Total spending grew 0.9% in June.

Future contracts for Fed funds turned negative for the first time.

https://soundcloud.com/user-291029717/fed-fund-futures-turn-negative-boe-talks-uk-back-to-1706?in=user-291029717/sets/the-morning-call

“But I keep cruising, can’t stop, won’t stop moving; It’s like I got this music in my mind, sayin’ it’s gonna be alright” Taylor Swift 2013

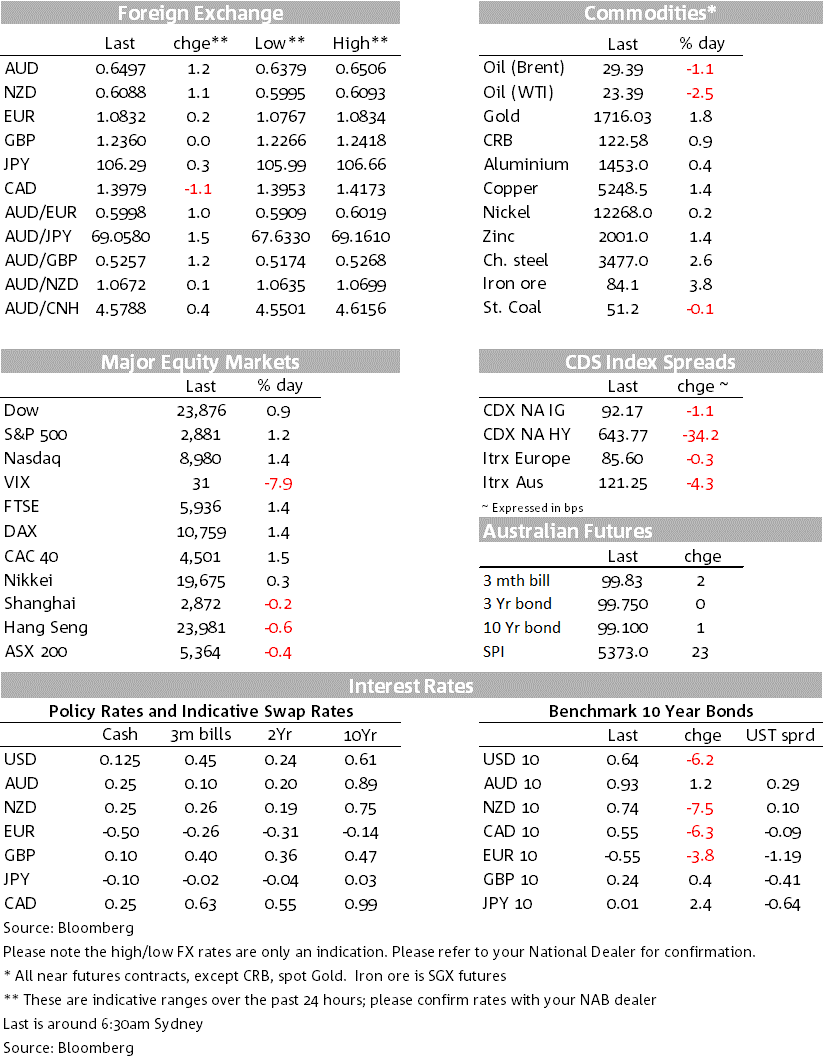

Later tonight the US unemployment rate will likely hit 16% with 21.7m jobs lost due to COVID-19 lockdowns. While the deterioration is known, many will be asking whether risk sentiment can stand such a sticker shock? For now equities continue to be buoyed by hopes that we are passed the bottom given containment rollback with the S&P500 +1.2% overnight (the Fed’s Barkin was the latest making the point we may be passed the bottom: “If you were to pick a date that would be the trough of this downturn we are probably right there….There is only up from here”). . Reinforcing notions the US is rollback measures despite the track of the virus, President Trump has pledged to shift resources to re-opening. Better than expected Chinese trade data also added to hopes of a rebound following rollback, while news that US Trade Representative Lighthizer and Chinese Vice Premier He would speak as soon as next week helped ease concerns over US-China trade G10 FX continues to reflect the more positive tone with the global growth proxies of AUD (+1.2%), NZD (+1.1%) and CAD (USD/CAD -1.1%) higher, and the USD on the backfoot (DXY -0.3%).

