A private sector improvement to support growth

Insight

Trump’s executive orders hit technology stocks in the US and China on Friday.

“Do you really like it?; Is it, is it wicked?; We’re lovin’ it; Lovin’ it, lovin’ it; We’re lovin’ it like that”, DJ Pied Piper and the Master of Ceremonies 2001.

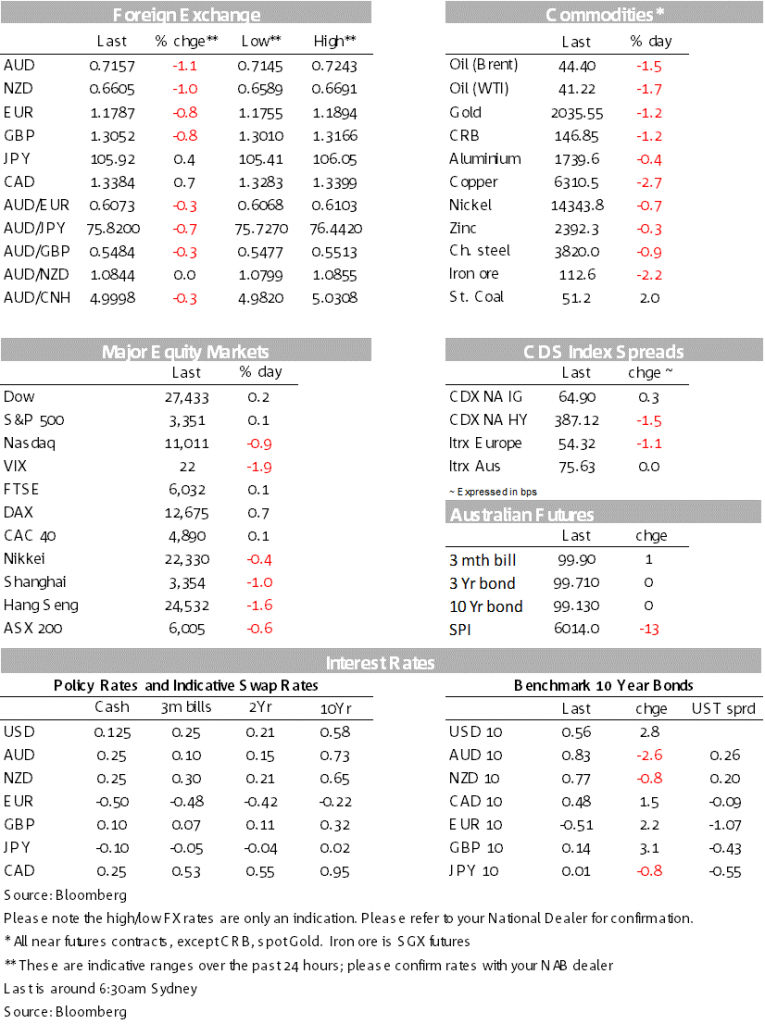

“Do you really like it” was a 2001 one hit wonder from DJ Pied Piper and the Master of Ceremonies. Some will be wondering the same thing from President Trump after his executive actions on WeChat and TikTok (45 day notice of a ban) drove a cautious mood in markets, reinforced by the largely symbolic sanctioning of 11 Chinese/HK officials, incl. HK Chief Executive Carrie Lam. Tech stocks were hit on both sides of the pacific and the NASDAQ ended in the red at -0.9%. Those actions come ahead of scheduled US-China talks on August 15 where the consensus to date in markets is that President Trump wants the phase 1 deal to continue (as much as China) given the need for votes in the mid-West come November.

A better-than-expected payrolls report (1.8m v 1.5m expected) though did help stabilise sentiment during the US session with the S&P500 closing slightly in the green at +0.1%. The USD (DXY) rose 0.7%, initially driven by cautiousness and then supported by the strong payrolls print and likely short covering given market positioning. Safe havens outperformed with USD/Yen +0.4% and USD/CHF +0.2%. Losses were led by the AUD (-1.1%), NZD (-1.0%) and NOK (USD/NOK +0.9%). Yields rose with US 10yr +2.8bps to 0.58%, most of the moves occurred well after payrolls and likely reflects positioning with a record $112bn of US Treasuries to be auctioned. As we open markets will be scrutinising President Trump’s latest executive actions to bypass Congress on a fiscal package (announced on Saturday), which fall well short of what Democrats were proposing (more on that below).

First to US Payrolls which were much stronger than expected and helped to stabilise sentiment. Headline payrolls in July rose 1.76m v the 1.5m expected, while unemployment fell to 10.2% from 11.1% and was also well below the 10.6% expected. Underneath the hood the beat was helped by a 0.3m rise in government employment with educators returning to work, while overall gains were driven by leisure and hospitality workers +0.6m. Weak aspects of the report included little bounce in goods-sector employment (just +0.039m), while the participation rate actually fell to 61.4% from 61.5% where a rise to 61.8% was expected. The data though is seen as dated given the deterioration seen in the high-frequency data to date.

The mood in markets was overwhelmingly cautious after President Trump’s actions on WeChat and TikTok. Late Thursday President Trump signed two executive orders that would ban WeChat and TikTok in the US in 45 day’s time. The unexpected part of the order was that it signalled out WeChat and its owner the Chinese tech giant Tencent with potentially profound implications for Apple given WeChat’s extensive use in China as a electronic communication and payments platform (Apple closed down -2.5%). Tencent also has a big presence in the US through its gaming operations.

