We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

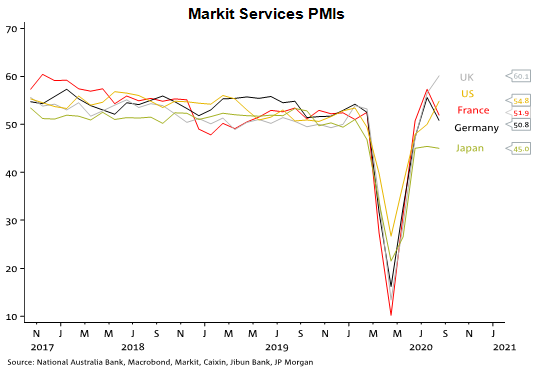

Europe’s PMI’s disappointed markets on Friday, whereas the US numbers were better than expected.

Friday was a night of sharp contrasts between the economic news out of the Eurozone, where the rising trend in Covid-19 infection rates in France, Germany, Italy and especially Spain in recent weeks showed up in fall-backs in ‘flash’ PMIs, led by France’s service sector, and the US which saw stronger than expected Markit PMIs and a huge jump in Existing Home Sales – and also the UK where retail sales and PMIs significantly exceed expectations. For the most part this showed up in relative equity and currency market performance (US stock up but Eurozone down) and currencies (USD up, EUR down) whereas for UK markets negative headlines out of the latest set of EU-UK trade talks overshadowed the economic data to push GBP smartly lower.

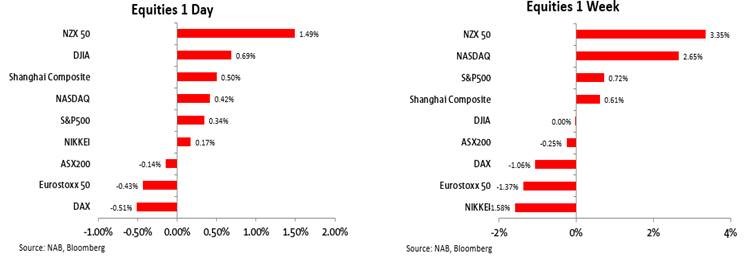

Equities saw the S&P push on to a another record close of 3,397 (+0.34%) and too the NASDAQ (+0.42%) whereas the Eurostoxx 50 earlier finished 0.43% lower. On the week the NASDAQ is again the outperformer amongst the major indices, though eclipsed by a 3.35% rise for New Zealand – the latter doubtless spurred on by the latest commitments from the RBNZ, now marked out as the world’s most dovish central bank.

Apple was again one of the start technology sector performers on Friday, up 5% on the day, reportedly linked to indications from US official that plans to outlaw the use of WeChat in the United States would not apply to US firms’ operations inside China.

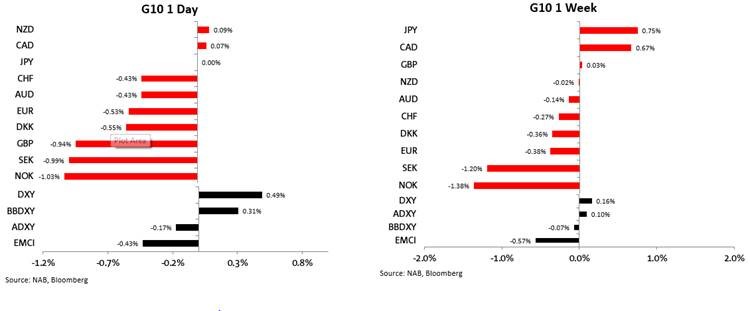

GBP was the biggest loser among the G10 majors, down 0.9% and back to flat on the week, positive economic news from both retail sales and PMIs overshadowed by negative headlines out of the latest round of EU-UK post-Brexit trade talks, following which the EU’s Michel Barnier said he sees a trade deal ‘unlikely’ and suggested things are ‘going backwards more than forwards’. The UK’s Daily Mail at the weekend reported that Cabinet Office Minister Michael Gove is ‘working round the clock’ to prepare Britain for a No Deal Brexit, as the UK’s trade talks with the EU continue to be deadlocked.

The latest round of talks, the seventh, which started on Tuesday, floundered over the EU’s insistence on prioritising agreement on state aid and fisheries. The UK’s negotiator, David Frost, agreed this weekend that there had been ‘little progress’. A Government source said: ‘While an agreement by the end of September is still possible, a long to-do list still remains and time is of the essence for both sides. The EU’s insistence that nothing can progress until we have accepted EU positions on fisheries and state aid policy is a recipe for holding up the whole negotiation at a moment when time is short for both sides’.

And also a 0.5% fall in EUR/USD post the Eurozone PMI data, the USD was up in index terms notwithstanding it being a modestly positive session for US risk assets. BBDXY was up 0.3% Friday to be about flat on the week and DXY +0.5% to be 0.16% up on the week.