Rates markets are now toying with the possibility of the Fed needing to do more and taking rates into the negative (Fed Funds Futures price a small chance of negative rates by the end of the year; negative 1-2bps by year’s end). There doesn’t appear to be an obvious driver and Fed officials overnight downplayed the prospects (Fed’s Barkin: “I think negative interest rates have been tried in other places and I haven’t seen anything personally that makes me think they are worth a try here”). Market participants think there is a risk though and high profile bond investor Gundlach tweeted “the pressure to go negative on Fed Funds will build as short term borrowing explodes and dominates. Please, no. Rates < 0 = Fatal.” Intellectual firepower for the argument also came earlier in the week by Rogoff (see The Case for Deeply Negative Rates). Bond yields are also ratcheting up rate cut expectations with US 2-year yields falling -5bps to 0.1% and 5-year yields -8bps to 0.29%, both all-time lows. The US 10yr yield fell -7.3bps to 0.63%.

The USD was on the backfoot with the DXY -0.3%, though still within its April range. The EUR rose 0.2%, supported by President Lagarde pushing back on the recent ruling by the German Constitutional Court which had ordered a proportionality assessment of the public sector bond buying program. Lagarde said the ECB was “undeterred” and that the institution is “answerable to the European Parliament…we will continue to do whatever is needed, whatever is necessary, to deliver on that mandate.” Italian 10yr yields retraced some of their moves following the Court ruling, down -6bps to 1.91%.

G10 global growth proxies continue to outperform with the AUD +1.2% and the NZD +1.1%. Better than expected trade data from both Australia and China helped buoy sentiment. The Australian Trade Balance yesterday shot the lights out with exports to China playing catch-up after recent lockdowns, reaching $10.6bn in March up from $3.9bn in February and well up on the $6bn consensus. Commodities drove the surge with a 24% volume-driven rebound in iron ore and a sharp 225% rise in the non-monetary gold exports. Chinese Trade data also beat expectations by a considerable margin with exports up 3.5% y/y against the consensus of a -11% decline. It is likely firms were working through export backlogs, and all eyes will be on whether this can be sustained given very weak new export orders from the recent PMI surveys.

The positive trade sentiment was reinforced overnight by reports that US Trade Representative Lighthizer and Chinese Vice Premier Liu would speak as soon as next week on implementation of the Phase-One US-China trade deal (see SCMP for details). The call will be the first since the phase-one deal was signed in January and provides some comfort to markets which had grown concerned about renewed tensions over trade as well as Trump’s doubts over the origin of COVID-19.

US Jobless Claims came in at 3.2m v. expectations of 3.0m and over the past seven weeks jobless claims have risen by some 33.5m and equivalent to around 20.5% of the entire US labour force filing for unemployment benefits. If you were to look for a positive, the new filings have been steadily falling over recent weeks. Consumer Credit statistics also disappointed coming in at -$12bn against expectations of a rise to +$15bn and perhaps a pointer to tighter credit conditions.

The BoE and the Norgest Bank met. The Norges Bank surprised markets by cutting its cash rate from 0.25% to 0%, though did not envisage making further cuts. Despite the surprise cut, the Norwegian krone has been the top performing currency over the past 24 hours, up almost 2%. Oil prices rose earlier in the session after reports that Saudi Aramco had increased its pricing for oil to be delivered in June, but that move has since completely reversed with Brent Oil now -1.1%.

They refrained from adding more stimulus in a 7-2 vote. Analysts expect the BoE to upsize its QE programme over the next few months though, with the Bank set to reach its bond buying target as soon as July, if it carries on at its current pace. The Bank said it expected growth to fall 3% in Q1 and 25% in Q2 but Governor Bailey struck a relatively upbeat tone, saying he expected activity to bounce back “much more rapidly than the pullback from the global financial crisis”. The Bank said it expected “only limited scarring to the economy”. Time will tell.

All focus this morning will be on the RBA SoMP where the RBA will publish its forecast track for the economy along with two scenarios. The National Cabinet also meets today and is widely expected to announce a plan to rollback containment measures with the aim to have most of the economy open by the end of July, except for international flight which will be restricted likely until a vaccine/effective treatment for COVID-19 is found. International focus will be on US Payrolls where jobs are expected to fall 21.7m, pushing the unemployment rate up to 16% from 4.4%.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.