Total spending grew 0.9% in June.

There’s more optimism today that countries are reaching the peak of COVID-19, which is pushing US equities higher.

https://soundcloud.com/user-291029717/eu-fiddles-whilst-equities-rise?in=user-291029717/sets/the-morning-call

I feel most times we’re high and low (high and low)

If I had my way, never let you go (never let you go) – Empire of the Sun

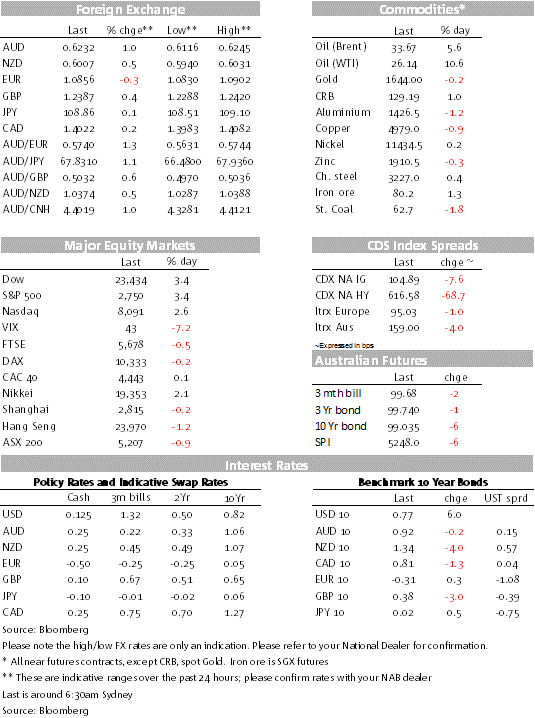

Price action overnight has been a story of optimism and disappointment. US equities are riding high on the back of encouraging COVID-19 stats while President Trump is talking up the prospect of opening up the economy again. Meanwhile, disillusionment is the driving factor in Europe as EU finance ministers failed to reach agreement on a united stimulus package. Ahead of the Opec+ meeting tonight, oil prices are heading higher and while the USD is broadly stronger against majors, reflecting EU currencies’ weakness. The AUD and NZD have outperformed on the positive US vibes.

US equities had a good day with the Dow and S&P500 up over 3% while the NASAQ gained 2.6%. The S&P 500 is now just over 20% above its March 23 low, which in the eyes of many it would signal the index is now back on a bull market. Positively too, overnight gains were broad based with all 11 sectors in the S&P 500 recording gains for the day. Market volatility remains elevated, encouragingly, however the VIX index has continued is steady decline ending the day at 43, on March 19 the index printed a high of 85.47.

US optimism has been driven by further declines in the rate of US COVID-19 infections. Anthony Fauci, director of the US National Institute of Allergy and Infectious Diseases, said the start of a turnaround in the fight against the coronavirus could come after this week. While President Trump has also chimed in tweeting and speaking on Fox news about the prospect of re-opening the economy sooner rather than later. Speaking to Fox News, the President said the administration was “looking at the concept where we open sections of the country and we’re also looking at the concept where you open up everything.

Although the market has embraced all this news and run with the optimism, scientist recommendations around the world advocate a cautious approach to the removal of containment measures, the risk of a second round of infection is just as bad as the first one if containment measures are not managed carefully. After initial success, Japan and Singapore have now tighten their containment measures and even in Europe talks of easing measure are only gradual, Austria for instance is looking at opening essential stores while keeping most measures in place including keeping schools closed. Worth noting too that president Trump has constantly move his position and events in other parts of the world, suggest the President is being too optimistic, unless we find a vaccine, most containment measures are more likely to be in place for months rather than weeks.

Talks of more US fiscal stimulus have also helped the overnight positive vibes. Democrats calling for another $500b (~5%/GDP) stimulus package. In addition to the $250b requested by Treasury Secretary Mnuchin for small businesses, the Democrats want more money for hospitals and state and local governments. These are still early days, but the fact that both Democrats and Republicans are talking about it is good omen, we should expect more US stimulus, the magnitude is the more uncertain aspect.

