NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

There was more reaction to the FOMC meeting with bond yields rising sharply.

https://soundcloud.com/user-291029717/fed-pushes-bond-yields-up-russia-drives-oil-down?in=user-291029717/sets/the-morning-call

Now you’ve worked it out, And you see it all

..And you want to shout, How you see it all – R.E.M.

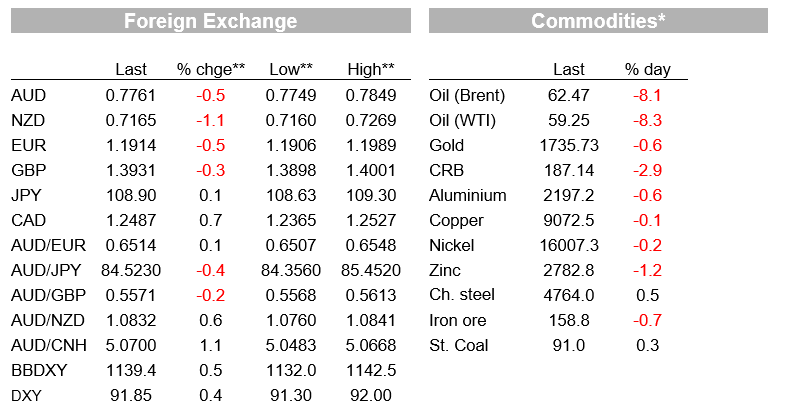

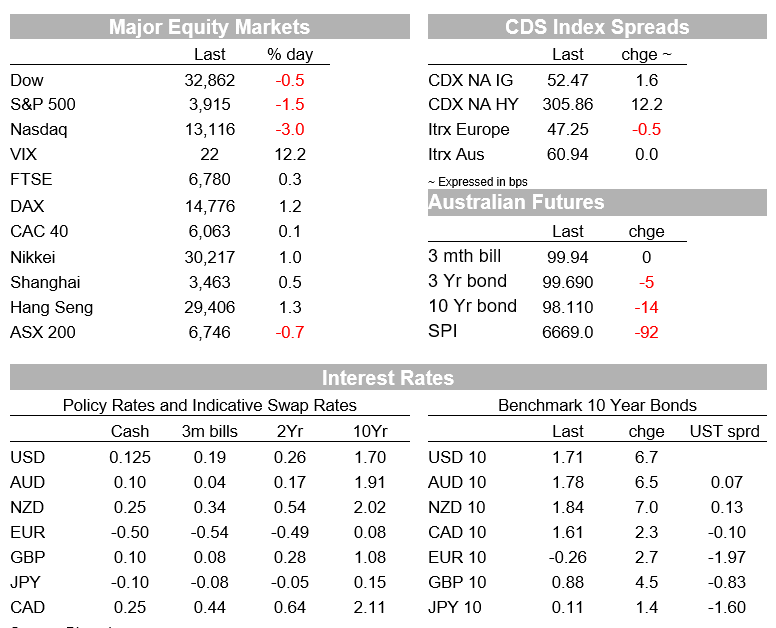

FOMC aftermath sees longer dated UST yields make new highs with 10y UST yield leading the move up, now trading at 1.71%. US equities don’t like the spike in yields with tech shares leading the decline, NASDAQ down ~3.0%. USD reverses post FOMC losses supported by a safe-haven bid and higher UST yields. NZD and NOK the big G10 underperformers, the latter feeling the pain from the slump in oil price, in spite of the Norges Bank signalling the prospect of a rate hike later this year.

After some navel gazing, the UST Treasury market has concluded that the Fed is not poising any challenges or discomfort for longer dated UST yields to keep pushing higher in a quest for finding a new higher equilibrium given the Fed’s higher tolerance for a “temporary“ overshoot on inflation and the Bank’s new mantra of “seeing is believing”. This means the Fed will not act on its forecast and instead it will wait for the data to corroborate its expectations over the speed of recovery. Longer dated UST yields are likely to be more sensitive to the economic and inflation narrative from incoming data releases while the front end remains anchored by a Fed funds rate unlikely to go anywhere any time soon.

This all sounds very dandy, but there is also the risk that a rapid rise in longer dated UST yields become a source of market instability triggering a tightening in financial conditions . For now, unlike the ECB, the Fed is not too concern interpreting the current rise in longer dated UST yields as a reflection of the market pricing in an improvement in the US economic outlook. Thus, against this backdrop, overnight we have seen the 5y, 10y and 30y UST make new cycle highs (0.8669%, 1.7526% and 2.5040%), although in the past couple of hours the move up yields has lost momentum with the 10y now trading at 1.7099%. On this point, it is interesting to note that if we decompose the move in 10y UST yields, it has all come from a move up in the real component with the breakeven component little changed. No doubt the move lower in oil prices has been a factor at play.