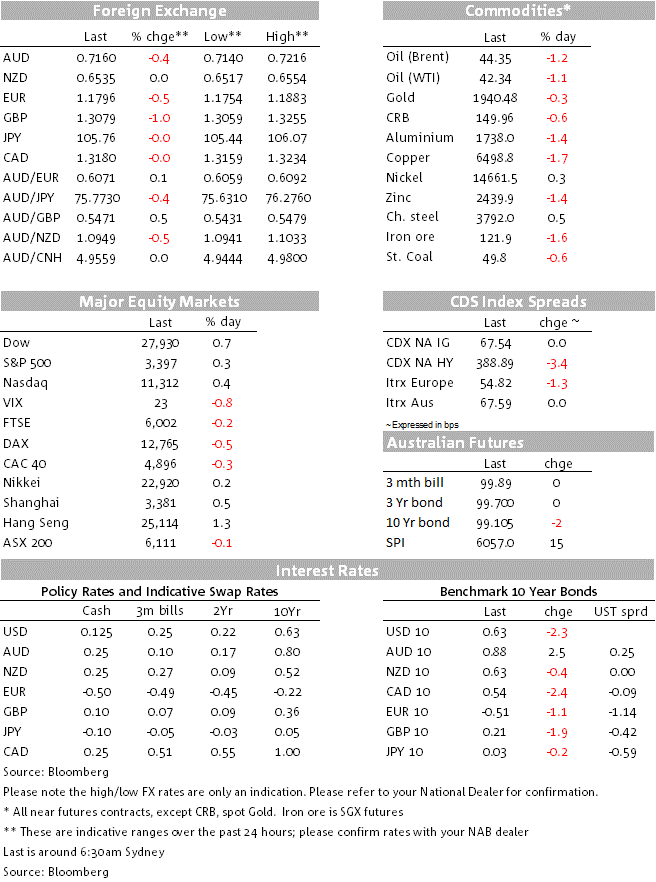

AUD/USD lost 0.4% to end the week 0.14% lower at 0.7161. NZD clawed back a little of recent cross-rate underperformance to be 0.1% up on the USD to end flat on the week at 0.6541. Both AUD and NZD have started the new week little changed from their NY closes.

Bond markets saw yield slower on Friday and also on the week, so at least partially reversing the prior week’s significant rise.10-year Treasuries lost about 2bps to 0.63% (down from a peak of 0.72% on 13 August)

Includes a report, c/o the FT, that the Trump administration is considering bypassing normal US regulatory standards to fast-track an experimental coronavirus vaccine from the UK for use in America ahead of the presidential election, according to three people briefed on the plan. One option being explored to speed up the availability of a vaccine would involve the US Food and Drug Administration (FDA) awarding “emergency use authorisation” (EUA) in October to a vaccine being developed in a partnership between AstraZeneca and Oxford university, based on the results from a relatively small UK study if it is successful, the people said. This news follows claims by President Trump that members of the ‘deep state’ in the FDA are slowing down the progress of a vaccine to sabotage his re-election bid.

As foreshadowed last week the House of Representatives passed legislation to address concerns about the U.S. Postal Service. The bill would provide $25 billion in emergency funds to shore up the U.S. Postal Service and halt any changes to the agency’s operation until after the November presidential election. The vote came just one day after the USPS’s newly appointed boss, Postmaster General Louis DeJoy, testified before a Senate committee on Friday, reassuring lawmakers that his agency could handle the expected influx of mail-in ballots. The Bill is unlikely to be taken up by the Senate, besides which President Trump on Friday said he would veto it.

Will be the weekend press reports on Friday’s national cabinet meeting in which RBA Governor Philp Lowe said the states and territories need to inject another $40bn (~2% of GDP) into job-creating infrastructure. According to the Weekend Australian, Dr Lowe and Treasury secretary Steven Kennedy briefed state and territory leaders on the economic outlook, warning that unemployment was forecast to stay above 7 per cent for the next two years. The economic briefing came as parliament’s independent budget watchdog issued a warning about the nation’s debt levels, revealing that Australia’s net debt burden was estimated to be up to $800bn higher than would have been the case without the COVID-19 crisis. Three policy priority areas were identified by Dr Lowe: the provision of income support through programs such as JobKeeper and JobSeeker; the development of infrastructure and training programs across the areas of energy, transport, housing, schools and hospitals; and the implementation of measures to ease the cost of doing business.

“The level of commonwealth investment in fiscal intervention in this crisis is well over 15 per cent of our economy,” Mr Morrison said. “As a share of state product, the states in total (have committed) around 2.5 per cent…but the Reserve Bank governor called on the states and territories today to lift their fiscal investment over the next two years in programs of the nature that I’ve outlined … to the tune of 2 per cent of GDP or $40bn over the next two years. Dr Lowe told state and territory leaders they could absorb the debt required to fund the additional $40bn in spending. Mr Morrison said: “I would support that view. The expenditure, of course, needs to be purposeful. It needs to be targeted. It needs to go where it’s going to have the best effect.” Ratings agencies backed the call from the central bank. Standard & Poor’s Global Ratings analyst Anthony Walker said: “State government balance sheets have plenty of room to accommodate additional infrastructure investment.”

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

Economic and financial market update

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.