Total spending grew 0.9% in June.

Fed warns of considerable medium-term risk.

“I got that boom boom boom; That future boom boom boom; Let me get it now; Boom boom boom (Gotta get that)”, Black Eyed Peas 2008.

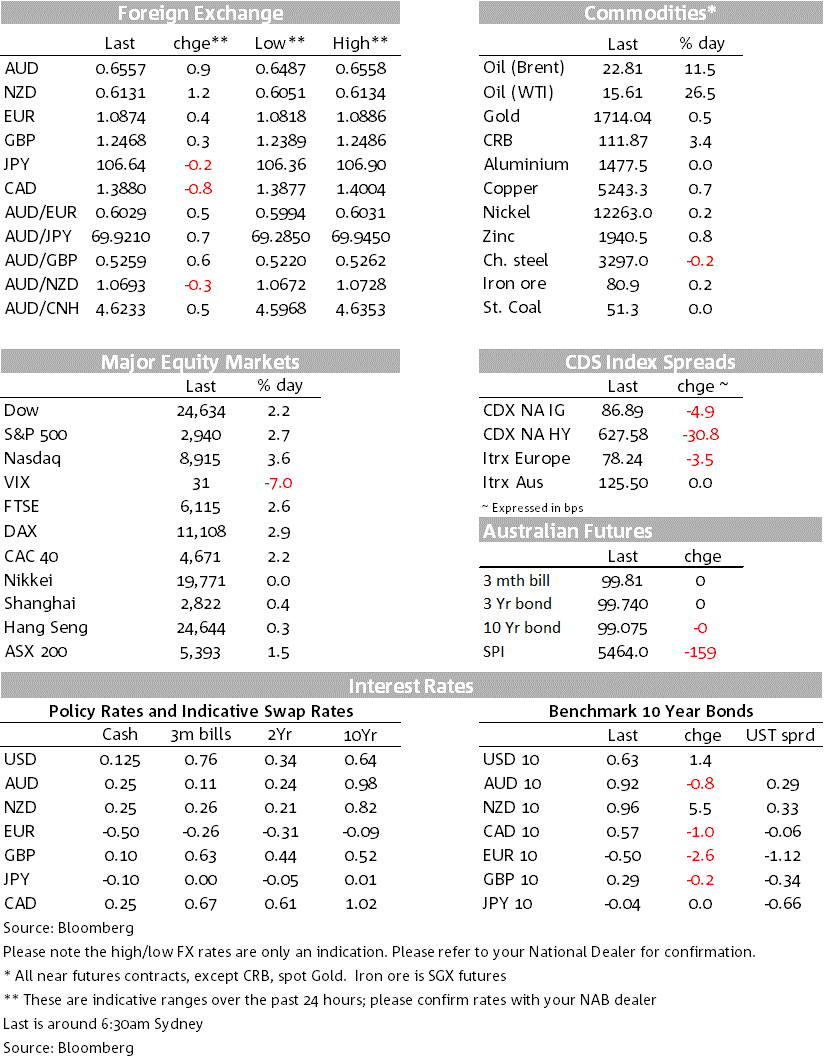

In the words of the Black Eyed Peas, equities went boom boom pow overnight (S&P 500 +2.7%) with the pow coming from positive trial results of Gilead’s Remdesivir. The US FDA is said to be fast-tracking approvals for the drug and it is hoped that if it is an effective treatment, it could facilitate a quicker and greater rollback of containment measures. Also supporting sentiment were positive tech earnings and a surprise fall in gasoline inventories. The Fed and a negative US Q1 GDP print had little impact on markets. In FX, global growth proxies rallied sharply with NZD +1.2% and AUD +0.9%, while the USD (DXY) was on the backfoot down -0.5%. Yields though were broadly steady, while oil surged in what has been a volatile couple of weeks (WTI June +26.5%).