Yesterday after more than 16 hours of negotiations and around the time some of us were thinking about cooking dinner duties ( yeap one the perks from working at home!), EU finance ministers failed to reach an agreement on a potential €500bn COVID19 rescue package, effectively prolonging a paralysis that is increasing the risk of a deeper recession for many European countries while adding yet another reason for many to consider leaving the Union. A new call has been schedule tonight although is unclear whether major differences can be reconciled.

The Netherlands is reportedly resisting a proposal for joint European bonds (so-called ‘coronabonds’) and insisting that lending to more vulnerable countries, like Italy, takes place through the ESM, with conditions attached. The Italian government, on the other side, is not prepared to accept strict conditions on ESM loans given the backlash that would occur in its home country. Leader of the populist League party in Italy, Matteo Salvini called ESM funding “illegal and senseless.”.

EU politicians have a history of staring at the abysms, before making last minute decisions, so chances are that history repeats itself. On this score, French Finance Minister Le Maire said he was “certain” a deal could be agreed.

The lack of resolution saw Italian 10y BTPS up 4bps to 1.645% while the Euro (-0.35% to 1.0856) and other European currencies lost ground against the USD. Looking at core bond yields, 10y Bunds were little changed while the move up in UST yields was led back by the back-end of the curve, both the 10y and 30y UST tenors gained around 7bps relative to Sydney closing levels, to 0.772% and 1.37% respectively.

Offshore credit markets have had a good session, with US CDS indices tighter by 10bps (for investment-grade) to 60bps (for high-yield). In other credit-related news, Everi Holdings, which makes casino games, is the second company to seek to raise funding via the leveraged loan market.

USD indices vs majors (DXY 0.29% and BBDXY o.11%) edged a little bit higher, helped by EU currencies’ weakness while the USD was mostly weaker against EM/Asian currencies.

The positive vibes coming from the US equity and credit market boosted the pro-growth antipodean currencies with the AUD leading the charge, up ~1 % over the past 24 hrs. The pair now trades at 0.6230, after printing an overnight high of 0.6245. The appreciation in the AUD came despite S&P revising the outlook for the Australian government’s credit rating to negative. In other news, Australia yesterday passed a wage subsidy scheme, which will see the government pay a subsidy of $1,500 every two weeks per employee.

The NZD is not far behind, up ~0.90% and now trading at 0.6012. Both antipodean currencies enjoyed a steady rise over the course of the night mimicking the move up in US equities.

There were more interesting comments from RBNZ Assistant Governor Hawkesby and Chief Economist Ha yesterday. Both signalled that the QE programme was likely to be upsized at the May MPC meeting on the 13th, because the bond market will be a lot bigger than what the RBNZ had originally assumed. Both also seemed to push back on the notion that the RBNZ should buy corporate bonds. Ha told interest.co.nz “corporate ones are a little bit trickier. I don’t know where we’d go on that one.” Hawkesby expressed hope that the RBNZ’s large-scale purchases of LGFA bonds, on their own, will help other areas of the broader credit market. Ha also flagged the possibility of FX intervention, which would involve the RBNZ selling the NZD, in an attempt to lower the currency, and accumulating foreign assets. On the potential for a negative OCR, Ha said this was “probably something that comes back on the table at some point”, but it wasn’t an immediate priority.

Oil prices have been very volatile (again) overnight, ahead of the meeting of OPEC+ tonight and then the G20 energy ministers on Friday night. Brent is up ~5% and WTI is up ~9%, market now await any agreement on production cuts, not just from OPEC and friends, but also from big producers such as US, Canada and Brazil. The markets has an oversupply of around 35mb/d, so unless we get meanigfull agreement, the market will remain oversupply and any uptick in prices is unlikely to be sustain..Buy the rumour sell the fact?

Bernie Sanders conceded in the race to become the Democratic Presidential nominee, paving the way for Joe Biden to run for president later this year. The news isn’t a surprise, with Biden having amassed a strong lead.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.