Online retail sales growth slowed in May following a fairly strong April

Insight

The ECB announced it will extend its bond buying program by a further €600b.

Tap it, tap it, slap it on the floor, Hey you really got me humming, Don’t you keep my motor running – Jerry Lee Lewis

With politics inside the Beltway looking increasing fractious (possibly not unrelated to the tumbling odds on President Trump winning a second term of office) European policy makers have picked up the baton with respect to more policy stimulus – both monetary and fiscal. This is showing up more in currencies (a weaker USD, stronger EUR) than it is in equities, where US stocks have just closed with the S&P down 0.34% and the NASDAQ -0.7%.

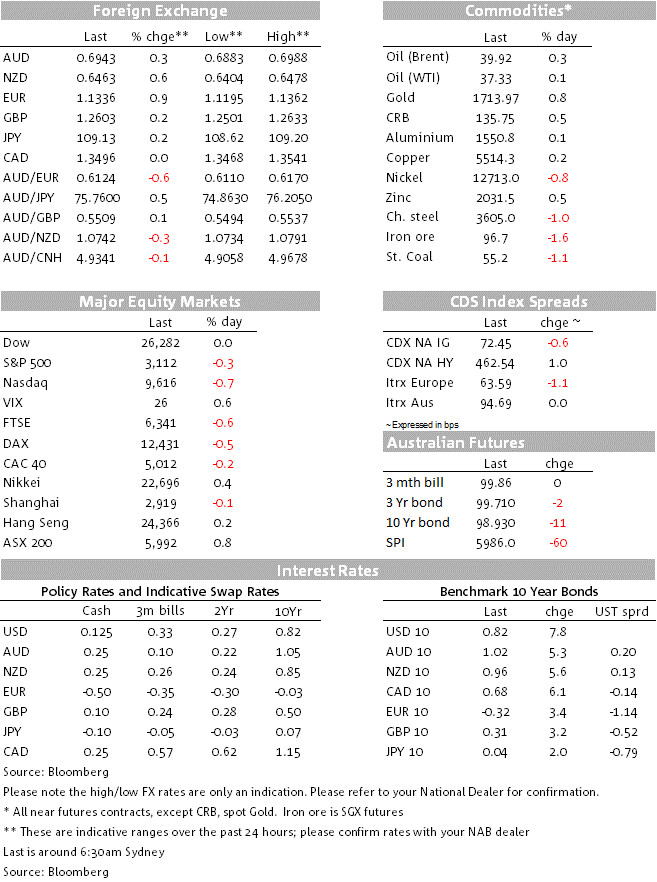

The ECB over-delivered on market expectations, expanding its Pandemic Emergency Purchasing Programme (PEPP) by €600b to €1.35tn, some €100bn above the top end of market expectations and defied the suggestions of folk like ourselves who argued that the ECB could hold fire for now, tactually, in the hope of keeping the pressure on the politicians to secure agreement on the size and form of the proposed EU Recovery Fund. On the latter, hopes of early agreement have been dealt another knock by news that Finland has joined the ‘frugal four’ (Austria, Netherlands, Sweden and Denmark) in opposing debt mutualisation and the distribution of the proceeds of the Fund largely in the firm of grants.

ECB bond buying will now extend though at least June 2021 and the reinvestment of maturing assets though to at least June 2022. The ECB won’t, for now, even be constrained by the so called Capital Key governing how much of each Eurozone countries’ bonds it can buy, until it gets into the re-investment phase of the programme. The Italian bond market loved the message, 10-year BTP yields falling by 13.3bps to 1.20% partly at the expense of German Bunds (+3bp to -0.33%). US Treasury yields meanwhile are up 8bps at 10-years to 0.82%, not for any blindingly obvious reason, especially as US equities set back a little after recent heady gains. Doubtless Fed QE buying will shortly put paid to this.

The ECB will thus be continue to buy bonds at a €100bn monthly clip for at least another year, in doing effectively agreeing to purchases debt at a faster rate that Eurozone governments will be creating it as part of their national fiscal support mechanisms. In justifying its actions, the ECB’s new forecasts have the economy contracting 8.7% in 2020 (and as much as 12.6% if there is a second wave of COVID-19 cases), CPI inflation still only 1.3% by 2022, and a tightening in financial conditions. We’d dispute the latter (they have eased significantly of late) and ironically the positive Euro reaction to the ECB news has the effect, in isolation, of tightening conditions.

(Late Wednesday night in fact) Germany’s government agreed on a new €130b fiscal stimulus package (3.8% of GDP), driving a still bigger nail into the ‘Schwartz null’ coffin that hitherto bound Germany not to run fiscal deficits. The policy measures included a temporary three percentage point cut to the value-added tax and increased welfare payments including a €300 cash handout for each child (to the parents thereof, we presume). The VAT cut starts on July 1, which means that June retail sales will likely be very weak but can be easily looked through.

The combination of news of more stumbling blocks in the way of agreement on the EU Recovery Fund, more aggressive ECB easing than expected and higher US Treasury yields would have been a classic recipe for EUR/USD weakness, not the near 1% rise we have in fact seen. Testament, we would argue, to the momentum now established behind the long-heralded dollar downturn. Further dollar weakness has seen AUD/USD come within kissing distance of 70 cents (high of 0.6988) before pulling back to near 0.6950 now. Symptomatic of the risk-positive currency backdrop, AUD/JPY has pushed up above Y75.50 and indeed spend some time overnight above Y76. Yesterday NAB published revised FX forecasts, reflecting in part confidence in continuance of the Usd downturn, now seeing AUD/USD at 0.72 cents at year-end and NZD/USD at 0.66.

US initial jobless claims continue to track lower but not quite as quickly as expected, at 1.877mn against the .843m consensus. This brings the cumulative total since mid-March to 43m, and continuing claims running at over 22m over the past four weeks.

US payrolls tonight are expected to show an 8 million fall in employment following the 20.5mn April fall, with the unemployment rate rising to 19.5% from 14.7% last time5.05 from 13.0% last month. Canada’s employment report is expected to show its unemployment rate rising to 15.0% from 13% in April

Before that German factory orders for April are the European data highlight, expected to record a 19.9% monthly drop after falling 16.0% in march, to be 29.7% down on a year ago.

Locally we get the AiG Performance of Services Index, which in April was a paltry 27.1

Sunday brings May China trade data, where exports are expected to be down 6.5% y/y against+3.5% in April in USD terns. Imports though are seen improving, to be down ‘just’ 7.8% y/y up from -14.2% in April

It’s a long (Queen’s birthday) weekend in Australia for all except QLD and WA. There will be no ‘Morning Call’ Podcast on Monday morning, though we will publish a Market Today note, courtesy of our illustrious BNZ colleagues.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.