The US administration also announced sanctions on 11 senior Chinese and HK officials including HK Chief Executive Carrie Lam. Rounding out the actions, US regulators recommended that overseas firms lifted in US exchanges must be subject to US public audit reviews from 2022. The bigger question for markets is whether these actions jeopardise the US-China trade talks on August 15 and markets will be looking closely for any Chinese retaliation. The running assumption in markets has been President Trump needed the phase one deal to succeed (as much as China) this side of the November elections to secure the mid-West. At the same time President Trump is running a hard China line into the elections.

Chinese trade data shot the lots out, but took a backseat given the actions on WeChat and TikTok. For the record exports soared, +7.2% v -0.6% expected and vindicating the view that global restocking is happening given the run down in inventories as seen in global business surveys amid a sharp recovery in new orders.

The RBA SoMP also took a backseat on Friday

Though did contribute marginally to the softer AUD. The AUD’s (-1.1%) similar performance to the NZD (-1.0%) though suggests it as not an dominate force on the Aussie. The SoMP overall was was on the dovish side with forecasts for inflation and wages downgraded by around 0.25ppt across the forecast horizon. Trimmed-mean inflation is now expected to be just 1.25% in 2021 and 1.5% by the end of 2022. Unemployment forecasts have also been revised higher by up to 1ppt with unemployment now peaking at 10% and remaining elevated at 7% by the end of 2022. Given the forecast trajectory, markets may ask what else the RBA can do. The SoMP reinforced the RBA’s red lines on the use of certain tools: “not a case for intervention in the FX market”; negative rates are “extraordinary unlikely”; and monetary financing of budget deficits “not an option”. The RBA has not ruled out adjusting the existing package of measures if needed, which puts the emphasis on tweaks including lowering the cash rate (to 10bps from 25bps), extending and lowering yield curve targets further out the curve, outright QE, and/or tweaking the Term Funding Facility.

Trump actions to bypass Congress will likely dominate today’s session, particularly the legality and whether this prompts Congress and the Administration to agree to a broader package. On Saturday Trump announced an executive order and three executive memorandums to extend some stimulus measures given talks between Democrats and the Administration had made little progress. The headlines are that the unemployment benefit supplement will be extended but lowered to a minimum $300 a week, with an extra $100 a week should states be willing to fund it (so $400 a week, down from $600 a week). It’s unclear whether all states would be able to fund their portion. While President Trump does not have the power of the purse, he has precedent in transferring already approved amounts around in an emergency with the funding of $44bn coming from the $70bn Disaster Relief Fund. The extra weekly benefits would be available until Dec. 6, about a month after the Nov. 3 general election, or until the disaster fund’s balance drops to $25 billion. Other measures include deferral of Federally held student loans through to December 31 with interest waived (43m borrowers with student loans). Eviction moratoriums are also being explored for properties with government-backed mortgages (affects around one-third of renters).

A busy week domestically where focus will remain on Victorian virus counts which should start to be flatten out given Melbourne’s level 4 lockdown has been in place for a week (since 2 August, note mean incubation for the virus is thought to be 5-14 days). Datawise we get Payrolls on Tuesday for the week ended 25 July with job losses likely to show from Melbourne’s earlier level 3 lockdown. The NAB Business Survey will be viewed in this light. Employment on Thursday should be interesting with market expectations ranging from a wide -120k to +150k! – the debate being whether the survey reference week (interview typically on the Sunday between the 5th and 11th of each month) was too early to pick up the slowing in the labour market seen in payrolls and the smaller household COVID-19 survey.

RBA Governor Lowe is speaking in parliamentary testimony on Friday where his views on the economy and what else the RBA could do given their subdued baseline forecasts will be closely watched (the Governor has already laid out his red lines on the use of certain tools: “not a case for intervention in the FX market”; negative rates are “extraordinary unlikely”; and monetary financing of budget deficits “not an option”). Finally the WPI is on Wednesday with also a wide consensus of -0.3 to +0.5% q/q – either way the data is likely to be dated given the RBA notes in its liaison program that around 35% of businesses are expecting to implement wage freezes in the year ahead.

Though its likely politics will again dominate over data for markets. Democratic Presidential hopeful Biden is set to announce his running mate this week which could prove to be important to the odds markets are ascribing to a Democratic clean sweep come November (Presidency, Senate and House; PredictIt is back to 52% from a high of 58% in August – see link). President Trump’s recent actions on Chinese officials and companies will also be closely watched, especially for Chinese retaliation given US-China trade discussions are scheduled for August 15. Discussions over a fiscal package will also likely to continue despite President Trump’s executive actions.

It is an important week for China with aggregate financing figures due anytime, CPI/PPI out today and monthly activity indicators on Friday – retail sales again the one to watch. The European summer holiday season will see a quiet week with no top-tier data apart from the UK which has Q2 GDP on Wednesday. It is also fairly quiet in the US with just CPI on Wednesday and retail sales on Friday. Closer to home across the ditch the RBNZ meet with the consensus for no change to either rates or the QE bond buying program limit. Our BNZ colleagues suggest the RBNZ is likely to defer decisions on the QE program to later in the year.

A quiet day domestically with no top-tier data scheduled. Across the ditch NZ has a prelim read on the ANZ Business Survey and China has CPI and PPI data. The US and Europe also has little in the way of data, though focus will be squarely on President Trump’s authority to extend the unemployment benefit supplement.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

A private sector improvement to support growth

Insight

Online retail sales growth accelerated 1.1% in April

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.