Housing market sentiment rallied as national housing price growth accelerated in the March quarter.

Insight

Equity markets got a boost from the news Trump and Juncker have reached an agreement to halt further tariffs but tech stocks took a dent from the sharp fall of Facebook’s earning results.

https://soundcloud.com/user-291029717/handbrake-on-car-tariffs-facebook-lands-facedown

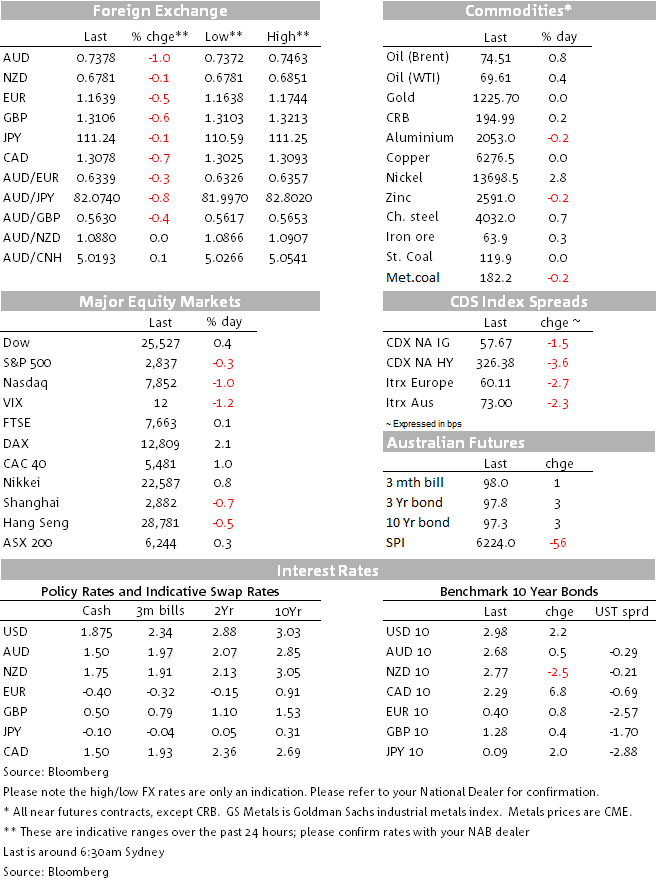

It has been an eventful night with a few macro themes at play. The USD is stronger across the board largely aided by a softer euro courtesy of a dovish ECB and softer CNH amid heightened US-China trade tensions. European equities had a good day following the Juncker-Trump trade truce, but wobbles in the IT sector led by a 19% collapse in Facebook have led the declines in US equities. Front end US Treasury yields have edged a little bit higher in spite of softer US data releases ahead of the 2Q GDP print tonight and the AUD is the underperformer in G10 caught in the US-China crosshairs

While still comfortably confined within recent ranges, relatives to yesterday’s levels the USD is up around 0.50% in index terms against major currencies and a little bit more (ADXY +0.61%) against Asian pairs. Looking at the majors a softer euro has been the key driver for USD strength overnight following an unchanged ECB policy guidance with ECB President Draghi reaffirming the Bank’s commitment to keeping keep rates on hold “through the summer of 2019” ( i.e. after September 2019), effectively dismissing earlier news reports suggesting the wording back in June had been purposely left vague enough to allow for a hike as early as the July 2019 meeting. Draghi also noted that Inflation uncertainty is “receding”, however trade tensions remain a concerns adding that the outcome from the Trump/Juncker meeting was a “good sign” but “too early to assess”.

So after trading to an overnight high of 1.1744 ahead of the ECB meeting, the euro now trades at 1.1643 (-0.71%) close of the midpoint of its 1.15-1.1850 range held since mid-May. Other European currencies followed the euro lower and GBP was not far behind, down 0.59% and currently trading at 1.3108. On Brexit news, EU’s chief negotiator Michel Barnier confirmed market speculation officially ruling out allowing the UK to collect customs duties on its behalf.

The other driver of USD strength and also the cause for AUD’s underperformance over the past 24 hours has been the collapse of the Qualcomm/NXP deal. CNH is the big underperforming Asian currency over the past 24 hours, down 0.94% and to some extent China’s failure to approve the deal has been interpreted by some as a signal of qualitative measures that China has now decided to implement in the escalating trade tensions with the US. So in a background where the US appears to be making some progress on its trade negotiations with Europe and NAFTA, the collapse of the Qualcomm/NXP deal suggest China is aiming for a more hawkish strategy against the US.

So after trading to 0.7463 high following positive sound bited from the Juncker-Trump meeting, the AUD now finds itself as the biggest G10 underperformer, down 1.03%. That said, at 0.7377, the AUD remains yet again comfortably within its 0.7311-0.7484 range held since mid-June.

The NZD has also fallen over the past 24 hours, in sympathy with the move in the EUR and fall in the CNY. The NZD fell from a high of 0.6851 early yesterday afternoon, which was towards the upper end of the trading range over the past month and now trades at 0.6784.

The positive sentiment from the Trump-Juncker agreement was almost immediately dented by Facebook’s earnings results, which were released after the market close. While earnings beat expectations, Facebook said it expected revenue growth to slow and reported disappointing global daily active user numbers. Facebook shares promptly fell 20%, which has dragged down the NASDAQ (-1%) and the S&P500 (-0.2%) overnight.

Amazon reported after the bell, beating EPS expectations, but underwhelm on revenues and revenue guidance. Still in after hours trading the shares are up just under 4%.

The US treasury curve bear flattened overnight with the 2y tenor climbing 1.7bps to 2.688%, in spite of the soft US data releases. The 10y rate trades at 2.974%, a smidgen higher than yesterday’s levels and in Europe 10y bunds close 0.8bps higher at 0.404%.

It has been uneventful and mixed night. Oil prices are a bit higher +0.46%/+0.76%, iron ore is essentially unchanged and gold is down 0.80%

US economic data was mixed, with the monthly trade balance and (volatile) headline durable goods orders weaker than expected, but capital goods orders and shipments stronger. The Atlanta Fed GDPNow estimate for (quarterly annualized) Q2 growth was subsequently revised down to 3.8% from 4.5%. Q2 US GDP is released tonight ( see more below)

EZ: ECB deposit facility rate: -0.4% vs -0.4% exp.

US: Trade balance, Jun: -$68.3b vs -$67b exp.

US: Durable goods orders (m/m%), Jun: 1% vs 3% exp.

US: Capital goods orders – non-defence ex air (m/m%), Jun: 0.6% vs 0.5% exp.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Housing market sentiment rallied as national housing price growth accelerated in the March quarter.

Insight

Growth slowing, but less abruptly than Q1 GDP suggests

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.