On a seasonally adjusted basis, the NAB Online Retail Sales Index recorded a drop in growth in July

Insight

The rally in US equities continued at the end of the week, with the optimism spreading to Europe.

https://soundcloud.com/user-291029717/equities-race-higher-on-trade-optimism?in=user-291029717/sets/the-morning-call&

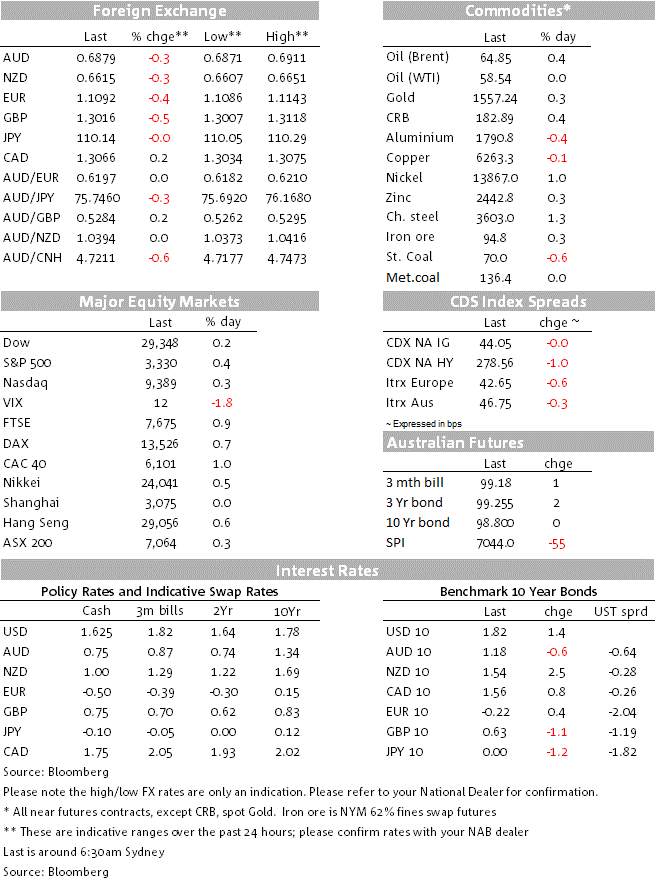

Another day another record high for the US stock market, the S&P500 and NASDAQ chalking up gains of 0.4% and 0.3% respectively and meaning that less than three weeks into 2020, the S&P is up just over 3% and the NADAQ just shy of 5%. The ASX 200 meanwhile, which closed above the 7,000 barrier for the first time last Thursday, added another 0.3% on Friday to finish at 7,064. We really are sounding like a broken record (take you pick from the Plain White Ts, Katy B, Little Boots or Alex Ebert)

In the last week or so, there has been an increasing amount of analytical and journalistic commentary linking the heady performance of US (and with that global) stocks since October last year to the re-inflation of the Fed’s balance sheet that began last September when funding pressures re-emerged in the US market, to which the Fed responded initially by increasing its repo activity with U.S primary dealers and then beginning a programme of additional outright Treasury bill purchases. Dubbed ‘not QE’ on the basis that the Fed is not purchasing longer-dated securities outright with the intention of suppressing the so called ‘term premium’ on longer term government bond yields, the relationship between the size of the Fed’s balance sheet, now some 11% bigger than where it was in late September 2019, and the performance of US risk assets during this period is nevertheless uncanny. Friday’s weekly Fed balance sheet data showed a more than complete reversal of the fall we had seen the prior week, to a new post-September 2019 high of $4.177tn.

Alan Kohler wrote a good piece on this in the Weekend Australian subscriber link and which draws parallels with the Fed’s liquidity injections in late 1999, which was also associated with strong stock market gains which then came to a crashing halt once the liquidity was withdrawn in 2000 when it became clear that the world’s computer systems were not going to stop working and planes weren’t falling out of the sky.

Irrespective of the above, economic data clearly had a hand in Friday’s markets, in particular on GBP where a fleeting attempt to recover from the early week drubbing that followed the big downside surprise on UK inflation and some dovish Bank of England commentary, was put to the sword after an exceptionally weak set of UK December retail sales numbers. Some had though these might show evidence of a ‘Boris bounce’ following the December 12 general election result, but far from it – sales fell by 0.6% in headline terms and a bigger 0.8% excluding auto fuel.

GBP was Friday’s worse performing G10 currency, GBP/USD -0.5% with some contagion effect onto EUR/USD, which fell by 0.4%. Since these two currency pairs make up 70% of the DXY dollar index, the latter was up by 0.3% to 97.6, its best level of the year to date and highest since Christmas Eve. AUD and NZD were both 0.3% lower, to 0.6871 and 0.6607 respectively. GBP is potentially vulnerable to further loses at the start of the weak following an interview with UK chancellor Sajid David in which he poured cold water on the idea of the UK seeking regulatory alignment with the EU.

“There will not be alignment, we will not be a rule taker, we will not be in the single market and we will not be in the customs union — and we will do this by the end of the year,” Javid said, urging companies to “adjust” to the new reality. subscriber link

Friday’s US economic data was overall supportive for US stocks, Treasury bond yields (latter up 1.4bp to 1.82% at 10 years) and the USD. The most eye-popping was housing starts, up 16.9% on the month against expectations for a 1.1% rise, though unseasonably mild December weather doubtless had a hand here (building permits actually fell by 3.9% though are still on a rising trend). It also impacted negatively on utilities output (i.e. heating) which supressed headline industrial production (-0.3%) relative to manufacturing output (+0.2%), better than the -0.1% expected]. JOLTS job openings a – a past favourite of Janet Yellen – shows clear signs of easing, down to 6.8mn from 7.361mn in October, while the preliminary University of Michigan Consumer Sentiment Index dipped by 0.2 to a still very strong 99.1 against 99.3 expected.

A reminder that Friday’s China activity indicators beat expectations, while GDP was broadly in line. Overall positive and evidence of growth stabilisation at the end of 2019. Industrial Production was 6.9% y/y up from 6.2% and against 5.9% expected, Retail Sales growth was steady at 8.0% y/y against 7.9% expected and Fixed Asset investment 5.4% up from 5.2% and the 5.2% consensus. GDP growth beat on the quarter at 1.5% q/q against 1.4% expected, keeping the y/y growth rate at 6.0% y/y. Multi-decade lows sure, but don’t forget than for an economy that has been doubling in size about every 10 year, 6% growth represents a much bigger absolute increase in demand than the 7% growth rates we last saw in 2017.

US stock and bond markets will be closed for the Martin Luther King Jr. holiday. Wellington is also on holiday.

Key to Australian markets this week should be Thursday’s Labour Force Survey, where NAB is forecasting a weaker than consensus outcome both for employment (+10k vs. +5k consensus) and unemployment (5.3% from 5.2% and 5.2% consensus). Wednesday’s Westpac Consumer Confidence will also be of keen interest, as the most comprehensive read to date of the impact of the bushfires on sentiment. NZ has Q4 CPI on Friday, ahead of Australia’s next week.

Internationally, US earnings season holds more interest than the data calendar which is light. Netflix is the first of the FAANGS to report, on Tuesday. The ECB, BoJ and BoC all meet. ‘Flash’ European PMIs on Friday will also be important.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

On a seasonally adjusted basis, the NAB Online Retail Sales Index recorded a drop in growth in July

Insight

Firmer consumer and steady outlook

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.