We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

The US Fed has reiterated that they will do whatever it takes to protect the US economy, with inflation expected to remain below 2 percent through to 2022.

People talkin’ about us, They got nothin’ else to do. When it all comes down we will, Still come through

In the long run, Ooh, I want to tell you, it’s a long run – Eagles

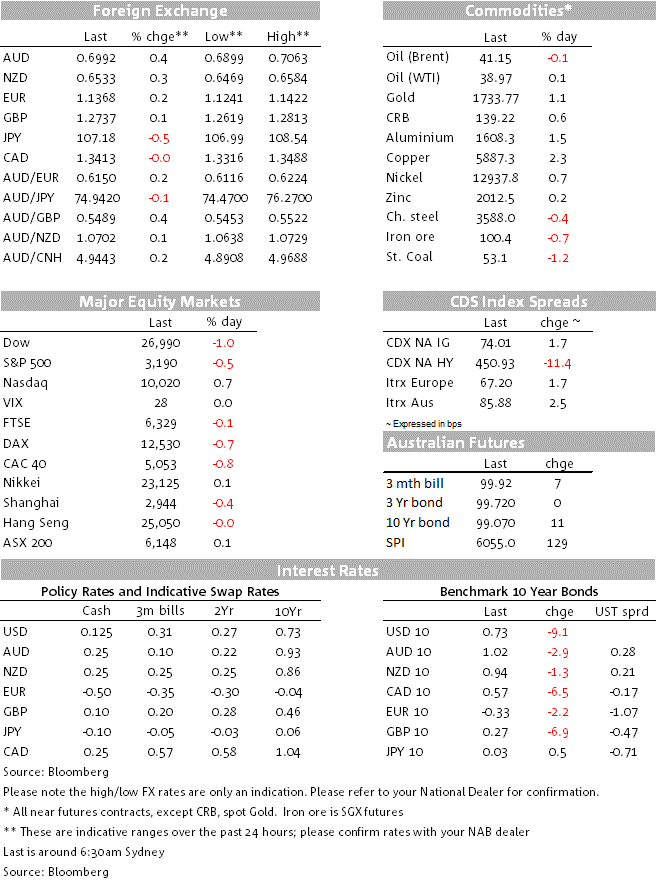

The Fed left the Funds rate target unchanged at near zero. The Statement expressed no intentions to change the policy setting for a while with the new dot plot reaffirming this view. All officials see no change in rates through 2021 and only two expect a rate hike in 2022. The FOMC Statement sees the S&P 500 briefly trade in positive territory, but Fed Chair Powell subdued assessment of the economic outlook shifted the mood leaving the equity benchmark marginally in the red. The USD ends the day weaker across the board with the AUD and NZD making new COVID-19 intraday highs before easing into the close. The UST curve bull flattened with the 10y rate down 5bps to 0.7263%

The FOMC reiterated its full commitment to use all its tools to support the economy and in doing so it intends to keep its ultra-easy policy setting unchanged for a long time. The Statement reiterated “The ongoing public health crisis will weigh heavily on economic activity, employment, and inflation in the near term, and poses considerable risks to the economic outlook over the medium term”.

The Fed reinforced its commitment to maintain “smooth market functioning” by promising to maintain its Treasury and mortgage purchases “at least at the current pace”. The current pace of UST purchases is around $80bn p/m and about $40bn p/m of MBS. The implication is that more QE is possible if longer dated yields continue to rise. Powell also mentioned in his press conference that they will continue to review the asset purchase forward guidance, that they have been studying the international evidence on yield curve control. The Fed Chair also told reporters that such discussions will continue at upcoming meetings. Economists surveyed by Bloomberg expect them to consider adopting the strategy later this year.

The FOMC assessment of the US economy was also little changed. The virus and containment measures were still seen to “have induced sharp declines in economic activity and a surge in job losses.” Inflation is still viewed as being held down by lower oil prices and weak demand. On a more positive note, the Statement noted that, ‘financial conditions have improved, in part reflecting policy measures to support the economy and the flow of credit to US households and businesses.’

