NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

US equities have climbed as the US goes through Wednesday without a clear winner in the election.

https://soundcloud.com/user-291029717/divided-they-stand?in=user-291029717/sets/the-morning-call

Victory, till Victory, Victory, till Victory – Patti Smith

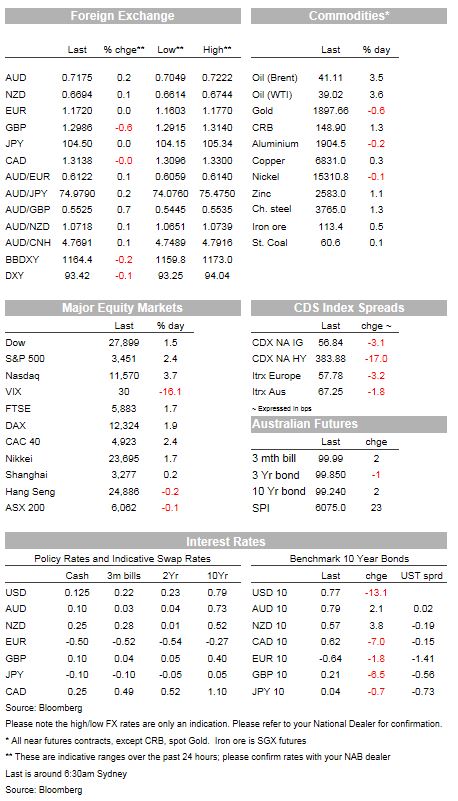

The Australian market wakes up to find we are really no further forward regards knowing the US election result than when we were when most of us went to bed last night. When I did, the current Electoral College count from seats that have been called by the media stood at 238-13 (for those willing to call Kansas for Biden) an it is the same this morning.

The stats of Wisconsin, Michigan, Pennsylvania are still in play, while in the south North Carolina and Georgia are still in the balance. In the west, ballot in Nevada are still being counted. President Trump has just been reported as filing a court claim for the Michigan vote count to be stopped and demanding a recount, while Wisconsin has just been called for Biden by The Associated Press. In the betting markets, Biden is now being given about an 80% change of victory – early yesterday afternoon, Trump’s was afforded similar odds of winning!

The failure so far of the Democrats to win any of the ‘toss-up’ seats currently held by Republicans, or to defeat either Lindsey Graham in South Carolina or Susan Collins in Maine (both considered winnable by the Democrats) has greatly diminished the chances of them wresting control of the Senate (currently held 53-47 by Republicans). This might yet come down to the run-off special election in Georgia on 5 January, five days before the new Senate is due to be sworn in.

After what was the proverbial roller-coaster across markets during our time zone yesterday, with some wild gyrations in US equity futures, AUD/USD trading a range almost as wide as the whole of October and US bond yields some 8bp lower at 10-year on the diminished prospect of the ‘blue wave’ and with that sharply expanded fiscal deficits, equity market have now decided they like the prospect of a ‘do nothing’ President, lacking control of both houses of Congress – in which resect history is on their side. This view will though, remain contingent on some sort of covid-19 related fiscal package being agreed, ideally sooner rather than later, in which respect current Senate leader Mitch McConnell, fresh from re-election in his Senate seat, has been out saying “we need to do a stimulus bill before the end of the year”.

The S&P 500 was up 2.9% and the NASDAQ 4%. A feature of yesterday’s trade and overnight was a reversal of the ‘rotation trade’ out of ‘Big Tech’ (on regulatory and tax concerns) and into stocks seen most likely to benefit from large-scale US fiscal stimulus under the blue wave scenario.

European stock closed with gains of 2-2.5% for the FTSE100, DAX and CAC40 (gains, arguably much more consistent with a Biden victory than Trump re-election, the latter with its attendant risk of the President persisting with his attacks on European allied and threatening tariffs on German cars imports, etc.).

Bond markets have seen the sharp rally in our time zone yesterday extend, with 10-year Treasury yields now down 14bps on Tuesday’s closing level at 0.76%. This looks to be much more to do with the virtual evaporation of prospects for massive fiscal stimulus and sharply expanded budget deficits in the year ahead than the uncertainty factor regarding the election result – otherwise US stocks would not be where they are.

The DXY index -0.15% and BBDXY -0.18%. This is despite a 0.5% fall in GBP/USD and where reports suggest that some serious differences remain in EU-UK trade talks (currently not yet back underway). EUR/USD and USD/JPY, the other big index contributors, are little changed, as too USD/CAD. AUd/USD was on a particularly wild ride yesterday, trading clear above 0.72 earlier on (high of 0.7220) and then down to a low of 0.7049 when the uncertainty/fear factor gripped market regarding the election outcome.

The rebound in risk sentiment, and view that the USD is most likely headed lower post-election, sees it back to 0.7180 as I type. NAB FX Strategy teams’ 70-74’ forecast range for AUD/USD through year held since mid-year, continue to look on the money.

Both the US ADP private payrolls and US ISM services indicators undershot market expectations. The ISM fell to its lowest level in five months (56.6 v 57.5 expected) and looks vulnerable to further falls, as COVID19 spreads across the US, disproportionately affecting the services sectors as tighter restrictions take force. The ADP report at 365k against 650k expected points to slowing employment growth.

The US election will be far from our minds and the market will be focused on the out-of-control COVID-19 spread in the US and associated negative economic implications.

ANZ November preliminary Business Confidence and Activity outlook. Australia has September trade balance (expected A$3.7bn vs $2.64bn in Aug).

Eurozone has German factory orders for September (expected +2.0% m/m), September retail sales and the EU Commission’s latest economic forecast.

The US has weekly jobless claims.

The Bank of England will be the main (non-political) offshore event, where the consensus looks for a £100bn increase in QE purchases to £845bn. The risk is skewed to a larger increase.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Confidence and Conditions Lift

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.