Online retail sales growth slowed in May following a fairly strong April

Insight

The AUD held its position after the better-than-expected Australian Labour numbers yesterday.

https://soundcloud.com/user-291029717/good-aussie-jobs-numbers-add-to-a-positive-vibe?in=user-291029717/sets/the-morning-call

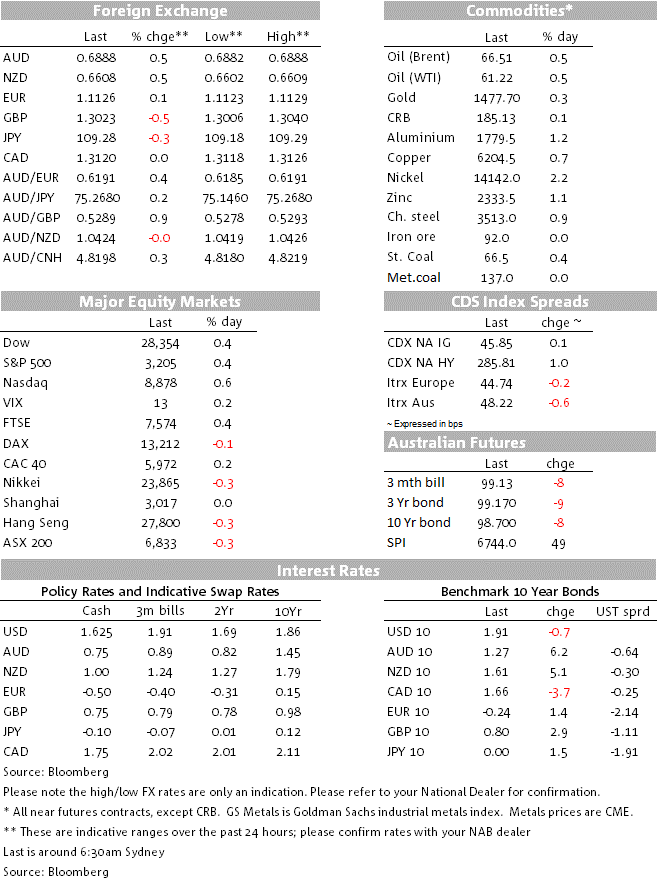

A flurry of central bank activity could not derail the quiet lead into Christmas that we have seen over the past week. There is also little new news globally with the biggest headline this morning being the Riksbank’s as expected decision to lift rates out of negative. In G10 FX GBP continues to come under pressure, down -0.4% to 1.3023 and is now 1% below pre-election levels as hard Brexit fears surface. The USD (DXY) is little changed with only small moves in EUR (+0.1% to 1.1124) and a moderate one in USD/JPY (-0.3% to 109.28). The top performing currencies are the NOK and AUD, the AUD on the back of yesterday’s stellar jobs numbers with the Aussie now up 0.5% over the past 24 hours to 0.6888. Global yields were little moved, with US 10yr yields -0.9bps to 1.91% and German 10yrs +1.4bps to -0.24%. Stocks continue to hit record highs with the S&P500 +0.4% to 3,205.

2019 was no doubt the story of central banks cutting rates to ward off risks and lift inflation. The exception to that game in G10 were the Nordics (Riksbank and Norgesbank) and the Bank of Canada. Overnight the Riksbank played further to that view, hiking rates to 0% (as expected) and ending the five year experiment with negative rates. While it is tempting to take this as a pointer for central banks in 2020, it is worth noting that the Riksbank’s forecast for the policy rate is to be on hold through 2020 and 2021, while unemployment is forecast to edge higher throughout the forecast horizon. Indeed the press conference emphasised that part of the reason for the hike was that there were risks to keeping negative rates for a long period. The Norgesbank also met overnight, keeping rates unchanged at 1.50%. There was some perception of a hawkish bias with the projected policy rate path lying between 1.50-1.60% and thus implying a 40% chance of a hike next year. Although the Norgesbank also makes it clear that “since the rate path is closer to 1.50% than 1.75%, the path can be interpreted to mean that there is a greater probability of the policy rate path remaining at 1.50% than being raised to 1.75% in the coming period”. NOK was smartly higher on the mild hawkish interpretation with EUR/NOK -0.4% to 9.9763.

The BoE kept its cash rate unchanged at 0.75% in a 7-2 decision with Haskel and Saunders dissenting again in favour of a cut. The Minutes to the meeting noted the Bank was prepared to cut rates if global growth didn’t stabilise or Brexit uncertainty remained. Alternatively if risks did not materialise “some modest tightening of policy” may be needed. The market currently prices around a two-thirds chance of a rate cut next year. The next BoE governor is likely to be announced on tonight according to the FT with Andrew Bailey reported to be the clear favourite.

GBP initially rose, then fell away post the BoE meeting to be -0.4% to 1.3012. There was no single catalyst, though the Queens Speech emphasised that PM Johnson was again ruling out any extension to the implementation period: “we will avoid the trap of further dither and delay – by ruling out any extension to the implementation period beyond 2020”.

Was on the weaker side of expectations with the Philly Fed Manufacturing Index at 0.3 against +8 expected, while Jobless Claims were 234k against 225k expected. The details of the Philly Fed were more positive though with increases in new orders, though jobless claims is worth watching in coming weeks given the recent uptick. Treasury yields did dip lower on the news, though on net US 10yr yields are -0.9bps to 1.91%.

Impeachment news had little impact on markets, with the Senate widely expected to exonerate President Trump after the House voted to impeach. The date of the Senate trial is not yet known with ground rules still being worked out.

Is one the best performing currency pairs consolidating yesterday’s gains to be +0.5% to 0.6888. The Aussie jobs numbers were much stronger than expected with employment rising a sharp +39.9k and dispelling fears that a sharp slowing in employment growth was in stall after last month’s negative -24.8k print. The unemployment rate also dipped a tenth to 5.2% from 5.3%, though the trend overall remains flat with the unemployment rate cycling between 5.2-5.3% over the past eight months. Overall the data while much stronger than expected suggests little to no progress towards the RBA’s goal of full employment – pegged at around 4.5%. NAB continues to expect the RBA to cut the cash rate by 25bps in February with markets around 40% priced.

AUD strength also buoyed the NZD, up 0.5% to 0.6608. Also adding to the positive sentiment was NZ GDP data yesterday which was strong in the quarter +0.7% q/q against the consensus of 0.5% and well above the RBNZ’s MPS forecast of 0.3%. There were though sizeable revisions to history with the annual y/y rate of 2.3% bang-in-line with expectations. The NZD spiked initially and then faded given the downward revisions to history. Nevertheless, the data is another piece of evidence that the economy has picked up steam after a weak H1 2019 with most other indicators also suggestive of a similar story.

A very quiet day ahead with only the US PCE figures of note:

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.