Online retail sales growth slowed in May following a fairly strong April

Insight

The least surprising news today is the decision by the FOMC to keep rates on hold in the US.

https://soundcloud.com/user-291029717/fomc-on-hold-boe-go-next-us-gdp-tonight-corona-virus-spreads?in=user-291029717/sets/the-morning-call

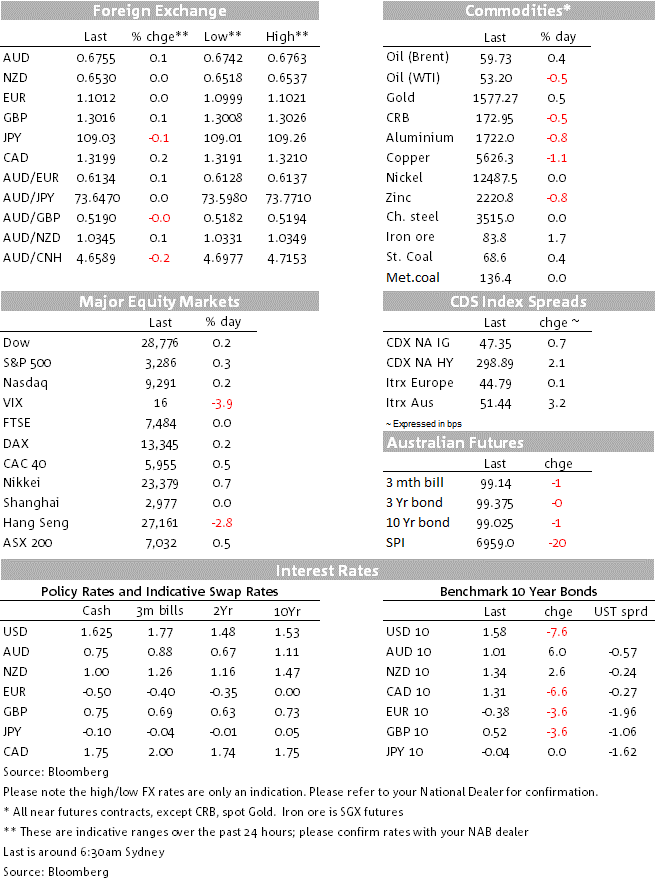

Wednesday FOMC meeting was meant to be a non-event. In the end it wasn’t. Instead Chair Powell turned the music up in the press conference with dovish words on inflation, stating the “Fed is not satisfied with inflation running below 2% and it is not a ceiling”. Markets interpreted that as the Fed envisaging cutting rates in the future on the inflation outlook alone instead of the flat to higher rates outlook implied at the December FOMC meeting. Markets now price 1.6 rate cuts from the Fed by the end of 2020 compared to 1.2 cuts yesterday. A Fed lower for longer has seen bonds extended their rally with US 10yr yields ‑7.6bps to 1.58%, while the USD (DXY) reversed gains to finish broadly unchanged at 98.025. Equities unsurprisingly are higher with the S&P500 +0.3%, helped along by solid earnings and no worsening in the fears over the Wuhan Coronavirus despite a rising death toll. The oil market though remains concerned on the outbreak with a number of airlines cancelling or reducing flights to China and OPEC has flagged the possibility of extending or deepening production cuts. As we open, the AUD is trading at 0.6755 having reversed some of its CPI inspired gains yesterday. Rates markets though continue to pare pricing for an RBA February rate cut, now just 10% priced, with a number of media commenters with known links to Martin Place downplaying the prospect of a February rate cut and implying the next meeting for a cut may not be until April.

