Online retail sales growth slowed in May following a fairly strong April

Insight

US equities continue to rise, even though the jobless claims numbers rose last week.

“Right from the start; I gave you my heart; Oh oh, I gave you my heart; Don’t go breaking my heart”, Elton John & Kiki Dee 1976

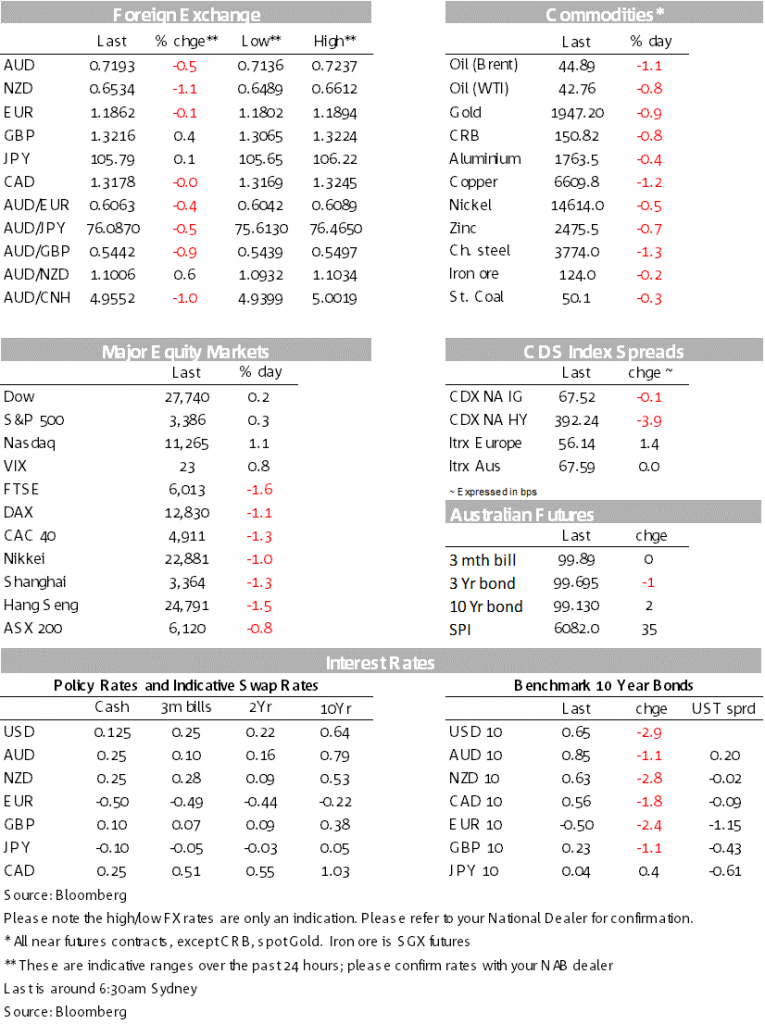

“Don’t go breaking my heart” was Elton John’s 1976 global hit and so it was with equities overnight with the S&P500 closing up 0.3% despite worrying jobs data (initial US jobless claims 1.1m v 0.9m expected). Tech outperformance was the driver with gains led by Microsoft (+2.1%), Facebook (+1.8%) and Apple (+1.5%), while the wider tech-heavy NASDAQ closed up 1.1% with lots more talk around talk valuations – e.g. Tesla rose 6.5% overnight and is up an incredible 21% over the week ahead of a 5-for-1 stock split on August 31.

With the US 10yr Treasury yield -3.4bps to 0.65% and more than reversing yesterday’s post FOMC Minutes moves (post FOMC high was 0.68%). Implied inflation breakevens also fell overnight with the US 10yr implied inflation breakeven down -3.8bps to 1.6274% and below the recent intraday peak of 1.7182%. Partly driving was an underperforming $7bn 30yr TIPS auction which came in more than 5bps above the prevailing yield when issued (issue -0.272%, prior to auction was -0.325%). The underperformance also perhaps reflects some uneasiness over views around inflation given the sharp run up in inflation expectations – 10yr breakevens have risen by more than 100bps since their lows – and FOMC Minutes yesterday that said little around allowing the economy to run overwhelmingly hot.

They disappointed expectations coming in at 1.11m v. 0.92m expected 0.97m previously. The rise for the week of August 15 suggests that a another wave of layoffs may be starting in the US and this will be important to watch for the recovery, especially given the scaled down unemployment benefit supplement (to $300 a week from $600 a week; $400 if states kick in an extra $100) is yet to be rolled out comprehensively across the US. According to a Labor Department official: “An extra $300 a week in federal unemployment benefits is likely to take a couple of weeks to reach workers and funding could be exhausted a month and a half later” (see WSJ for details). Continuing claims for the week prior though did fall to 14.8m from 15.5m. Also disappointing expectations slightly was the Philly Fed coming in at 17.2 v. 20.8 expected.

The USD fell with the DXY -0.3% to 92.74 and remaining near two year lows (and also reversing some of the post FOMC Minute moves). GBP was the outperformer, up 1.2% from yesterday’s lows to 1.3216. There is no obvious driver with little news from Brexit negotiations. The NZD was the underperformer, down some -1.1%. Again there is no obvious catalyst for the move, though the dovish signals from the RBNZ and the possibility of negative rates in NZ next year has been the overwhelming narrative since the MPS. The RBNZ/Treasury made some tweaks yesterday to the Business Finance Guarantee Scheme (covers 80% of any losses on loans made by banks under the scheme, and take up as been minimal and so is increasing the max loan size from 500k to 5m. the term of its Term Lending Facility term has also been extended from three years to five years.

There was little news yesterday in regards to Australia, though an MNI sources piece did suggest to expect strong Chinese growth in Q3 (5%) and Q4 (6%). However a lack of recovery in retail and private investment will continue to put the focus on stimulus to drive growth, which should benefit Australia’s commodity exports.

COVID-19 cases continue to rise, with the one-week change in new cases reaching its highest since early May. The renewed spread of the virus in Europe, albeit nothing like the sharp rise seen earlier in the year, highlights the challenge of safely reopening economies. French President Macron ruled out another lockdown and said the country would use more targeted measures to control its spread. In the US, the growth in new cases is trending lower.

Domestic focus will be on retail sales for July which could show a further rise even though the level of retail sales is 7.2% above pre-pandemic levels. A testament to the amount of government support which has buttressed household incomes during the pandemic. Across the ditch, the RBNZ’s chief economist Ha is speaking on a webinar on the recent unexpectedly dovish MPS with our BNZ colleagues now expecting the RBNZ will take its cash rate into negative in 2021. Offshore flash PMIs dominate with focus on whether the European PMIs lift further above 50. The US is relatively quiet with only existing home sales in addition to the flash PMIs. Details below:

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.