Online retail sales growth slowed in May following a fairly strong April

Insight

The Federal Reserve cut rates but didn’t give a clear indication of further cuts or promise the return of QE.

https://soundcloud.com/user-291029717/fed-turns-hawkish-bank-liquidity-problems-continue-oil-slides-further?in=user-291029717/sets/the-morning-call

They’re tearing us apart, They’re breaking up my heart – Eric Clapton

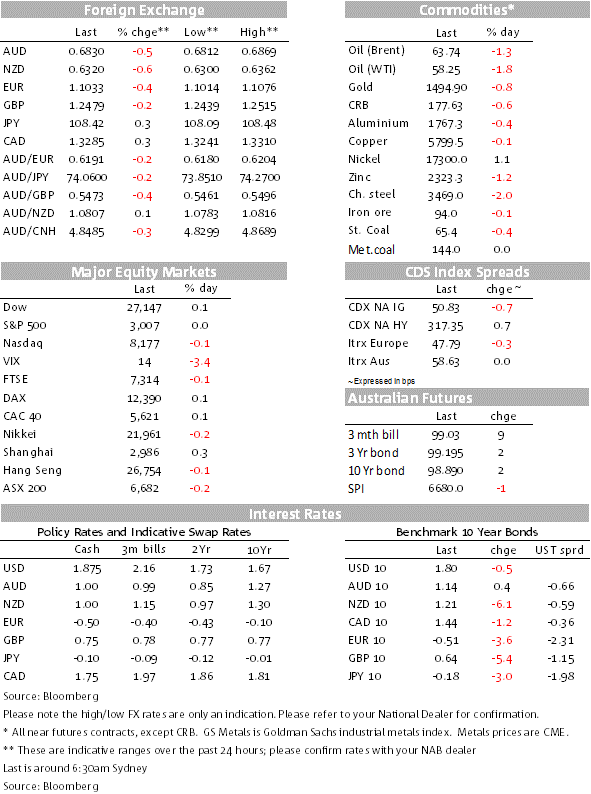

As usual markets marked time ahead of the FOMC decision while reaction to the 25bps Fed funds rate cut and hawkish statement (relative to expectations) has been mixed. The US equity market welcomed the rate cut and ignored the hawkish tone in the announcement while the bear flattening in the UST curve reflected bond investors’ disappointment. The move higher in UST yields initially boosted the USD, but following Fed Chair Powell’s conference remarks stressing that if “the economy weakens, more extensive cuts may be needed”, the USD has started to give back some of its early gains. Dissentions and Divergence in the new dots plot also highlight a growing division between officials. True to from President Trump didn’t waste time and had another go at Powell and the Fed.

The FOMC lowered the Fed funds rate by 25bps to 1.75-2.0% as expected and in light of stresses in the money markets, officials also lowered the excess reserve rate by 30bps to 1.80%, a decision that should help keep the effective Fed Funds rate within the range. Changes to the economic projections were minimal, reinforcing the view that as a base case no further easing will be required. That being said with core PCE only expected to reach 2% by 2021 and stay at this level in 2022, in addition to the US led trade uncertainties on the US and global growth outlook, is probably fair to say the Fed’s inflation outlook is not an impediment for further easing.

The message of no further easing as a base case was also evident in the median dot plot, which reflected the 2 rate cuts since June this year and an unchanged Fed Funds rate at the end of both 2019 and 2020, followed by a modest tightening in 2021 (from current mid-point of 1.875% to 2.125%) and then some more in 2022 ( to 2.125% to 2.375%).

But as it is often the case the devil is in the detail. For one the Statement highlighted the downside risk to the outlook, as much as the statement noted the “Committee’s view that sustained expansion of economic activity, strong labor market conditions, and inflation near the Committee’s symmetric 2 percent objective are the most likely outcomes” the statement also noted that stressing that “uncertainties” about this outlook.

Similarly as much as the median dots don’t show further rate cuts, seven out of 17 officials have one more easing this year. This plot divergence is comparable to the pattern seen in the June dot plot and of course a month later we got a rate cut in July. Just as interestingly, however, the dot projections, which were submitted last week, show that five officials did not have a rate cut pencilled in for this month. Finally the remaining dots show 5 members believed the range should not have been lowered. So there is a clear divergence of opinion and in contrast the market still fully prices another full rate cut by the end of the year and a further 40bps of easing through next year.

In his opening address at the press conference, Chair Powell remained positive on the economic outlook and argued that today’s rate cut was to provide “insurance” against the risks. When asked if this was still a mid-cycle policy adjustment, he agreed but offered that if the economy weakens then a more extensive series of rate cuts could be appropriate. When asked whether the FOMC still had an easing bias, Powell said “we don’t” and argued that policy will be data dependent.

Reaction to the FOMC decision has been somewhat mixed. The US equity market was drifting lower prior to the announcement, but then all major equity indices reacted positively to the annoucemenet. The Dow (+0.13%) and S&P 500 (+0.03%) managed to climb their way back into positive territory while the NASDAQ lagged a bit behind closing at -0.11%.

UST yields were drifting lower ahead of the meeting, but reaction to the “hawkish rate cut” triggered a curve bear flatting with the 2y year rate jumping from 1.6595% to 1.7621% ( 10.2 bps higher) while the 10y note moved from 1.74% pre announcement to 1.796% currently.

The USD benefited from the move higher in UST yields and enjoyed gains across the board. Relative to levels this time yesterday, DXY is 0.33% higher at 98.579 while BBDXY is +0.25 to 1210.08. NZD and AUD are at the bottom of the leader board down around 0.55% at 0.6321 and 0.6828 respectively, both have recovered a little bit of ground post the FOCM announcement with NZD making an overnight low of 0.6300 and a low AUD 0.6812. Today our expectations is for a soggy New Zealand’s Q2 GDP print and we also see Australia’s unemployment ticking up one tenth to 5.3% ( see more below). Both calls are below consensus and if our economists are right, the AUD and NZD are likely to struggle today.

In other news, President Trump tweeted that he had instructed the Secretary to the Treasury to substantially increase sanctions on Iran. Both the US and Saudi Arabia believe Iran was behind the strikes on Saudi oil facilities, with the US’s Pompeo saying he had “high confidence” in this and Saudi Arabia’s defence ministry saying the attacks were” unquestionably sponsored by Iran”. Oil prices have continued to ease off as Saudi production comes back on line, with Brent crude down nearly 2% to USD63.40, now up only 5% from the pre-attack level.

US economic data continued to surprise on the high side, with housing starts and permits both surging to their highest level since 2007, fuelled by lower mortgage rates. UK inflation was much softer than expected, with annual core CPI inflation down to 1.5%. The BoE meets tonight, but any policy decisions are on hold until the fog of Brexit clears. Core Canadian CPI inflation remained steady at 2.0%, supporting the view that the BoC can hold its ground longer before joining the easing party.

That being said, we think Japan’s economy has significant challenges ahead. US led trade woes are likely to exert further downward pressure on the external side of the economy and the October sales tax increase is an additional headwind. There are also signs of potential weakness in the labour market. Unless we see a material improvement in US-China trade tensions, all these dynamics suggest the BoJ will be forced to reassess its position later in the year.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.