The Q&A again dominated after an FOMC statement that had minimal changes. The most significant comment was Powell’s remarks around inflation: “Fed is not satisfied with inflation running below 2% and it is not a ceiling”. On the more optimistic side, Powell said there are grounds for “cautious optimism”, noting supporting financial conditions, easing trade tensions and lower odds of a hard Brexit. The coronavirus was likely to cause disruption, but it is uncertain what the macroeconomic impact will be – note SARS had little impact on the US. The Fed also made some minor implementation changes, hiking IOER by 5bps given the Effective Fed Funds rate at 1.55% is at the bottom end of the 1.50-1.75% target, while extending repo operations at least through to April.

Data was on the soft side with the US Goods Deficit and Inventories meaning downside risks to Q4 GDP out tonight. The consensus for GDP currently stands at 2.1% and various GDP Nows suggest a lower print at around 1.7% following the data. As for the data itself, the Goods Deficit rose to $68.3bn, above the $65bn consensus. Almost all the increase was due to a 2.9% rise in imports, driven by industrial imports. While the trade balance is likely to make a large contribution to Q4 GDP as a whole, it will be offset by inventories with Wholesale Inventories down and Retail Inventories flat. Importantly for the outlook, Q1 GDP could be soft as well as imports recover from the tariff uncertainty and as Boeing weighs on Industrial Production and the manufacturing sector more broadly. Second-tier Pending Home Sales also disappointed, falling a sharp 4.9% in the month, but is very hard to explain and probably more reflects difficulty seasonally adjusting data at the end of the year. Housing construction is one area of strength in the economy and is expected to add to growth.

The AUD reversed yesterday’s CPI inspired gains with the USD having strengthened initially before the FOMC and as coronavirus fears weigh on the oil market. As we open the AUD is trading at 0.6754. As for yesterday’s CPI figures, headline inflation was a tenth higher than expected at 1.8% y/y, though the core trimmed mean measure was broadly in-line and also matched what the RBA had projected back in November. Markets have further reduced pricing for a Feb rate cut to just 10% with a rate cut not fully priced until July 2020. RBA commentators with known links to Martin Place also downplay the prospects of a February cut and also state the outlook for cuts will be tied to consumer spending with December quarter consumption figures held out to be key. It is important to note here the RBA doesn’t get December quarter consumption figures until before the April Board Meeting.

Equities rose with the S&P500 +0.3%. Apple beat earnings expectations after the close yesterday amid an increase in iPhone sales, while GE was boosted by the progress the company was making in its recovery and cost-cutting plans. As for the earnings season, around 28% of the S&P500 have now reported earnings, with 70% beating analyst expectations so far. Note Facebook, Microsoft and Tesla all report after the market close later this morning, while Amazon reports tomorrow.

Coronavirus fears in markets are no worse despite the number of cases and deaths rising. As of yesterday there were 6,065 cases and 132 deaths, importantly for markets 98% of cases are still in China, while the mortality rate of the virus is significantly lower at around 2% compared to SARS at 9.6%. The virus is likely to impact Chinese growth with the Chinse Academy of Science suggests GDP growth could fall from 6% y/y to below 5% in Q1. In terms of quarterly growth profile that would imply GDP growth slowing to 0.3% q/q in Q1, from 1.5% and is broadly in line with the rules of thumb associated with SARS (SARS was estimated to have dragged 0.5-1.1%points off growth in 2002-03). The impact on economies outside of China is likely to be more felt in the tourism/travel sector, with the oil market very sensitive. Algeria noted OPEC may take action with the March meeting maybe moving to Feb in order to study steps to ensure the oil-market is balanced a coronavirus spends (currently may extend cuts until June from the original March deadline, but also may signal even greater cuts).

It is very quiet domestically with no date of note scheduled. Datawise all focus will be on the Bank of England meeting with markets pricing a 50% chance of a cut, though economists are less convinced with only 30% tipping a cut. The German advanced CPI for Jan is also out, though is unlikely to move markets. Focus then shifts to the US with Q4 GDP where downside risks might be evident given various GDPNows under-club the 2.1% consensuses. In markets, focus will remain on the Wuhan Coronavirus as well as earnings reports with Amazon being the latest FAANG to report:

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.