The new median forecast show GDP growth slowing to -6.5% in 2020 followed by a rebound to 5.0% in 2021 and 3.5% in 2022. Although it is notable that there is a huge range in the numbers, for instance GDP for next year ranges from -1% to +7%, and unemployment from 4.5% to 12% . After a big jump in the unemployment to 9.3% in Q4-20, the median forecast shows a decline to 5.5% is expected by the end of 2022. Core PCE is seen at 1% at the end of 2020 and 1.7% at the end of 2022. So with both unemployment and inflation (Core PCE) below the FOMC targets at the end of 2022, the funds rate is not expected to change over the next two and half years, although this assessment does not prevent an earlier start to Quantitative Tightening, which could be possible if by then the economy was seen to be heading towards maximum employment and price stability.

Fed Chari Powell delivered a sombre assessment of the US economic outlook. Powell noted that while the May’s jobs data were unexpectedly positive, “it’s a long road”, then adding that the pandemic could inflict longer-lasting damage on the economy. He also remarked that the central bank has been unable to get inflation to its 2% target even during the 128-month expansion that just ended.

The FOMC Statement and Powell’s comments rattle the US equity markets. After jumping into positive territory on the Statement, the S&P 500 ended the day down 0.53%. The tech-heavy Nasdaq Composite index, on the other hand, ended the day 0.67% higher and at a new record high. Early in the sessions abd ahead of the FOMC decision, European equity markets traded in and out of positive territory, but in the end all major regional indices ened the day with negative returns. The Stoxx Europe 600 Index closed down 0.4%, marking the biggest three-day drop since May 15.

After a down and up reaction to the FOMC and Powell, the USD ended the day weaker across the board. The BBDXY index is now 0.50% lower relative to levels this time yesterday morning and DXY is -0.31% trading at 96.081 as I type. Technically both USD indices still have room to trade lower and when we look at major currency pairs such as the euro, the USD also look vulnerable. The euro now trades at a1.1376, after printing an overnight high of 1.1422. The euro’s previous high on March 9 was 1.1495.

The AUD and NZD have also performed against the USD. The AUD currently trades at 0.6998, up 0.69% in the past 24hours. Reaction to the FOMC saw the AUD trade to a new COVID-19 high of 0.7063 before easing as the USD regained some ground into the close. The NZD traded in a similar pattern, printing a new COVID-19 high of 0.6584 and now trades at 0.6536 ( 0.49%).

Reaction to the FED and Powell has resulted in a bull flattening of the UST curve with the 10y note 5bps lower relative to pre FOMC levels at 0.725%.

The WSJ reported that the US government plans to fund and conduct decisive studies of three experimental coronavirus vaccines starting next month, according to a lead government vaccine researcher. The phase 3 trials will involve tens of thousands of subjects, marking the final stage of testing. The timetable suggests researchers are making rapid progress, advancing their vaccines through earlier stages of testing. To that list we can add Pfizer, which is outside of the government programme and is also due to start phase 3 testing as early as next month.

The US core CPI fell for the third consecutive month and slightly undershot market expectations, dragging down the annual increase to 1.2% yoy, the weakest in nine years. The deflationary pulse should ease from here, as activity levels pick up, but a large negative output gap should ensure that weak inflation remains an enduring theme. Weak inflation data from China – with PPI deflation approaching 4% – suggested that the country was still “exporting” deflationary pressure around the world.

The OECD published a forecast update which showed two equally probably scenarios – global growth down 6% in 2020 if a second wave of COVID19 infections can be avoided or falling 7.6% if a second wave before the end of the year leads to renewed lockdowns. Under either scenario, world GDP won’t be back at end-2019 levels until at least two years.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

Economic and financial market update

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.