Online retail sales growth slowed in May following a fairly strong April

Insight

The US President hinted that a resumption of trade talks with China wasn’t a done deal, adding uncertainty in an already shaky market.

https://soundcloud.com/user-291029717/nab-revises-forecasts-as-trade-tensions-rise-pound-pummelled-salvini-fires-election-salvo?in=user-291029717/sets/the-morning-call

I don’t care, oh I don’t care, Oh no I don’t care – Cheryl Cole

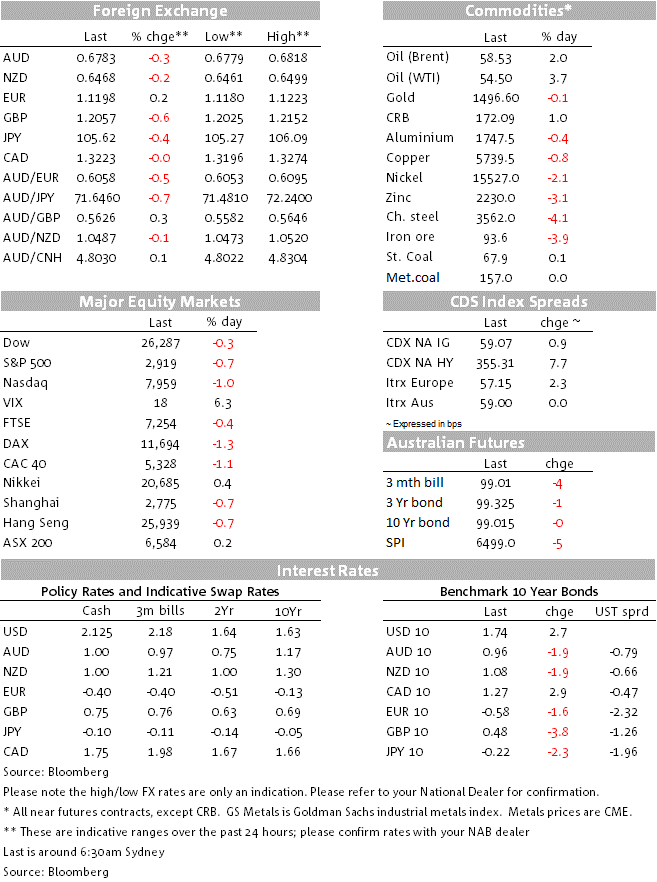

After trading higher for three consecutive days, US equities ended last week on a sour note following comments from President Trump suggesting he didn’t really care if China trade talks took place in September, further reinforcing the growing view that both economic powers are gearing up for a protracted trade war. In spite of the negative trade news, UST yields, edged a little bit higher on Friday and the USD was little changed. AUD and NZD weakened a little on Friday night, but GBP was the biggest loser after data showed the economy contracted in Q2. Meanwhile in the commodity complex, iron ore prices declined again, gold closed just below the $1500 mark and oil prices continued to recover notwithstanding another IEA downgrade to global oil-demand.

After a shaky start to the Friday’s overnight session, US equities embarked on a decent recovery and at one stage it looked like all three main equity indices could end the week recording a fourth consecutive days of gain. These expectations banished in the last hour of trading following comments from President Trump giving the impression that he was not bothered whether or not US-China trade talks would take place in September. He said “We’ll see whether or not we keep our meeting September…if we do, that’s fine. If we don’t, that’s fine”. There was also some market confusion after Trump said “we’re not doing business with Huawei”, but the White House later clarified that he was only referring to the ban on Federal Departments buying from Huawei. Earlier during our Friday morning, Bloomberg reported that the White House was holding off on a decision about licences for US companies to restart business with Huawei after Beijing said it was halting purchases on US farming goods.

After the market close, and playing good cop for change, White House trade advisor Navarro, a known China Hawk, said he was still expecting a new round of talks with China to go ahead as planned in September. However he also expressed discontent with China’s strategy to devalue its currency, adding that structural changes from China, such as an end to massive subsidies to state own companies, forced technology transfer in exchange for access to the Chinese market, cyber intrusion and Fentanyl trade ( that is killing 100 Americans a day), were all needed in order to get a deal over the line.

The Dow Jones ended Friday down 0.34%, the S&P 500 dropped 0.66% while the tech-heavy Nasdaq Composite fell 1%. All three major indices posted losses for the week, with the S&P 500 down 0.5%. Meanwhile on the other side of the Atlantic, major European indices also closed in negative territory with the STX Europe 600 index closing the day -0.84% and down -1.74% for the week.

The USD was little changed in index terms with DXY closing the week at 97.49 , but GBP on the other hand was the big mover, losing 0.82% against the USD to 1.2033 following an unexpected contraction in the UK’s Q2 GDP print. UK GDP was soft at -0.2% q/q (zero consensus) and to 1.2% y/y. That’s the first quarterly decline since 2012. A weak outturn was generally expected due to prior stock-piling ahead of the 29 March original Brexit date. That boosted Q1 GDP to +0.5% and some payback was anticipated. Inventories in Q2 subtracted 2.15 pct pts from GDP, business investment remains soft at -0.5%, but private consumption was reasonable at +0.5% and government spending was strong at +0.7%. Looking forward the weaker economic momentum seen in activity indexes may be partially offset by more stock-building ahead of 31 October and by a rebound in auto production as the August annual shutdown was moved to March this year.

CAD was the other big mover during Friday’s overnight session, but in the end the Lonnie closed the day little changed at 1.3222. Weaker Canadian employment sent the unemployment rate higher to 5.7%, against expectations but market reaction was muted to the extent that annual wage inflation rose to a decade-high rate of 4.5% y/y. Oil was another factor at play with prices continuing their rebound ( WTI +3.7% to $54.5 and Brent $58.53 +2%) following last week’s comments from Saudi Arabia to engage with OPEC+ friends in order to reduce output. Gain in oil prices came about in spite of the fact the International Energy Agency downgraded its forecast for global oil-demand growth for the third time in four months, lowering it to 1.1 million barrels a day from 1.2 million barrels a day.

AUD and NZD ended the week about 0.20% lower at 0.6786 and 0.6468 respectively. The NZD met some resistance just under the 0.65 mark, before trending lower through the US trading session to close the week near the middle of the wider-than-usual 2-cents range for the week. After trading sideways during our session on Friday, the AUD also drifted lower later in the US session, reflecting a souring in market sentiment following President Trump comments. After highlighting downside risks to our AUD and NZD forecasts at the beginning of last week given the escalation in trade tension between the US and China, on Friday we officially downgraded our FX forecasts reflecting our new assumption that nothing materially positive in terms of US-China trade negotiations will happen at least through the remainder of 2019 and early 2020.

Global growth is likely to endure a challenging environment over coming quarters and our expectation is that the PBoC will allow the yuan to continue to depreciate, taking USD/CNY to 7.40. This combination is not a good recipe for commodities and growth sensitive currencies such as the AUD and NZD, as a result we have slashed our end of the year targets for AUD to 0.65 and NZD to 0.62.

US 10-year rates ended the week nudging higher, up 3bps to 1.74%. This capped off a volatile week, which saw it trade a wide 26bps range. Italy’s bond market extended losses after the government’s call for a new election after it lost its majority. Italy’s 10-year rate rose to 1.80%, taking its gain for the last two trading sessions to about 40bps. Currency markets don’t seem bothered by yet another election, with EUR nudging back up to 1.12.

Looking at commodities in more detail, copper prices eased 0.8% on Friday while iron ore fell another 3.9% to $93.6. Gold, was a tad softer, closing just under $1500, probably reflecting some profit taking, after a decent run of late.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.