Online retail sales growth slowed in May following a fairly strong April

Insight

Even though trade talks are still going ahead between the US and China this week, what little hope of any sort of outcome, seems to be rapidly diminishing.

https://soundcloud.com/user-291029717/deals-are-falling-off-the-table?in=user-291029717/sets/the-morning-call

The Peter Lee surveys are now taking place. If you have appreciated NAB’s research support please let your company’s representative know.

This is my quest, to follow that star, no matter how hopeless, no matter how far. To fight for the right, without question or pause, to be willing to march into hell for a heavenly cause – Boris Johnson Andy Williams

Fed Chair Jerome Powell has just spoken and is at pains to say that while the “time is now upon us to expand the balance sheet” that the “growth of the balance sheet for reserves purposes should not be confused with QE”. We’ll concede to him on this, given the at times acute resurgence of money market funding pressures in recent weeks which to date the Fed has dealt with via short term open market operations. Now a more permanent fix is at hand via the outright purchase of Treasury Bills.

Powell says that the Fed will act as appropriate, is not on a pre-set course (the latter a familiar Janet Yellen refrain) and will assess the outlook on a “meeting by meeting” basis. Powell repeats that global developments are the main risk to an otherwise positive outlook, but acknowledges these are impacting on business investment as well as manufacturing and trade. On the former, last night’s NFIB (small business) survey confirms a fairly dire outlook, with the capital spending intentions index – a good lead indicator of non-oil related capex, now into negative yr/yr terrain. The overall NFIB index fell to 101.8 from 103.1, not a disastrous level but confirming an ongoing downtrend and with trade concerns identified as the prime culprit.

US producer prices showed unexpected weakness (the Final Demand measure -0.3% against +0.2% expected and pulling the yr/yr rate down to 2.0% from 2.3%). No tariff impact here, though one explanation is a big fall in wholesale and retail profits margins – possibly just noise but it could mean firms are unable to pass on the impact of higher tariffs and instead are enduring a profits squeeze.

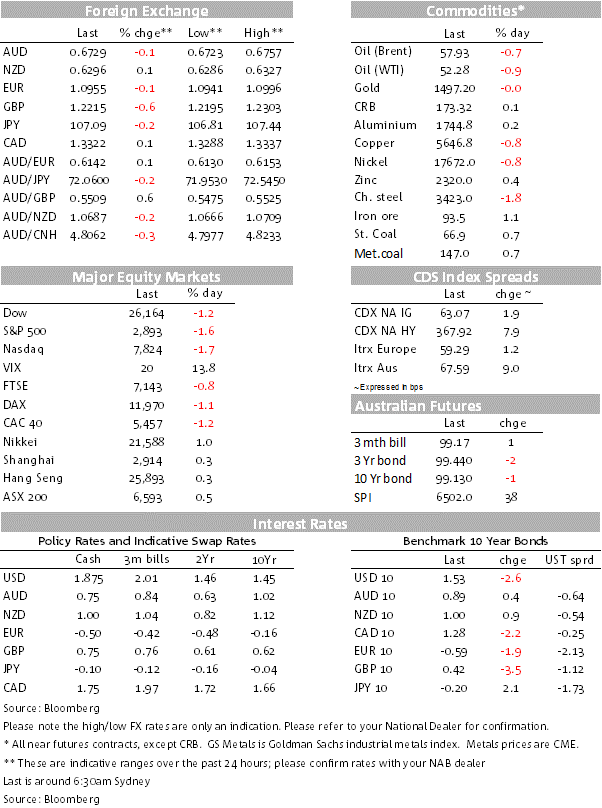

US stocks undertook a small blip up then back down post-Powell, 2 year Treasury yields are some 4bps lower (presumably on the balance sheet news) and 10s a lesser 1-2bps. The bigger (negative) impact on stocks and bond yields came at the open, on increased pessimism at any prospects for a breakthrough at the trade talks scheduled to resume in Washington tomorrow and featuring chief China trade negotiator, vice-Premier Liu He. This was on the the news that greeted us yesterday morning that the US was adding 8 more China technology companies to the so called banned entity list – and 28 Chinese public security bodies in total, citing – for the first time – human rights violations (of Muslim minorities in at least one Chinese province) rather than just national security concerns as has been the case to date.

To this developments we can now add a renewal of the suggestion that the US administration is looking to interfere in US investments in Chinese equity markets, with reports that government pension funds might be banned from doing just this, and that the government may be looking to lean on the index providers with regard to their progressive increase in the number and weight of Chinese stocks in their various indices (MSCI is in process of increasing the weight of China A shares in its EM index from less than 1% to just over 3% by November 2019). This is all very sketchy at this stage, but evidently unnerving.

US indices have just closed with the S&P 500 down 1.6%, the Dow -1.2% and the NASDAQ 1.7% lower. Financials have led the decline in the last ‘hour of power’, its S&P sub-index down by more than 2%, apparently on perception of interest rate margin compression according to one of our New Yok colleagues. US Treasuries are coming into the last hour of New York trade with 2s -4.4bps at 1.419% and 10s -2.6bps at 1.532%

GBP is the biggest mover by far, off 0.6% after UK PM Johnson said the a Brexit deal was ‘nearly impossible, following an early morning phone call with German chancellor Angela Merkel at which she was reported to have insisted that Northern Ireland remain inside the EU Customs Union (pending any new trade arrangement that obviated the need for a border with the south). This doesn’t to our mind materially increase the risk of a no-deal Brexit on October 31st, with an extension and early elections still by far the most likely scenario. However, as my London Gavin Friend points out, it’s worth noting that the Conservatives poll standing has been improving of late, and that as such no-deal Brexit odds following an election that brought either an outright Tory victory or the ability of the Tories and the Brexit Party to muster a majority, is on the rise. More nervous week ahead for all things GBP, through NAB’s FX Strategy team did nudge up its GBP forecasts yesterday to better reflect the diminishing risk of a no deal Brexit on October 31st.

The NZD has given back part of its APAC session gains (which followed news of a stronger than expected CNY fixing on the first day back from the Anniversary holidays) but is still just up on 24 hours earlier. The AUD is just in the red at 0..6731. There was no reaction yesterday to the latest NAB business survey, which showed Business Conditions recording a sixth consecutive below-average month, pointing to ongoing weakness in the business sector. In the month, conditions edged up 1pt and confidence edged lower. While both conditions and confidence remain below average levels +6 index points – the broad-based trend decline since mid-2018 appears to have slowed. In the month, profitability and trading conditions remained below average, contrasting with the employment index, which edged up and is now above average. This mirrors official data that show ongoing strong employment growth but subdued consumer spending.

Locally, Westpac consumer confidence is at 10:30 AEDT – its was last at a subdued 98.2.

Not much offshore this evening, just US JOLTS (job openings) and September FOMC minutes (5:00 AEDT Thursday), the latter already superseded by Powell’s remarks just now.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.