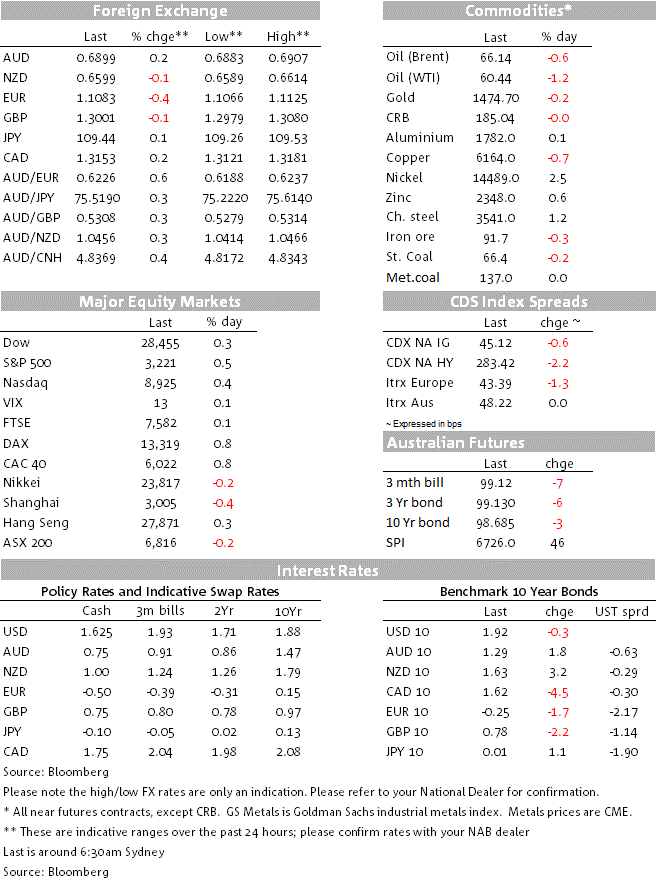

US equities gapped higher at Friday’s open and held their gains though the session, S&P finishing +0.5% and NASDAQ +0.4%. YTD gain for S&P now stands at 28.5%. Strong performance by Joe Biden in Thursday’s night Democratic Presidential contender debate and polls showing him ahead of left-leaning Warren and Sanders in the nomination race, cited in some dispatches for gains.

US bond markets showed little net change across the curve, 2s +0.1bp, 5s unchanged, 10s -0.3bp and the 30-year -1bp. On the week, 2s are 2.3bp higher and 10s +9.5bps.

It was a good night for the USD Friday, DXY adding 0.3% to 97.69 do now very comfortably back in the ~96.5 – 99.5 range that has prevailed since August. EUR (-0.38%) and CHF (-0.44%) losses drove USD gains, with AUD/USD the best performing G10 pair, +0.2% to close exactly at 0.6900. Very positive risk sentiment and the erosion of February 2020 RBA rate cut expectations (now 37%) have been supporting AUD since last Thursday’s better than expected local employment report, prior to which a February rate cut was priced at nearer to 60%.

CAD was weaker Friday (-0.27%) after October retail sales printed -1.2% against +0.5% expected, though spent much of the rest of Friday clawing back knee jerk losses amid suggestions the weak October may have reflected delayed sales in front of Black Friday/Cyber Monday which the statisticians are as yet struggling to adequately seasonally adjust for.

Trump said he had very good talk with Xi about the trade deal, though Xi reportedly said that he was unhappy with US criticizing China human rights record on HK and US supporting Taiwan.

Plenty of US data Friday, the highlight being November Personal Income, Spending and PCE deflator data. The Fed’s preferred core PCE deflator was 0.1% as expected, putting yr/yr at 1.6% up from 1.5%, also as expected. Personal Income rose by 0.5% above the 0.3% expected and Personal Sending 0.3% against 0.2% expected.

Q3 US GDP unrevised at 2.1%.

Philly Fed Business Outlook 0.3% down from 10.4 and 8.0 expected.

Weekly jobless claims 234k from 252k prior week but above the 225k expected.

Q3 US Current account -$124.1bn little changed on Q2’s revised -$125.2bn.

Nov Existing Home Sales -1.7% after +1.5% in October (revised from 1.9%) beneath the -0.4% expected.

UoM final Dec Consumer Sentiment 99.3 from 99.2 preliminary and expected

Atlanta’s Fed’s Q4 GDP Now estimate revised to 2.1% from 2.3%

UK final Q3 GDP revised up to 0.4% from 0.3% (yr/yr 1.1% from 1.0% preliminary)

UK final manufacturing PMI 47.6 vs. 47.4 ‘flash’.

Friday’s CFTC/IMM data shows the overall net USD speculative long (G10+MXN) reduced to just 16k contracts from 66k the week before. The big changes were in NZD, where the prior net short of 25k was reduced to just -8k; GBP where the net short of 23k reduced to -6k (so picking up the pre-UK general election rally) and additions to MXN longs, to 152k from 131k

Coming up

Australia November Private Sector credit at 11:30 AEDT (expected 0.2% for 2.4% yr/yr down from 2.5% in October).

US November Durable Goods Orders (expected +1.5%, while core ‘non-defence ex-aircraft’ orders seen +0.2%); US November new Home sales, expected -0.4%.