FOMC Minutes re-iterative ‘patience’, many see inflation fall as ‘transitory’

US equities and bond yields lower on intensifying trade frictions, inventory-led oil price slide

GBP still on the skids with near-zero chance of WAB being approved in June, PM May’s days seen numbered

‘Flash’ Eurozone PMIs this evening the main economic draw

The FOMC minutes have come and gone in the last couple of hours to little fanfare. Key quotes are that “Members observed that a patient approach to determining future adjustments to the target range for the federal funds rate would likely remain appropriate for some time,” and that “many participants” viewed the recent easing in inflation “as likely to be transitory, and participants generally anticipated that a patient approach to policy adjustments was likely to be consistent with sustained expansion of economic activity, strong labor market conditions, and inflation near the committee’s symmetric 2% objective.” Worth noting that the Minutes (from May1st) pre-date the initial ramp up in trade tensions (i.e. Trump lifting of the tariff rate on $200bn worth of Chinese imports to 25%) so the narrative vis-a-vis the balance of risks to the economic outlook could change come the next (June 18/19th) meeting.

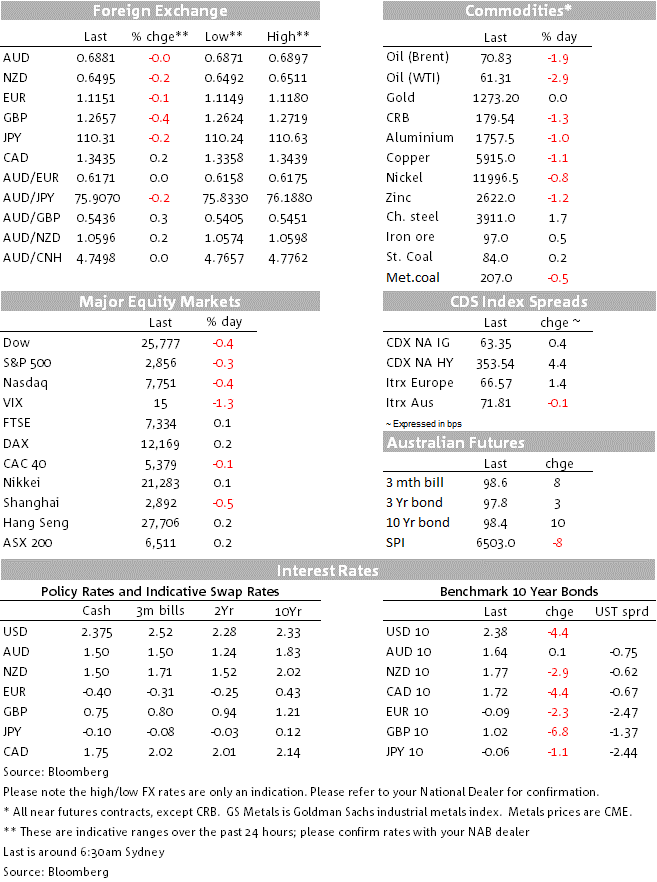

Most of the overnight action in equities and bonds occurred prior to the Minutes and didn’t change much thereafter. The main drivers, depressing both equity prices and bond yields, have been sharply lower oil prices – more below – and the further intensification of what is being dubbed in some quarters as the start of a technology cold war. This on yesterday’s news, courtesy of Bloomberg, that the “U.S. is considering cutting off the flow of vital American technology to as many as five Chinese companies including Hangzhou Hikvision Digital Technology Co., widening the dragnet beyond Huawei to include world leaders in video surveillance”.

Unrelated, Qualcomm has been the big loser in the IT sector, off 10.9% and enough to weigh on broader indices. This after the judge in the Federal Trade Commission anti-trust case against Qualcomm ruled against the company on “virtually every” measure. Also depressing the indices was a sell-off in consumer discretionary stocks – down 0.9% within the S&P500 – after Lowe’s and Nordstromm both reported weaker than expected earnings and cut future profits forecasts. US mainboard stock indices closed down between 0.3 and 0.5%

Oil has been hit hard on latest EIA inventory stats. showing a 4.74 mln. barrels rise in crude inventories last week against expectations for a 1.7mln barrels draw. Gasoline inventories were also sharply higher, +3.72mn barrels against an expected 850,000 barrels draw. WTI futures ended 2.7% lower at $61.42 a barrel on the NYME and Brent crude 1.6% lower at $70.99 a barrel on ICE.

US Bond yields appear to have fallen on a combination of equity market weakness as well as a fall in the break-even (inflation expectations) component of nominal yields. Nominal 10 year yields are 4.4bps lower to 2.382% within which break-evens are down 4bps to 1.80%.

In currencies, both AUD and NZD have been largely sidelined overnight, AUD/USD unchanged on Tuesday’s NY closing level at 0.6882 and NZD 0.2% lower at 0.6495 but unchanged on where we left it on Wednesday. Yesterday’s slippage came in conjunction with some further step up in pricing for another RBNZ rate cut in August, to 60% from about 50% earlier in the week. There has been no noticeable response to what out BNZ colleagues describe as a ‘slightly disappointing’ Fonterra forecast for the 2019-20 milk price payout of NZ$6.25-7.25 per kilo, a view seemingly predicated on anticipation of some further reduction in global dairy prices.

Far and away the biggest mover has been GBP, down another 0.4% to $1.2662 and lowest since 4th January (AUD/GBP up to 0.5435). Speculation Theresa May will be forced to step down as prime minister before she gets the chance to present her withdrawal agreement bill for the fourth time is intensifying. The 1922 committee of Conservative backbenchers is meeting on Friday and will reportedly discuss changes to its rules to allow an early leadership contest, if May does not resign first (under the current rules, May cannot face a leadership contest until December). Meanwhile, Brexit supporter Andrea Leadsom just announced her resignation from May’s cabinet and British media report other cabinet members as saying May needs to stand down. The threat of a Brexiteer future prime minister, such as Boris Johnson, continues to weigh on Sterling.

In index terms, the USD is very marginally firmer (DXY +0.04 at 98.1) with offsetting influences from a weaker GBP and CAD but stronger CHF, JPY and SEK.

Coming up

On the domestic calendar, only CBA’s PMI series and Japan’s Nikkei manufacturing PMI

Offshore this evening, its ‘flash’ French, German and Eurozone PMI data , with expectations for the numerous series narrowly mixed around April final levels. E.g. for the pan-Eurozone numbers, manufacturing is seen at 48.1 from 47.9 and services 53.0 from 52.8.

We also get the German May IFO survey, final German Q1 GDP numbers (with detailed breakdown) and the Minutes of the ECB’s April meeting

The US has the little-noticed Markit PMIs, New Home Sales and the Kansas City Fed manufacturing activity index.

Creating cost-effective choices for consumers while forging business success is nothing new for Chemist Warehouse co-founder Jack Gance. As special guest at a recent NAB Transaction Banking event series, he looks at a new way to pay for businesses and customers.