Total spending grew 0.9% in June.

European PMIs came out weaker than expected. That, together with a downbeat Mario Draghi, saw the Euro weaken.

https://soundcloud.com/user-291029717/europes-weakening-economy-and-a-downbeat-draghi-time-to-write-off-a-rate-rise

Markets are again choppy overnight in the midst of OK US earnings, especially from a better performance from semi-conductor stocks overnight, markets overall weighed down by continuing concerns over a global slowdown without resolution on trade issues, the shutdown, and Brexit if you wanted to throw that in too. ECB President Draghi made clear that they have downgraded the outlook from balanced to clear downside risk, Euro PMIs were mixed but with distinct signs of trade-related softness. US Jobless claims printed very low, but the US Leading Indicator for December was soft, tilting toward recession risk a little more

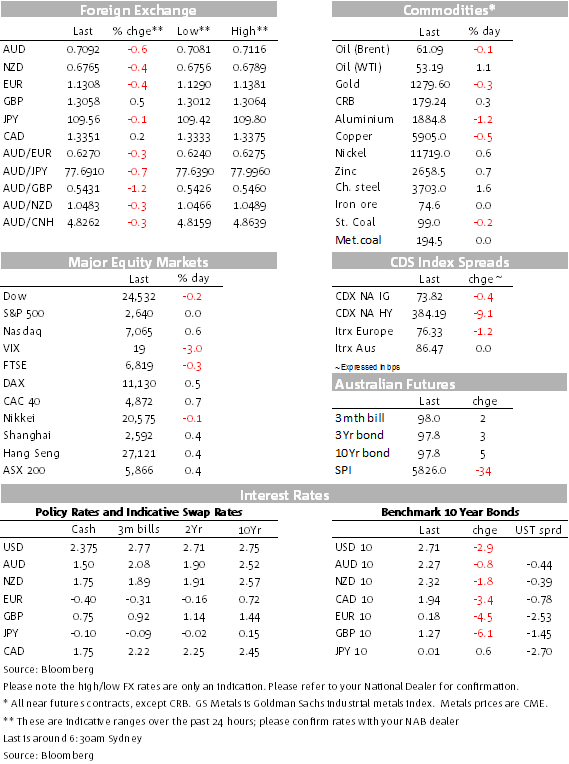

At the centre of the FX market overnight has been further weakness in the Euro and the AUD for their own reasons, while Cable has seen some more support as a Brexit crash out on March 29 looks increasingly unlikely. The USD is on net stronger but has had its own whippiness, getting some support from EUR/AUD softness, but not helped by US Commerce Secretary Wilbur Ross’s comments in an interview suggesting still some gulf between the US and China over trade policy.

To recount yesterday’s events for the AUD, it rose in the immediate aftermath of a better than expected labour market report for December, unemployment back down to 5% (below 5% unrounded). But then the market saw NAB had increased mortgage rates, the market joining the dots that, reading through that this would put more pressure on the RBA to ease, supporting bonds and scuttling the AUD. It was pulled down also with EUR weakness, only supported for a time by a whippy USD. It’s now trading near its overnight lows.

The EUR was volatile in the aftermath of a mixed set of French/German/Euro PMIs released earlier in the evening, but then a downbeat Draghi laid his risk growth risk cards on the table, the ECB formally changing its risk outlook from balanced in December to downside risk from a combination of geopolitics, protectionism and global factors. This meeting was one to take stock rather than delve into policy implications, Draghi said, but the read through was very much that a previously-posited rate rise after the summer now looks a very distant prospect, one that’s Slip Slidin’ Away as Paul Simon wrote many year back. It’s always a worry too when central banks assert that the risk of recession is low.

The suite of preliminary French, German, and Eurozone PMIs readings for January had their soft parts, especially the German Manufacturing PMI that printed sub-50 at 49.9 (51.5 expected), as did the French Services index (again) at 47.5 (French banks?). The Composite indexes were a little better than expected for Germany, worse for France and the Eurozone. There was particular weakness in German manufacturing orders, especially export orders, coming with ongoing softness in the German auto industry from softer offshore demand.

US Commerce Secretary Wilbur Ross did a TV interview making clear that while he expressed some confidence a deal could/would be done with China (what would it look like and when?), he made clear there’s still quite a gulf between the US and China over trade and especially intellectual property and technology, much more prickly areas to come to any mutually acceptable agreement. Chinese Vice Premier is to meet with US Trade Representative Lighthizer next week, Jan 30-31. The US Government shutdown enters day 34 with unpaid US government workers unable to get unemployment benefits and some availing themselves of food stamps.

US Jobless claims thus remained low. In fact they printed below 200k at 199K, a sign of a still strong US labour market. Despite this, the US Leading Indicator (a key recession risk indicator, one of the most reliable) for December again wavered, down 0.1% as it has in recent months, held down by lower ISM orders, building permits and of course the rout in stocks.

With markets still choppy and global slowdown chatter continuing, the bid tone for global bonds continued, US 2s down 1.87bps and 10s down 2.52bps to 2.7157%, testing 2.7%. There were even deeper falls in benchmark Euro yields, 10y bunds down 4.5bps to 0.18%.

Oil has been steadier, WTI seeing a modest recovery, up 1.2%, the LMEX base metals index was down 0.2% and copper by 0.5%. Gold was also somewhat lower (-0.4%) while bulks were more mixed, Dalian iron ore futures and Chinese steel rebar futures also higher, looking at Chinese macro growth support measures.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.