Our global forecasts are unchanged and we continue to expect soft global growth of only 3.0 to 3.1% between 2024 and 2026.

Insight

It’s been a topsy turvy session overnight.

https://soundcloud.com/user-291029717/equites-fall-again-boe-talks-negative-rates?in=user-291029717/sets/the-morning-call

“Then the stockman rides up with his dry dusty throat; He breasts up to the bar and pulls a wad from his coat; But the smile on his face quickly turns to a sneer; As the barman says sadly the pub’s got no beer”, Slim Dusty 1957

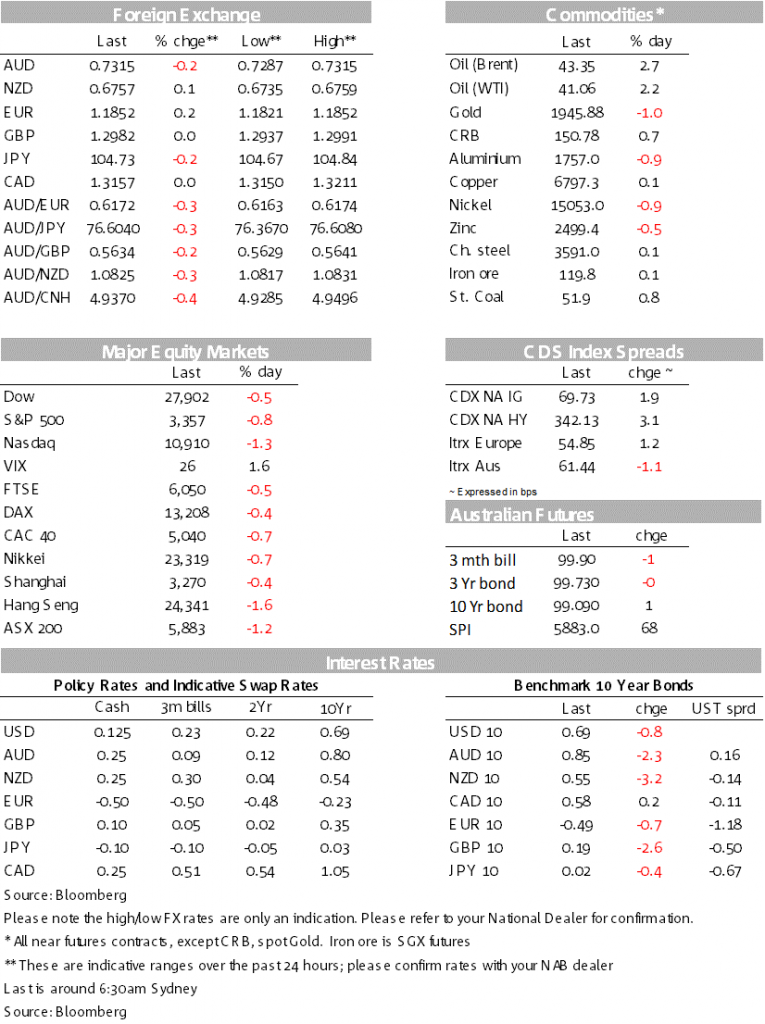

Equities continued their post-FOMC losses with the S&P500 -0.8% with declines led by tech (NASDAQ -1.3%). There was though limited flow through from the weakness into FX or bonds with the USD (DXY) down -0.2% and US 10 yields are little moved at -0.8bps to 0.69%.

GBP was the biggest FX mover intraday, falling sharply after the BoE flagged the possibility of negative rates (initially -0.9% to 1.2865), though quickly reversed given negative rates were not an imminent possibility alongside more positive UK-EU trade headlines.

The AUD also had an interesting session, lifting on yesterday’s strong jobs headlines, reversing on the details and then recovering as the USD weakened to end -0.2% at 0.7315.

As for what caused the smile in equity markets to become a sneer in the words of the title of today’s missive (Slim Dusty’s 1957 hit “a pub with no beer”), Wednesday’s FOMC meeting disappointed some who had expected the Fed to show greater willingness to step in and fill the fiscal void given the US Congress seems unwilling/unable to agree to a new fiscal package.

That paralysis continued overnight despite President Trump stating he liked “the larger numbers” in the bi-partisan $1.5tn House stimulus plan. The Democratic leadership are still pushing for a larger package (latest being $2.2tn), while Republicans are divided with many still strident that any package must be below $1tn (Senator Thune leading GOP member said pushing past $1 trillion “is a threshold at which you start losing Republican support”). Tech valuations also remain under focus with the NASDAQ now down -9.5% since it peak on September 2.

