Online retail sales growth slowed in May following a fairly strong April

Insight

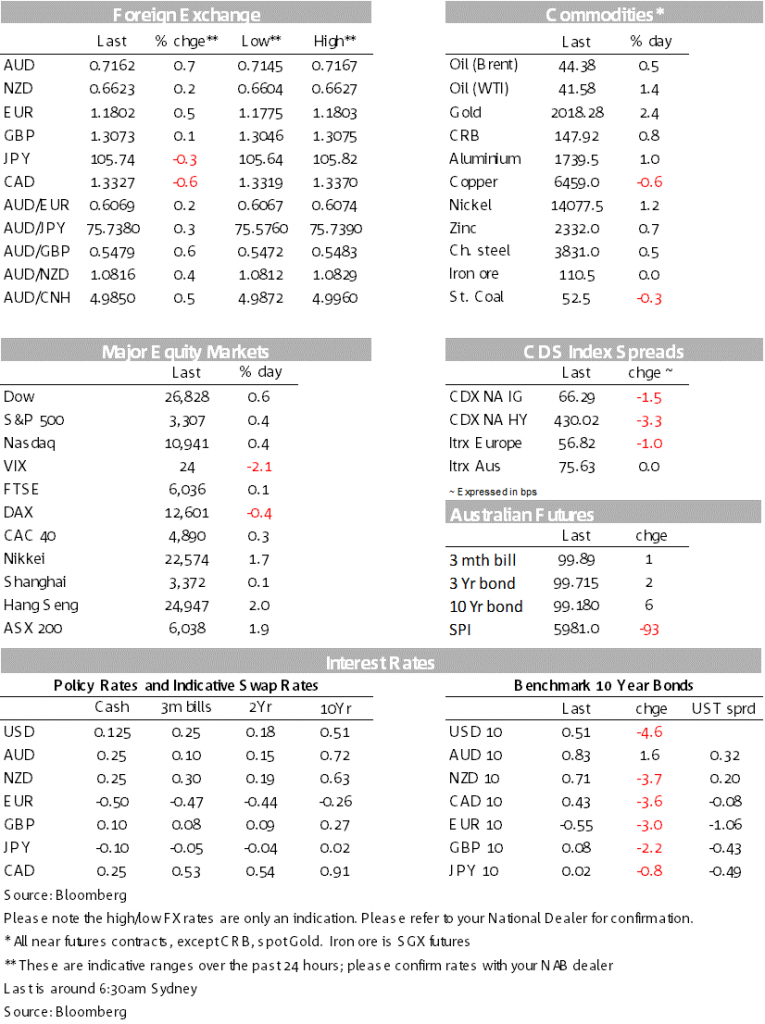

Treasury bond yields are reaching new lows which has heightened the appetite for gold.

“More than words is all I ever needed you to show; Then you wouldn’t have to say that you love me; ‘Cause I’d already know”, Extreme 1990

“More than words” was an acoustic funk metal hit of the early 1990s and is now a well-worn love ballad. So it was overnight with markets still sniffing a US fiscal deal given the election proximity despite little progress having been made. Equities rose with the S&P500 +0.4%. In contrast bonds rallied with US 10yr yields -4.6bps to 0.51%, while gold closed above $2,000, currently +2.4% to $2,018. The USD fell with DXY -0.3% with EUR +0.5% and USD/Yen -0.3%. The AUD was the outperformer +0.7% to 0.7162, partly driven by yesterday’s RBA meeting where policy guidance was unchanged amidst some speculation that the Bank was contemplating further easing given the Victorian lockdowns. Looking ahead it’s a quiet day domestically with only lending finance, but offshore NZ has their labour market report, the final services PMIs are out and the US has ADP Payrolls and the Services PMI. Good luck.

Despite continuing negotiations, talks so far have yet to yield much in the way of progress. The White House chief of staff Meadows said “we’re a long ways away from striking any king of a deal”, Democratic House leader Pelosi said she was not budging from the $3.4 trillion package first proposed by Democrats (“at some point you just have to freeze the design”).

