West continue to escalate with the tit for tat increasing in magnitude and thus increasing the risk of someone making an overstep leading to a military conflict, notwithstanding the fact that Iran, the US and its allies continue to say that they do not want a conflict.

US equities range traded on the early part of Friday’s NY session with a solid earnings report from Microsoft unable to lift the market. Then as the Fed repricing gathered momentum in UST yields and USD, US equities began to falter not helped by Iranian news. The S&P 500 closed Friday 0.62% lower and the NASDAQ fell 0.74%. For the week, the S&P 5000 fell 1.23% and the NASDAQ dropped 1.19%.

In economic data, the University of Michigan consumer sentiment index rose slightly, close enough to consensus, and maintaining a historically high level. Inflation in Japan remained low, with the BoJ making little progress in driving inflation towards its 2% target despite its ultra-easy policy settings.

Oil prices ended the week on a positive note (Brent crude up almost 1%), breaking four days of losses and trimming the weekly loss to about 6%, with concerns about slowing demand predominating over much of the period. After briefly trading above $1450 early on Friday, gold close the week at $1426.5

JN: CPI ex fresh food, energy (y/y%), Jun: 0.5 vs. 0.5 exp.

CA: Retail sales ex auto (m/m%), May: -0.3 vs. 0.4 exp.

US: U. of Mich. cons. sentiment, Jul: 98.4 vs. 98.8 exp

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Our global forecasts are unchanged and we continue to expect soft global growth of only 3.0 to 3.1% between 2024 and 2026.

Insight

Conditions ease as slow growth weighs on firms

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.