Online retail sales growth slowed in May following a fairly strong April

Insight

The US Fed dropped interest rates by 50 basis points in an emergency cut.

https://soundcloud.com/user-291029717/feds-emergency-cuts-doesnt-halt-the-carnage?in=user-291029717/sets/the-morning-call

Just runnin’ scared each place we go

So afraid that he might show… Just runnin’ scared, feelin’ low – Roy Orbinson

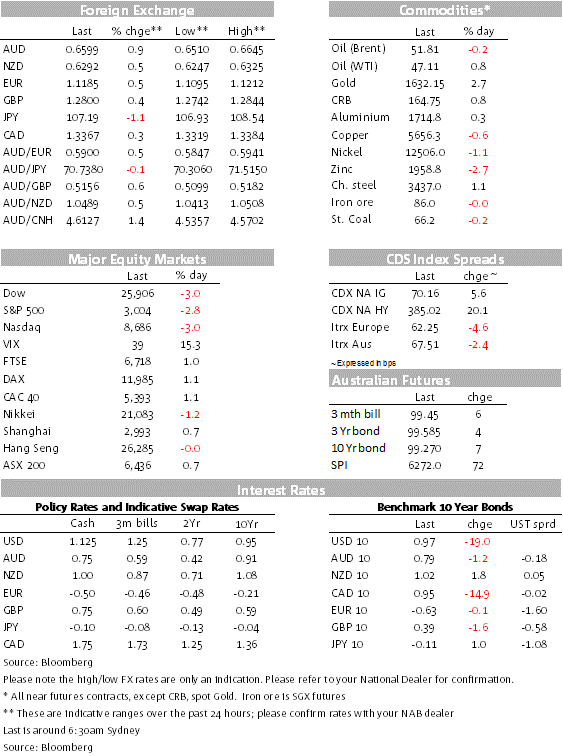

Markets were travelling with a spring in their step hoping for a positive outcome from the G7 Finance Ministers and Central Banks phone hook-up. In the end, the meeting failed to deliver anything concrete, but a couple of hours later the Fed stepped in with a 50bps rate emergency rate cut. After a brief boost ,Fed Chair Powell’s assessment of COVID-19 spooked markets triggering a massive sell-off in US equities and a fall in UST yields with the 10y note falling below the 1%. The USD is broadly weaker amid fall in yields and spike in volatility. AUD outperforms, up 1.10% and briefly trades above 66c.

The lack of any concrete measures from the G7 group of central bank governors and finance ministers was a disappointment for markets. After the much anticipated phone-hook up, the G7 Group reiterated their commitment to use all policy tools to achieve strong, sustainable growth and safeguard downside risks, but avoided any specific policy announcements. In the end, however, the big overnight moves came a couple of hours later following a surprise 50bps rate cut announcement by the Fed, which lowered the Fed Funds to a range of 1% to 1.25%. After a brief boost, US equities embarked on a sharp free fall ( S&P now down 2.87% as we type) while UST yields accelerated their decline with the 2y note down 20bps to 0.71% and the 10y note down 17bps to 0.99%, the latter briefly traded to an intraday low of 0.9235% just over an hour ago.

The big turn in sentiment appears to have been driven by the bleak assessment from Fed Chari Powell at the Press Conference following the rate cut announcement. Although Powell was at pains to emphasise that “The fundamentals of the U.S. economy remain strong”, he also noted that the magnitude and persistence of the coronavirus remains uncertain and will weigh on activity for some time. In addition, the Fed Chair also admitted that the Fed doesn’t have all the tools to deal with the negative impact from COVID-19, “We do recognize a rate cut will not reduce the rate of infection, it won’t fix a broken supply chain. We get that,” Powell said. “But we do believe that our action will provide a meaningful boost to the economy.”

Powell’s comments have delivered a reality check for markets, but also highlight the need for fiscal side to do more. As the Fed Chair noted, the Fed does not have all the answers, a 50 bps rate cut is a positive move and should help ease some of the pain by lowering the cost of capital. But access to capital is also a concern, particularly for those sectors in the economy directly affected the virus outbreak (tourism for instance and in some countries like Australia, education as well). On this score, worth noting Powell’s emphasis on the need for a multi-faceted response from governments, health care professionals, central bankers and others to stem the human and economic damage.

Cleveland Fed President Loretta Mester said that “The underlying fundamentals of the U.S. economy remain strong, but the coronavirus will weigh on U.S. growth at least during the first half of the year, with a pullback in spending by households and businesses,” . We think the Fed has left the door open for more easing ahead, including as early as the schedule meeting on March 17-18. “In the weeks and months ahead we will continue to closely monitor developments,” Powell said.

