Online retail sales growth slowed in May following a fairly strong April

Insight

The US dollar managed a slight recovery which has also seen continued growth in US equities.

https://soundcloud.com/user-291029717/a-slower-recovery-than-hoped-for-yet-equities-still-rise?in=user-291029717/sets/the-morning-call

Incoming US economic data continues to play no part in explaining the latest lurch higher in US stocks, which sees the S&P500 and Dow ending the day +1.5% and 1.6% respectively but the NASDAQ a lesser 1%. The latter still hugely impressive of course but meaning that the latest rally is not the highly concentrated, ‘FAANG’-driven affair that has been the case for much of recent months. Quite why the rally has broadened out is frankly anyone’s guess, though both the ‘rates lower for longer’ and ‘vaccine round the corner’ pretexts both received some (small) succour overnight.

The WHO sanctioned the use of two cheap steroids to treat severely ill Covid-19 patients (on the premise they can reduce mortality rates by a third).

NY Fed President John Williams said the Federal Reserve’s updated monetary policy framework will improve the central bank’s ability to reach its inflation target and combat unemployment. The Fed’s new plan “represents both an important evolution in our thinking about how to achieve our goals and another step toward greater transparency,” adding the framework “positions us for success in achieving our maximum employment and price stability goals in the future.”

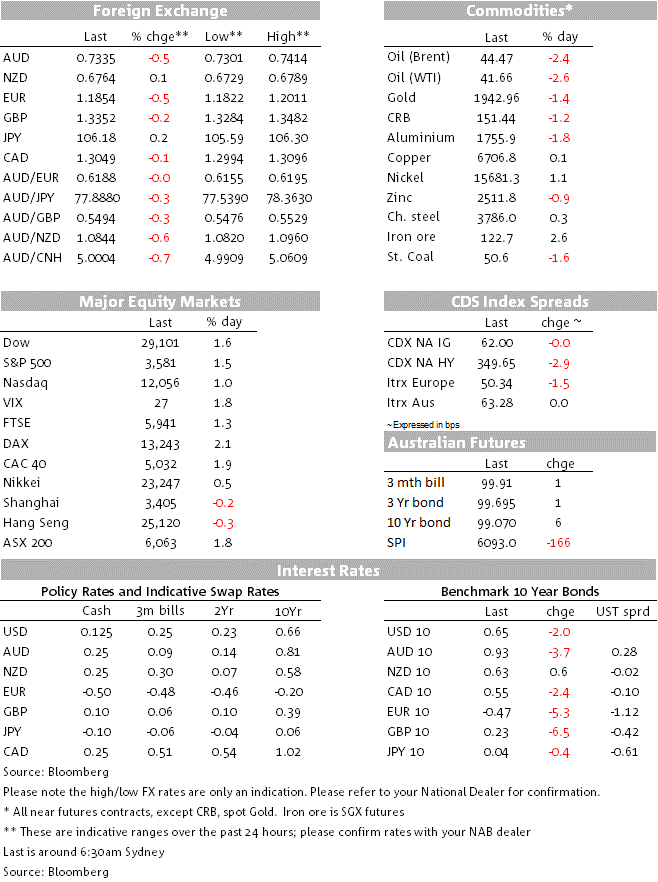

Nothing really new from the third most important Fed official (after Powell and Fed VC Clarida) though US bond yields are lower (10s -2.5bps to 0.644%) so the fall in the risk-free rate at which future corporate earnings are discounted is again on offer as an excuse for higher stocks, if one were needed.

Neither incoming US economic news or developments inside the Washington Beltway have given any cause for cheer overnight. The ADP Employment report came in much weaker than expected 428k against a consensus estimate of 1 million – suggesting downside risk to Friday’s non-farm payrolls relative to the current 1.35 million consensus. The Fed’s Beige Book, ahead of their September FOMC meeting, notes a pick-up in activity in most regions but described gains as mostly ‘modest’. And in Washington, House Speaker Nancy Pelosi reported “serious differences” remain regarding agreement to a new fiscal support package, following the phone call she had with US Treasury Secretary Steve Mnuchin which he has promised during a congressional hearing the day before.

By much more than their US equivalents, anything from 5 to 7 basis points at 10 years. Evidently, comments from notoriously hawkish Bundesbank President Jens Weidmann were summarily ignored. He said the ECB must withdraw emergency support when the economy has recovered from its pandemic shock, noting it has always been important that the 1.35 trillion-euro emergency bond-buying program is “limited in duration and clearly linked to the crisis,”

Germany saw near-record demand for a €6.5bn sale of “green” 10-year bonds, attracting demand of €33bn for the zero-coupon bond, pricing at minus 0.46%, 1bp under the prevailing conventional 10-year bond at the time. As my BNZ colleague Jason Wong puts it this morning, ‘as well as signalling insatiable demand from fixed income investors to allow their capital to erode in real terms (the attraction being it might erode at a slower pace than other “low risk” investments), it also signalled strong demand for ESG investments. Losing money has never felt better, in the name of a good cause’.

We finally have some let up in the almost uninterrupted USD downtrend of recent weeks, USD indices up by about quarter of a percent. Both AUD/USD and EUR/USD are about 0.5% lower than this time yesterday, AUD to a low 0.7301 from high of 0.7414 on Tuesday and EUR/USD to a low of 1.1822 after topping 1.20 earlier in the week.

The EUR had started falling on Tuesday night after ECB chief economist Phillip Lane had said that the currency mattered to the ECB even though it was not targeted, comments which we consider to have been taken out of context. This is certainly so judging from recent comments from Lane’s ECB colleague Isabel Schnabel who noted “I would also be cautious in interpreting the exchange rate changes in isolation, because research shows that if there is a depreciation of the US dollar, this tends to boost global trade and global growth. So even though there may be a competitiveness effect for euro area corporates, there is an effect working through global trade, which may actually compensate for that. At the moment I am not worrying too much about exchange rate developments.”

We rather think the read headlines of Lane’s comments were the excuse for some traders to take profits on long EUR positions, in the context of market positioning which looks to have become much more stretched than any other major currency. The currency outperformer of the last 24 hours has been the NZD, which received a fillip after RBNZ Governor Adrian Orr said that the exchange rate was behaving as one would expect and was not a concern. Together with AUD/USD slippage, the AUD/NZD cross fell to a low of 1.0820.

Yesterday’s Q2 GDP figures took a small bite out of the AUD – the O/n USD correction then doing the rest – though did no harm to stocks, the ASX 200 by far the strongest performing APAC equity index (+1.84%). GDP fell by 7% Q/Q (-6.3% y/y), confirming the large hit to economic activity as a result of the shutdown to limit the COVID-19 pandemic.

The fall in activity was driven by a collapse in household consumption (down 12% on the quarter) where spending on services fell 18% amid the peak of the restrictions. Likewise, by industry, hospitality and recreational services saw the largest falls in activity, although nearly all industries were heavily impacted. We expect that we are past the peak impact on activity, but the recovery will be still be a long process. We forecast a broadly flat outcome in Q3 (which will be impacted by the Victorian restrictions) and a ramping up in the level of activity as the economy reopens in the first half of 2021. Attention is now turning to the 8 October Budget where Treasurer Frydenberg post the GDP data is talking of five year recovery plan, including some $10bn worth of infrastructure spending (though remember that is the equivalent of about 0.5% of GD).

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.