Online retail sales growth slowed in May following a fairly strong April

Insight

There was some short-term market reaction during Powell's press conference.

https://soundcloud.com/user-291029717/fed-cuts-as-expected-but-markets-still-react?in=user-291029717/sets/the-morning-call

The FOMC cut the target Fed funds rate by 25bps to 2.00-2.25% as expected and is stopping the rundown if its balance sheet effective 1st August for reasons of consistency and simplicity – otherwise the Fed would be easing and tightening at the same time – rather than the planned stop at the end of September. The Fed failed to cut the Interest On Excess Reserves (IOER) by more than 25ps (only to 2.10%, down from 2.35%) against expectations that they probably would in order to keep the Effective Fed Funds rate closer to the mid-point of the new target band. There were two dissenters from the decision, Kansas Fed President Esther George and Boston’s Eric Rosengren, neither of whom wanted any change.

The Fed statement justified the cut “in light of the implications of global developments for the economic outlook as well as muted inflation pressures”. The Fed also said that “growth of business fixed investment has been soft.” Against this it noted that “the labor market remains strong and… economic activity has been rising at a moderate rate. Job gains have been solid, on average, in recent months”. On inflation it notes that “market-based measures of inflation compensation remain low” while “survey-based measures of longer-term inflation expectations are little changed” (the latter the same language they used in June).

In the subsequent press conference, Fed chair Powell said that the Committee saw this as moving to a somewhat accommodative policy stance and that this was more in the nature of a mid-cycle adjustment (our emphasis on both) rather than the start of a lengthy rate cutting cycle. This sent equity markets into a tail spin, bond yields jumping, as did the dollar to a new cycle higher. While he didn’t reverse course on these and while he said that this is not the start of a long series of cuts, in answer to a question he did respond “I didn’t say it’s just one cut”.

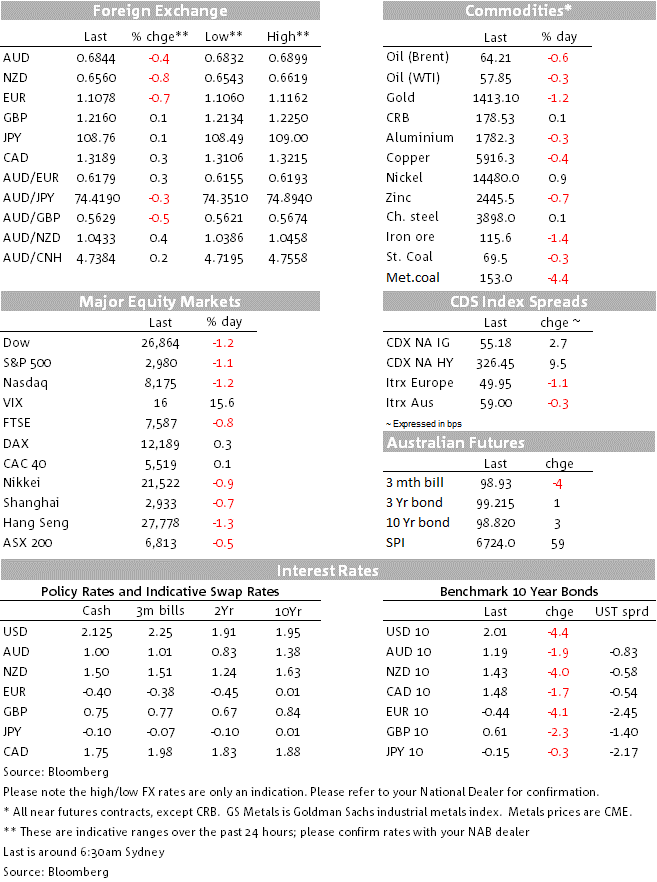

The latter comment looks to have aided the recovery in equities in late afternoon NY trade and where the S&P closed with a loss of 1.1%, the NASDAQ -1.2% and the Dow -1.2%, the S&P having been down 1.8% in the 45 minutes or so following the Fed announcement and early stages of the Powell press conference.

The Treasury bond market has predictably seen significantly curve flattening as the front end of the market is forced to scale back on prior expectations for at least 100bps of easing. 2-year treasuries are currently +2.5bps but it is more notable that 10s are now down 5bps and back pressing against 2.0%, which as my rates strategy colleague Alex Stanley notes, suggest the market thinks the Fed is making a policy mistake by not being more dovish.