Two studies found the drug was an effective treatment for COVID-19 in placebo-controlled trials. The first trial by the US National Institute of Allergy and Infectious Diseases (NIAID) saw 31% of patients seeing an improvement and recovering on average of 11 days compared to the placebo of 15 days. Dr Fauci who heads the NIAID said the preliminary results were “very optimistic” and that the drug had shown “clear-cut positive effect in diminishing time to recover”. A second study by Gilead themselves saw similar results for those patients receiving a shorter 5-day treatment as compared to a 10-day treatment (see Gilead for details).

While a treatment is not vaccine, a successful treatment would be a game changer for the virus and would help facilitate a greater rollback of containment measures. It could also give consumers greater confidence to resume pre-pandemic activity which is important given the consumer has lagged the recovery in China. Fast-tracking of the drug looks likely with the U.S. Food and Drug Administration indicating it is in talks to make the medicine available quickly with the New York Times reporting emergency authorization could be given as soon as Wednesday.

Equities surged on the news with the S&P500 +2.7%. Positive earnings from the tech sector and a recovery in oil also added to the rally. All sub-sectors rose apart from utilities and staples, a sign of broad-based optimism. In terms of earnings, Alphabet reported late Tuesday with revenue beating expectations and commentary in the earnings call noted they are seeing “early sings” of users “returning to more commercial behaviour”. Facebook and Microsoft also reported strong numbers after the close with shares up in after-market trading (Facebook +7%, Microsoft +1.5%).

Energy stocks outperformed (+7.4%) with WTI up 23%, both on hopes for a quicker recovery in global growth and news that gasoline inventories had unexpectedly fallen last week (gasoline inventories fell 3.7m barrels against expectations of a build of 2.5m). Oil though continues to be volatile.

The Fed also met overnight with no big surprises apart from not changing the rate on IOER. The target range was kept at 0-0.25% and in Powell’s words “we are not changing that guidance today”. On IOER, many had expected with the effective Fed funds rate trading down near 0.04%, IOER could be lifted by 5bps. With no change to the rate, overnight repo markets did trade 2-3bps lower. In the press conference Chair Powell said the Fed’s pace of bond buying, under its QE programme, had been pared back as market function had improved and it would continue to use its tools as needs be. Powell also said rates would be kept at current levels until the economy was on track to achieve its targets (of maximum employment and price stability), which is likely to be a long time. Yields overall were little moved by the Fed, or the risk-on rally with US 10yr yields +1.4bps to 0.63%.

US GDP also took a backseat with the Q1 contraction coming in as largely expected at -4.8% annualised against the -4.0% consensus. Of course, the worst is yet to come with expectations that Q2 GDP might fall by around 30-40% annualised. The Q1 contraction was driven by consumption (-7.6%) and business investment (8.6%), partly offset by a leap in housing investment (+21%) and net trade (contributing 1.3% points with imports falling faster than exports). The sharp fall in consumption was driven by services (-10.2% and largest decline since at least 1947) with goods spending down by -1.3%. That overall suggests the burden of the lockdowns has fallen on the services sector and lines up with the more disastrous readings coming from the services PMIs globally.

The USD was on the backfoot with DXY -0.5%. Global growth currencies led the rally with NZD +1.2% and AUD +0.9%, while CAD was supported by oil with USD/CAD -0.9%. Other major pairs also rose with EUR +0.4%, GBP +0.3% and USD/YEN -0.2%. Yesterday’s Australian CPI figures also gave some support to the Aussie (Headline was 0.3% q/q and trimmed mean 0.5%), though is somewhat academic as Q2 CPI will fall sharply as the virus starts to have an effect, with the main initial impact coming from the govt introducing free child care, at least temporarily.

Most focus this morning will be on the Chinese PMIs (due around 11.30am AEST) to see whether last month’s bounce in activity is sustained and whether there is a continued pick-up in the non-manufacturing sector. Domestically there is little on the radar apart from the RBA’s Credit Statistics (also 11.30am). Focus than shifts to Europe with Q1 GDP, CPI and ECB. US Jobless Claims will also continue to be scrutinised, while earnings season continues with Amazon and Apple (amongst others) scheduled to report. Key prints today:

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.