Total spending grew 0.9% in June.

A stimulus boost from the ECB is widely anticipated.

https://soundcloud.com/user-291029717/draghis-last-stand?in=user-291029717/sets/the-morning-call

The Peter Lee surveys are now taking place. If you have appreciated NAB’s research support please let your company’s representative know.

Compromise, sometimes lie, Get the Balance right, get the balance right – Depeche Mode

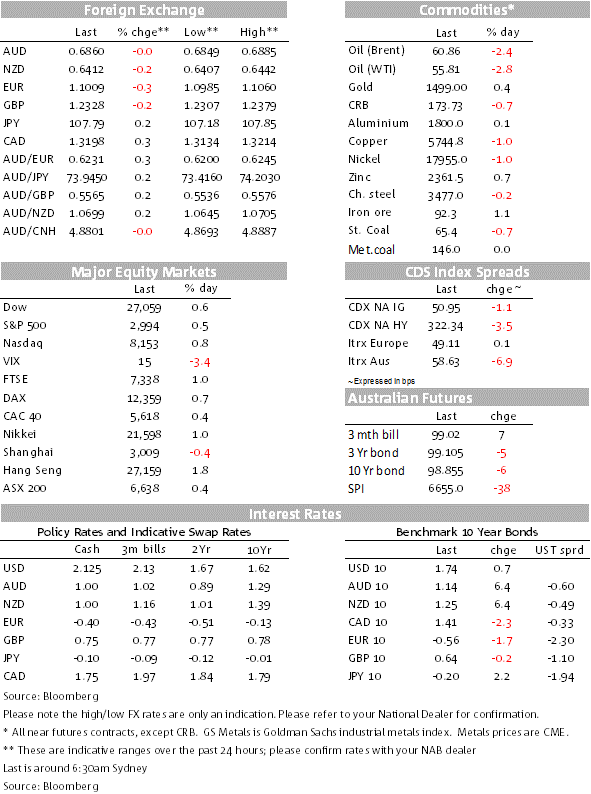

After a decent rise over the past couple of days, core global bond yields have taken a breather overnight and consolidate ahead of the ECB meeting and Draghi press conference tonight. US and EU equities are higher with technology shares the outperformers. Notable the NASDAQ closes above 1% after 3 consecutive days of negative returns. News President Trump is considering lifting Iran sanction and meeting Iranian President Rouhani also helps sentiment, dragging oil prices lower. The USD is broadly stronger amid softer euro and oil linked currencies while the AUD shows resilience and opens unchanged relative to levels recorded this time yesterday.

Ahead of the ECB tonight core global bonds have finally taken a breather after the aggressive repricing over the past few days that resulted in 10Y UST yields climbing 30bps from the lows recorded on September 4th (1.4422%) to 1.7437% currently. In a similar vein 10y Bunds now trade at -0.5640%, 1.5bps lower on the day, but 18bps higher relative to the lows reach on September 3rd .

Markets are shifting their attention to the ECB meeting tonight where there is a unanimous consensus for easing measures to be announced, but a great deal of uncertainty on what exactly these measures might entail. The consensus among economists is for a 10bp cut to the ECB’s deposit rate and the announcement of a resumption to QE, with the median estimate for a €30b per month pace of bond buying. The market prices 14bps of rate cuts in for this meeting, implying an almost 50% chance that the ECB could cut by 20bps.

We have sympathy with the 20bps deposit cut, but based on the number of ECB council members pushing back on the idea of a new QE programme, our senses is that the ECB will open the door to prospect of new QE programme, but it won’t necessarily officially announce one today. A greater consensus appears to be around the idea of a tiering system for bank reserves, whereby some portion of banks’ reserves will be exempted from the negative deposit rate, in order to mitigate the negative financial impact on the banking sector. We think this rather technical announcement will be very important to the reaction function tonight, without tiering, a more negative deposit rate will be a big burden for commercial banks.

QE or no QE is the other major focus, surveys suggest the market is expecting a new programme with the big follow up question of what the size?. The counter to this view is that after ECB Rehn talk of a significant easing package we have had a whole line of hawks including Weidmann, Knot, Nowotny, Lautenschlaeger, Villeroy, Muller and Holzman hosing down the need for sizeable stimulus, arguing in particular against a return to QE. The public disagreement on QE leaves us with a bias for the ECB to delay QE for now. Draghi might yet soothe opposition to re-starting QE, but this as a very close call.

Notwithstanding the recent rise in European and global rates, expectations for the ECB are still high (as evidenced by a 30 year German yield of 0%) and as such there is a risk that a no imminent QE announcement disappoints the market triggering an extension to the recent bond sell-off. Here what Draghi says will be very important, no QE but the promise of QE down the line alongside an increase in capital keys in order increase the potential for buying more sovereign bonds will be important. The potential of buying corporate bonds is also another consideration.

Another important mover in the overnight session, has been the decline in oil prices (over 3.5% from intraday highs) following news that President Trump discussed easing sanctions on Iran to help secure a meeting with Iranian President Hassan Rouhani later this month (also a key factor for the departure of National Security Advisor John Bolton).

So against a risk positive geopolitical factor, equity markets had a good night with both main EU and US equity indices ending the day with positive returns. Of note too, the Nasdaq index rose for the first time in four days with Apple’s shares up 3.18% the big move following news of a cheaper priced iPhone.

Moving on to FX, the USD has had a decent night with the DXY index up 0.30% to 98.63 and BBDXY +0.17% to 1210.84. Euro weakness ahead of the ECB has been on big factor ( -0.28% to 1.1010) while oil linked currencies ( CAD -0.33% and NOK-0.10%) have also underperformed. Meanwhile the equity risk positive environment also sees JPY ( -0.27%) and CHF (-0.10%) lower. Worth noting here that USD/JPY keeps on proving higher intraday levels, even with UST 10y yields consolidating over past 24 hours. The ECB announcement tonight is going to be a big deal for the near term prospect of USD/JPY.

The NZD and AUD received a short-term boost yesterday afternoon after the Global Times editor tweeted that China would take measures to ease the impact of the trade war. The NZD immediately moved up from 0.6410 to as high as 0.6439 and the AUD traded to an intraday high of 0.685. In the end, the absence of soybeans and pork in the exemption list, after media speculation that easing measures were imminent, was a bit of a disappointment. The AUD now trades at 0.6863 and NZD is at 0.6413.

At this point is probably worth noting to that we (NAB) have changed our call on RBA monetary policy. Previously we expected one more cut in November to 0.75%, together with additional fiscal stimulus. We now expect a further cut to 0.5% in February, at which point the Reserve Bank would outline its plans on unconventional policy. Unless the government delivers a meaningful fiscal stimulus, a further cut to 0.25% by mid-2020 is likely, along with the adoption of non-conventional monetary policy measures. More details from the note in your in box, also enclosed

China’s loan data for August was released late yesterday and while the headline beat expectations, the drivers painted a more underwhelming picture. Aggregate social financing expanded by ¥1.98trn, more than ¥1.01trn yuan in July and above the consensus forecast of ¥1.604trn. A sharp decline in undiscounted bankers’ acceptances was seen as the main driver for the bigger than expected number, so not necessarily a positive story in terms of financing prospects.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.