In FX, the US dollar jumped, the DXY index to its highest since May 2016 at 98.68 (+0.6%). We’ve been noting in our client presentations of late and a recent FX Strategy Soundbite (see: ‘What does a new Fed cycle mean for the USD and the AUD?’ from 28th June) that the USD has fallen in the early stages of every Fed easing cycle since 1984 with the exertion of 1995, which was the only mid-cycle ‘insurance’ easing – just as this one is so far being portrayed by Mr Powell.

Bar a relatively stable GBP, all G10 currencies have fallen against the surging USD with SEK and NOK leading the way. the NZD has had insult added to yesterday’s post ANZ survey injury, which our BNZ colleagues described as the ‘straw that broke the camel’s back’ in prompting them to revise their RBNZ call to now expect two 25bps cuts to the OCR this years, taking it down to 1% by November. NZD is off 0.75% on this time yesterday, to its lowest levels since June 20th (0.6560)

The AUD has gone from hero to zero, having rallied to 0.6899 in the wake of yesterday’s CPI data, where there was some relief that the core Trimmed Mean measure wasn’t lower than the 0.4% consensus and that the headline rate lifted by 0.6% against 0.5% expected, albeit half the gain was driven by a 10% rise in petrol prices. But the post-Fed big dollar reaction has seen the ‘battler’ sink back to 0.6832, so perilously close to taking out both the January 2016 and June 2019 lows (0.6845 now).

It hasn’t taken POTUS long to get the memo from the Fed and react on Twitter in wholly predictable fashion. He says “What the Market wanted to hear from Jay Powell and the Federal Reserve was that this was the beginning of a lengthy and aggressive rate-cutting cycle which would keep pace with China, The European Union and other countries around the world……..As usual, Powell let us down, but at least he is ending quantitative tightening, which shouldn’t have started in the first place – no inflation. We are winning anyway, but I am certainly not getting much help from the Federal Reserve!”. Expect much more of the same in coming weeks.

In US economic data, the Chicago PMI fell sharply in July, with the 44.4 reading its lowest since December 2015 (and before that, July 2009). The Chicago PMI tends to be more volatile than the other regional Fed surveys, and it’s possible that the ongoing woes at Boeing, which is headquartered in the city, have exacerbated the weakness in Chicago manufacturing relative to other districts. The ADP employment survey was close to expectations (+156k), at a similar level to the market consensus for nonfarm payrolls which is released on Friday night (+165k). Finally, the employment cost index, a broader measure of wage growth than average hourly earnings, was slightly lower than expected. Private sector wages rose at a 3% year-on-year pace in Q2, the same rate of growth in 2018, and suggesting overall wage growth remains in check, despite the tightness of the labour market.

On the trade front, US-China trade talks ended yesterday. There was no sign of a breakthrough, although Chinese state media described the talks as “frank, effective and constructive” and the two sides have agreed to meet again in Washington in September.

Earlier in the night, Eurozone Q2 GDP came in at 0.2% on the quarter as expected with year-on-year growth down to 1.1% from 1.2%, while headline CPI fell to 1.1% from 1.3% as expected following earlier soft German data. Core CPI fell to 0.9% from 1.1%. All these prints merely serve to consolidate expectations of ECB easing when the Governing Council returns from its August recess in September.

There’s a few things to look forward to today, but post FOMC and pre-Friday night’s US payrolls, they do rather pale by comparison.

In our time zone, the Caixin Manufacturing PMI looks like being the highlight, following the small rise in the official version yesterday to 49.7 from 49.6. Consensus is 49.5 from 49.4 last time.

Australia has Q2 Trade Prices, with Import prices seen 1.5% up and Export prices +2.8%, so an implied 1.3% rise in the goods terms of trade. And later today (16:30 AEST) we get the RBA’s July commodity price indices. In SDR terms, the latter is +8.5% up in the first half of the year (thanks largely to gold and iron ore).

Offshore it’s final Eurozone PMIs and the first and only UK Manufacturing PMI – latter seen down to 47.6 from 48.0.

The Bank of England’s latest policy decision should pass without incident amid the even denser fog surrounding Brexit but where downside economic risks from a no-deal Brexit will doubtless be highlighted.

The US has both the Markit then far more market sensitive ISM manufacturing survey, the latter seen up to 52.0 from 51.7. Also Construction Spending and weekly jobless claims.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.