US Jobless Claims were at or slightly better than expected (initial clams 860k v 850k expected; continuing claims that a lagged by a week were 12.6m v 13.0m expected). The Philly Fed Manufacturing Index was inline with expectations at +15, though the details were even more positive with shipments up 27.2 points. Combining the recent Empire Fed and Philly Fed points to a modest decline in the Manufacturing ISM later this month. US housing starts and permits were weaker than expected (permits -0.9% m/m v +2.0% expected), though the housing data overall is still showing very positive trends.

The BoE meeting was the most significant development overnight for those still seeing central banks embarking on another round of stimulus. The BoE left policy unchanged, but flagged it is looking seriously at negative rates (Governor Bailey has previously said it is in the toolbox). The Minutes to the meeting noted “the MPC had been briefed on the Bank of England’s plans to explore how a negative Bank Rate could be implemented effectively, should the outlook for inflation and output warrant it at some point during this period of low equilibrium rates. The Bank of England and the Prudential Regulation Authority will begin structured engagement on the operational considerations in 2020 Q4” (see BoE Minutes for details).

Markets are currently pricing in around 20bps of rate cuts priced-in for the BoE by the end of next year, which implies a cash rate of -0.1%. Given the looming risk of a no-deal Brexit and the recent resurgence in COVID-19 cases in the country, investors are also taking the possibility seriously. The UK gilt curve bull steepened, with 2-to-5 year rates falling by 5bps, but little movement at the longer-end of the curve. The New Zealand curve has also come under steepening pressure since the RBNZ signalled, at the August MPS, its intention to cut the OCR to negative next year. One gets the feeling that central banks are about to embark on another round of co-ordinated easing with the RBA closer to home recently stating “the Board…continues to consider how further monetary measures could support the recovery”.

GBP fell an immediate 0.9% in the wake of the negative rate comments. But with such a prospect still being someway off and most commentators thinking the BoE would embark on further QE before contemplating negative, GBP started to recover to finish unchanged on the day. On Brexit, the EU Commissioner said “I am still convinced [a trade deal] can be done” but said it was up to the UK to withdraw its controversial Internal Market bill to ensure the success of negotiations.

The EUR has recovered almost 1% from its intraday lows yesterday afternoon, below 1.1750, and is now 0.2% higher on the day, at around 1.1852. The JPY is 0.2% stronger despite BoJ Governor Kuroda’s pledge to ease further if labour market weakness impacted the inflation outlook.

Despite a very strong labour market report. Yesterday’s data shot the lights out with employment up +111k against a consensus of -35k.The unemployment rate also surprised, falling seven-tenths to 6.8% from 7.5% (consensus 7.7%). Despite the rosy headline, the detail suggests some caution with most of the jobs’ growth driven by sole traders (owner manager without employees) while hours worked rose a more modest 0.1% compared to the 0.9% m/m rise in employment. Importantly though, today’s data suggests there has been little spill over from Victoria’s lockdown to the rest of Australia, with employment rising in all other states.

Also perhaps contributing to some of the underperformance was an RBA Bulletin article yesterday that hinted at implications for policy. That paper (The Economic Effects of Low Interest Rates and Unconventional Monetary Policy) notes that with an effective lower bound to the cash rate, policy needs to remain lower for a lot longer than otherwise to see inflation return and unemployment fall to their respective targets. In order to ease policy further at the lower bound for the cash rate, the RBA can use unconventional policy (which it has already done via the 3yr YCC and the TFF), but a key transmission channel of lower bond yields is via the real exchange rate, which in this framework sees net exports account for around half of the effect of lower government bond yields on the level of GDP. The implication there is that current unconventional policy may not be as stimulatory as desired by the RBA with the nominal trade weighted exchange rate having appreciated to its highest level since December 2018.

Q2 GDP yesterday in NZ saw the fall in GDP come in close to market expectations (-12.2% v -12.5% expected). Our BNZ colleagues expect an equally large (+13.5%) bounce-back in growth in Q3 but the sobering reality is that the economy will still be about 5% below its pre-Covid peak by the end of the year, according to our forecasts.

A quiet day domestically with no data scheduled. Offshore most focus will be on UK Retail Sales and US Consumer Confidence:

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Our global forecasts are unchanged and we continue to expect soft global growth of only 3.0 to 3.1% between 2024 and 2026.

Insight

Conditions ease as slow growth weighs on firms

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.