Nevertheless, markets still sniff a deal given the proximity of the election. Bolstering those hopes were comments by Republican Senate leader McConnell who said “Wherever this thing settles between the president of the United States and his team, who has to sign it into law, and the Democrat, not insignificant minority in the Senate and majority in the House, is something I’m prepared to support…Even if I have some problems with certain parts of it.”.

The key issue in the talks is the $600 per week unemployment supplement with around 27m Americans receiving the payment according to Labor Department data (the last payment was $16.4bn for the week ended 25 July). Note both sides have agreed to another round of one-off cheques worth $1,200 to certain households. Failure to agree to another round of stimulus would hit the US economy hard at a time when high-frequency data suggests it is losing some momentum.

High frequency card data by JP Morgan suggests the consumer spending recovery has stalled with spending still down 10% on last year, while a recent survey by Cornell finds there has been a second round of layoffs with around 31% of those initially re-hired have been laid off a second time (see Cornell for details). Note the survey was from 23 July to 1 August so pre-dates this Friday’s Payrolls report.

Global bonds continued to rally overnight with the US 10yr yield falling -4.6bps to 0.51%. While there was no catalyst for the move, speculation is mounting what the Fed may announce regarding forward guidance come September – especially in regards to the inflation target and yield curve control. The Fed’s Daly sad the Fed was “thinking about how we can use forward guidance to telegraph to people…what our intentions are in terms of supporting the economy going forward.” Daly also noted the Fed is willing to run the economy hot “we have room to let the economy go well beyond what people think is its maximum level of employment”. The Fed’s Evans yesterday also played more explicitly into that view saying the Fed will not be worried about inflation unless it gets beyond 2.5%.

It was a tale of two halves with the USD initially climbing before reversing to end down -0.3%. Uncertainty over US fiscal talks appeared to weigh as well as commentary around the Fed’s forward guidance come September. The major driver of USD weakness continues to be the Euro with EUR +0.5% to 1.1802, while the Yen rallied with USD/Yen -0.3% to 105.74. An explosion in Beirut that is estimated to have killed 50 people has had little impact on the majors so far. The AUD was the best performer in the G10 +0.7% to 0.7162 helped by the RBA (see below). Across the Ditch the NZD underperformed +0.2% with AUD/NZD lifting 0.5% to 1.0820, a two month high despite the harsher lockdown in Melbourne. Australia’s greater exposure to China’s industrial recovery a likely factor (see below). Separately, whole milk prices fell 7.5% at the fortnightly GlobalDairyTrade auction overnight while the broader price index declined 5%. The fall in prices at this auction reverses around half the gains from the trough in May.

Yesterday’s RBA meeting was broadly supportive for the AUD. The RBA kept policy unchanged and while widely expected, there were some out there speculating the RBA may flag further easing given the stage four lockdown in Melbourne. The RBA instead kept policy and guidance unchanged, concluding: “the downturn is not as severe as earlier expected and a recovery is now underway in most of Australia. This recovery is, however, likely to be both uneven and bumpy, with the coronavirus outbreak in Victoria having a major effect on the Victorian economy”. The RBA’s latest forecasts (to be released in detail in Friday’s SoMP) were also largely unchanged from May. The RBA though did reinforce its commitment to the 3 year yield curve control target of 0.25% and flagged it would resume buying today to keep the yield consistent with the target – the comment in reaction to the 3 year yield being a little higher than 0.25% over recent weeks (recent high of 0.287%).

Other Australian data yesterday included Real Retail Sales and the Trade Balance which were on the softer side. Real retail sales fell 3.4% in the June quarter, a little weaker than the 3.0% expected by markets, with retail sales set to detract 0.6 percentage points from Q2 GDP. The trade balance for June was also slightly weaker than expected, but is still expected to add around 1¼ percentage points to Q2 GDP growth. The notable trend in the data was a surge in exports to China with almost 47% of all merchandise exports going to China. The rise comes despite elevated political tensions.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.