Oil prices are having a tough day, down over 8% with some analysts noting concern over rising tensions between the US and Russia, as well as concerns over Europe’s economic recovery . With the US threatening sanctions, analyst are speculating Russia could retaliate by flooding the market with oil. Slow vaccine roll outs and new lockdown measures in Europe are also a demand concern. Overnight, French President Macron announced the government decision to lock down several regions including the Paris area, in order to contain a third wave of the covid epidemic.

Higher bond rates and steeper curves have driven further sector rotation in equity markets, with Europe’s bank-heavy Stoxx 600 index showing further gains (+0.4%), while US equities are weighed down by underperforming big tech stocks – the S&P500 index is currently down around 1.45% while the NASDAQ index is down around 3.0%.

Moving onto currencies, the USD regained its mojo reversing its post FOMC losses with the move up in UST yields and risk aversion in equity markets supporting the move. BBDXY and DXY are up around 0.45% and now trading at 91.875 and 1139.39 respectively.

GBP and JPY have largely held their ground against the USD. Despite the high global rates backdrop, which would normally be negative for JPY, the currency has seen some support since the Nikkei reported that today the BoJ will amend the 10-year JGB target band to plus or minus 0.25% and scrap the ¥6b annual buying target of ETFs. USD/JPY trades at ¥108.889.

Meanwhile GBP didn’t experience an adverse reaction from the BoE policy meeting . The Bank’s latest policy update came and went with little market reaction, with the message as expected. The Bank upgraded the outlook for the UK economy but is not looking to tighten policy until “significant progress” is made in eliminating spare capacity and achieving the 2% inflation target sustainably – joining the chorus of other major developed central banks singing the same tune, basing policy on the rear vision mirror rather than projections.

The AUD now trades at 0.7762, weighted down by the negative turn in equity sentiment and higher USD. The pair is still up relative to levels post FOMC, but almost a cent lower from yesterday’s high of 0.7849, post the stellar Labour force report, The Australian labour market report was another blockbuster, with strong employment driving the unemployment rate down 0.5 percentage points to 5.8%, much lower than expected.

The NZD has been the worst of the majors, falling 1% overnight 0.7163. My BNZ colleague, Jason Wong noted that yesterday NZ Q4 GDP came in much weaker than expected at minus 1.0% q/q, but this came on the back of the surge in activity in Q3 (revised down a touch to 13.9% q/q). The data are so dated and volatile of late, there was only a small market reaction, with the rates market slightly reducing the chance of a rate hike from early next year. The story remains one of the NZ economy struggling to gain further traction after the strong post-lockdown bounce-back, given the hit to global tourism during the summer peak, while Q1 will be affected by the couple of temporary lockdowns. Confidence and tourism will lift in Q2 if the borders reopen as soon as next month, which has been hinted by government officials.

The euro is down 0.53% to 1.1913 and is still trading close to the bottom of its 1.1845 to 1.2243 recent range. The union currency showed little reaction to the news that the European Medicines Agency said that there was a “clear scientific conclusion” that the Oxford/AstraZeneca vaccine was “safe and effective” and that the vaccine was “not associated” with an increased risk of blood clots, adding that the benefits of the vaccine outweighed any possible risks. The announcement will pave the way for EU countries to reinstate the use of the vaccine and get the programme back on track. In the last hour, Italy said that it would restart the AstraZeneca vaccination programme on Friday.

Overnight ECB chief Lagarde urged EU government to get on with rolling out their fiscal spending plans in the coming to ensure the region’s recovery. the backdrop is the slow vaccine rollout and for some govts a need to properly finalise plans tied to the EU’s Next Generation relief fund, so that disbursement can begin by end Q2. Lagarde once again warned the ECB will try and crimp yield rises via bond purchases and that yield rises are unwarranted and could act as a brake on the recovery. Lagarde joins her collegues Schnabel and Slovak cbk/ECB Kazimir in warning the EU is rolling out its fiscal stimulus too slowly.

Finally, NOK is the big G10 underperformer, down 1.22%, undoubtedly weighed down by the sharp decline in oil prices. Notably, however, overnight Norway’s central bank brought forward the timing of what will probably be the rich world’s first interest rate increase since the pandemic broke out. The Oslo-based bank kept its main rate unchanged at zero on Thursday, as predicted, saying it now expects to start raising its benchmark deposit rate in the “latter half” of this year.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Confidence and Conditions Lift

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.