On a seasonally adjusted basis, the NAB Online Retail Sales Index recorded a drop in growth in July

Insight

The ECB changed nothing overnight, with President Lagarde saying risks remained on the downside.

https://soundcloud.com/user-291029717/ecb-sticks-with-bond-buying-plans-and-readies-for-double-dip-recession?in=user-291029717/sets/the-morning-call

I’ve got the sweetest hangover, I don’t want to get over, Sweetest hangover – Diana Ross

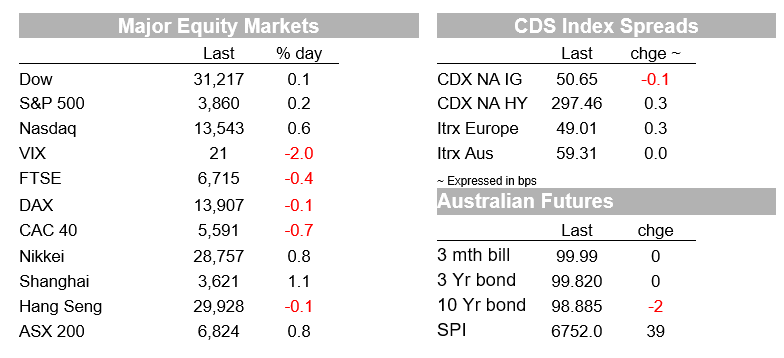

If at least part of Wednesday’s strong US equity market gains could be attributed to positive emotions, bordering on euphoria in some quarters, surrounding Joe Biden’s and Kamala Harris’ Inauguration ceremony and ensuing Tom Hanks-hosted musical celebrations, then there were some (very) small signs of a hangover setting in as Thursday NYSE session progressed.

The S&P500 was down to flat on the day when this missive began an hour ago from +0.2% earlier in the day, though has recouped the intra-day loss coming into the last hour.

The NASDAQ is currently up 0.6%. It therefore requires a very long bow to suggest that risk markets are yet coming close to seriously contemplating any of the potentially equity-unfriendly market aspects of the Biden administration’s policy agenda.

Doubtless that will come at some point, but for now the prospect of stronger fiscal support for the economy and the evident determination of the new administration to get to the other side of the pandemic as quickly as possible, together with incoming Q4 earnings results, looks to be carrying the day(s).

President Biden has just described the vaccine roll-out as a ‘dismal failure’ so far, is asking Americans to ‘mask-up’ until at least April, which he claims could save 50,000 lives, and says his (198 page) plan entails enlarging the pool of vaccinators.

Incoming US economic data had a hand in the early New York day market gains.

Initial jobless claims fell to 900K from a downwardly-revised 926K, below the consensus of 935K, with continuing claims down to 5,054K from 5,181K, also below the consensus of 5,300K.

December housing starts rose 5.8% to 1,669K from an upwardly-revised 1,578K, well above the consensus of 1,560K, as too were building permits, up 4.5% to 1,709K from 1,635K versus 1,608K expected. And, the January Philly Fed index jumped to 26.5 from 9.1, thrashing the consensus of 11.8 and marking something of a catch-up to recent strong underperformance versus the nationwide ISM manufacturing index.

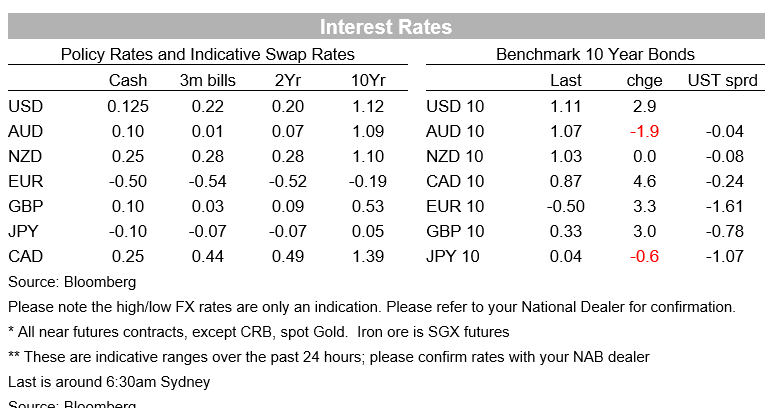

The other set piece during Thursday’s offshore market was the ECB, who left their main policy settings completely unchanged as expected (Deposit Facility Rate at -0.5%, the pandemic emergency purchase programme (PEPP) still EUR1.85tn, to run until Mar 2022 at least, and the asset purchase programme (APP) to remain open-ended at EUR20bn per month.