The sharp decline in UST yields and increase in market volatility have been a deadly combo for the USD. Prior to all of this uncertainty, the over valuation of the USD was helped along by it appeal as a carry currency vs other G10. The u turn in the volatility environment alongside a sharp decline in UST yields are now a bid headwind for the greenback. The USD is broadly weaker with DXY down 0.24% and BBDXY down 0.38%.

Fundamentals of the EU economy were already looking fragile prior to the COVID-19 outbreak and the lack of a clear fiscal plan has not been encouraging either. So why is the euro going up? We think a reversal of carry trades with the euro the most appealing funding currency, has helped the union currency move up from just below 1.08 a fortnight ago to 1.1173 currently. Potentially this move still has a bit more to go.

Yesterday the RBA cut the cash rate by 25bp to a new record low of 0.50% and retained an easing bias. The AUD popped a bit higher immediately after the announcement reflecting disappointment by some in the market that were hoping for a 50bp cut ( about 22% priced). The pair drifted higher over the course of the night and then briefly popped about 66c following the Fed announcement and Fed Powell press conference. Thus much of the AUD strength can be explained by the broad USD weakness. AUD now trades at 0.6596.

Late yesterday, Australia’s PM Scott Morrison confirmed that the Federal Government’s plans to shield the economy from the coronavirus fallout with an fiscal package to be announced ahead of the May Budget. This is a positive as until recently the government has been reticent to increase expenditure placing quite a bit of focus on achieving a surplus instead. This rhetoric no looks to have shifted, however those expecting a big fiscal bazooka are likely to be disappointed, last night the PM told 7.30 ABC report that the plan will be “targeted,” “measured” and “scalable” to prepare Australia’s economy against the virus that has shaken global financial markets and practically shut down China’s economy. NAB still sees a role for additional monetary easing, forecasting a follow-up rate cut in April.

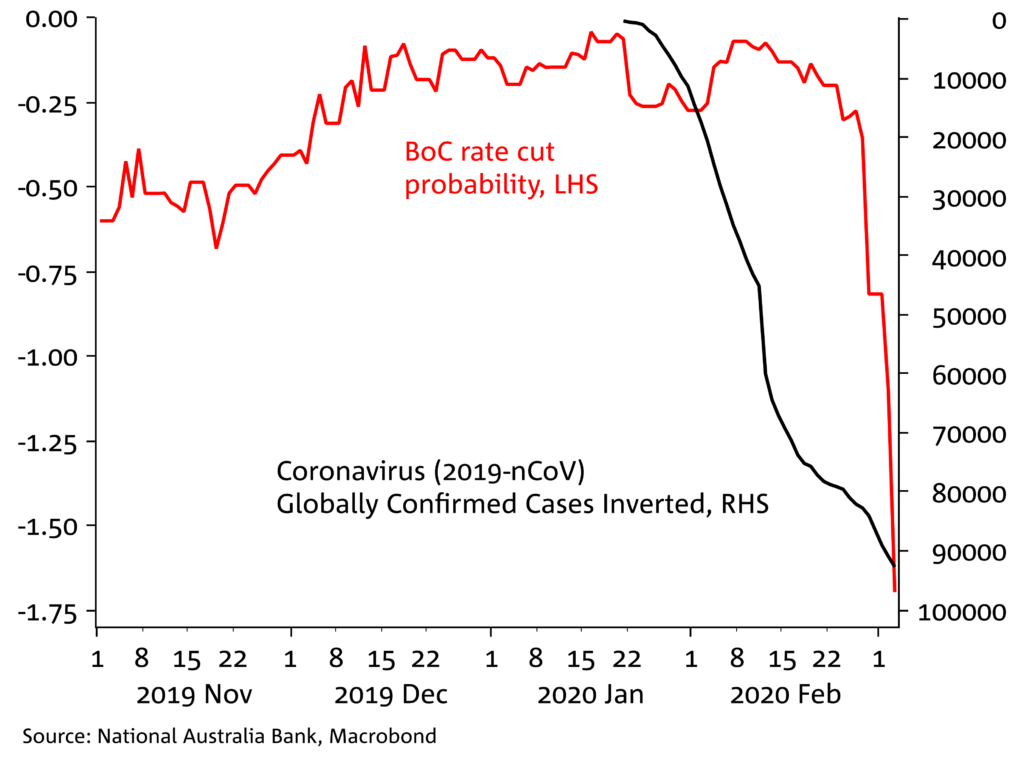

BoC next cab off the rank

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.