One comment that caught the bond market’s eye, though had in fact been mentioned by President Lagarde last month, was that, “If favourable financing conditions can be maintained with asset purchase flows that do not exhaust the envelope over the net purchase horizon of the PEPP, the envelope need not be used in full”.

10-year Bund yields lifted from -0.52% to -0.49% (though ended the day back at -0.50%).

In the press conference, Lagarde noted that the economic outlook was broadly in line with the base case set out in December (which looks to the product of some ‘overs and unders’, in so far as the pandemic has clearly worsened in Europe since early December, but the ECB at that time had a ‘no deal’ Brexit as its central scenario, plus we have since had the complete agreement and removal of hurdles to the Next Generation recovery fund).

Lagarde said, “ we are monitoring very carefully exchange rates, very carefully. Because we know that (the) exchange rate has an impact on prices and clearly play a part in our inflation forecast and what we can deliver in our monetary policy….So we are very attentive and as I said earlier on all instruments can be adjusted and nothing is off the table.” The EUR was unfazed by this.

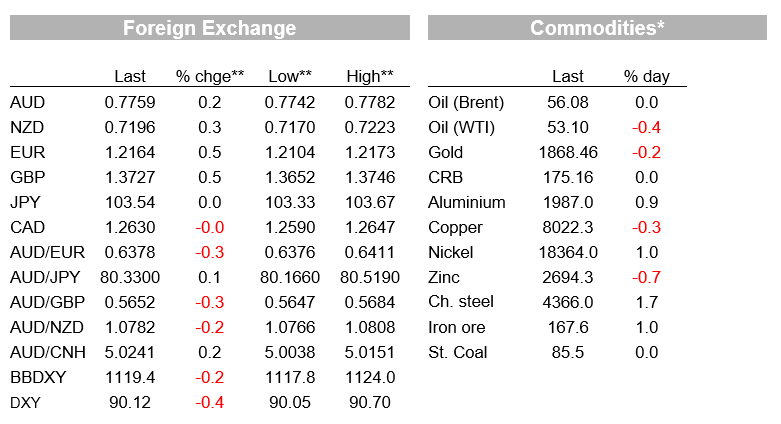

The combination of better than expected US data and the lift in Bund yields has lifted US Treasury yields, 10s currently up just under 3bps to 1.1075%, but off the earlier high of 1.12%, falling in conjunction with the set-back in the S&P500. Of particular note, 10-year US break-even inflation rates as implied by TIPS have risen another 4bps to a new cycle high of 2.16% – meaning 10-year real yields are down by 1bp (to -1.05%). In FX, the USD is therefore drawing no support from the rise in nominal yields, where the BBDXY index is currently 0.17% down on Wednesday’s NY close, albeit just off its intra-day lows.

Individual currency performance shows every G10 currency up against the USD, led by a 1% gain for the NOK, even though oil prices are little changed, and the CAD and JPY up by a mere 0.02-0.03%.

Yesterday’s ‘no change’ BoJ meeting came and went without the JPY market even noticing.

The NZD has recouped a little more of its recent underperformance against the AUD to be up 0.35% against +0.18% for the latter.

AUD/USD is back from an intra-night high of 0.7782 to around 0.7760 now. It got a small boost yesterday in the immediate wake of the December labour market figures, where employment came in bang on expectations at +50K but saw the unemployment rate drop by two tenths to 6.6% from 6.8%, the participation rate up one-tenth to 66.2% to be the highest in the history of the series.

The biggest surprise in the report came from the underemployment rate which fell 0.8 points to 8.5% to be back to pre-pandemic levels (lowest since December 2019) though some commentaries are stressing that this in part reflects people taking part-time work who were seeking full-time employment.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

On a seasonally adjusted basis, the NAB Online Retail Sales Index recorded a drop in growth in July

Insight

Firmer consumer and steady outlook

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.