Coming in for landing in a heavy cross wind

Insight

Other parts of the world are getting ready for a lockdown that could last a few months.

https://soundcloud.com/user-291029717/hibernation-but-for-how-longunemployment-surge?in=user-291029717/sets/the-morning-call

Coming Up Start up the engine, we’re heavy and rolling, A tank full of gas and the night is young

I don’t know you, don’t care where you’re going, To the Highline or the heart of the sun – Mark Ronson

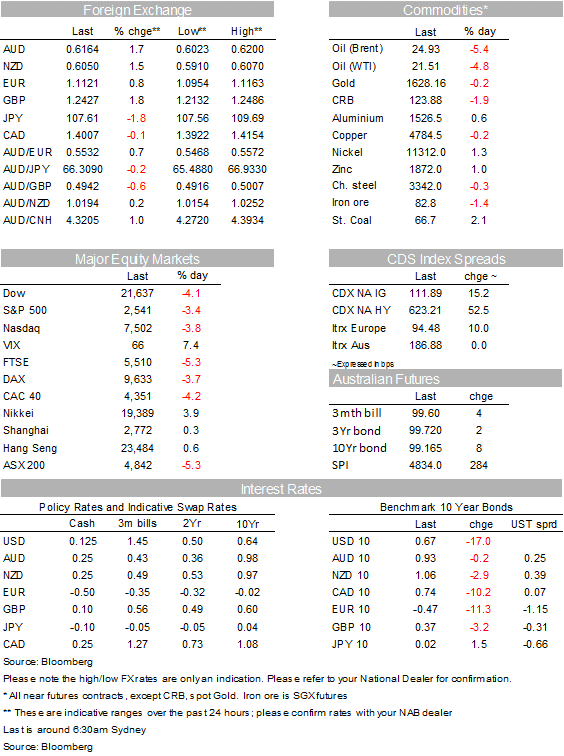

Market uncertainty remains elevated notwithstanding the official signing of a $2trn virus fighting fiscal stimulus by US President Trump. US and EU equities recorded sharp losses on Friday while core bond yields fell with the UST curve bull flattening. Still looking at the week, US equities made double digit gains. The USD was weaker across the board with NOK the only underperformer weighed down by a sharp decline in oil prices. GBP and AUD were the big outperformers.

US equities ended the week with sharp declines after president Trump signed the largest economic relief package in US history. On the day the Dow fell 4.1%, the S&P dropped 3.4%, and the Nasdaq Composite declined 3.8%. Still looking at the week US equities made huge gains, the Dow surged 13%, it biggest weekly gain since 1938 and the S&P 500 climbed 10%, although it is still down around 20% for the year. In a similar pattern European equities collapsed on Friday with the Stoxx Europe 600 Index tumbling 3.3%, but still managed to have a good week (The regional index gain 6.1% on the week).

On Friday the US Congress passed the $2.2trn (10%/GDP) fiscal stimulus package and Trump signed it into law. The package includes $500b in loans and other help for big business (including airlines, states and cities), $350b for small businesses, direct cash payments to low-and-middle income households (by way of a cheque for $1,200 for adults and $500 for children), and enhanced unemployment insurance. When coupled with previous legislation and the fact that the US fiscal measures being taken to combat the virus are worth roughly $2.8 trn or about 13% of 2019 nominal GDP. Importantly too, these numbers are over an above the economic stabilizers that kick in during a downturn, for instance extra healthcare cost and extra unemployment insurance.

So the big question for markets is whether the huge stimulus introduced so far across the globe will be enough to help the global economy withstand the economic shock from the COVID-19 containment measures. To answer this question one needs to know the magnitude of the containment measures and for how long they will be implemented. This is the big know unknown and it suggests markets are likely to remain volatile until this uncertainty is resolved. For instance, the England’s the Deputy Chief Medical Officer suggested lockdown measures to combat the spread of the coronavirus could last for months in the U.K. while in the US National Institute of Allergy and Infectious Diseases Director Anthony Fauci warned that US virus death could reach 200k and emphasised the importance of containment measures. President’s Trump hopes of getting the economy back up running by Easter look a bit unrealistic at this stage.

Xinhua reported that the Chinese Politburo had agreed to increase the fiscal deficit and would allow local governments to increase their issuance of infrastructure bonds, to fund more investment and support the economy. In Canada, the Bank of Canada cut its cash rate by 50bps, to its effective lower bound of 0.25%, in an unscheduled decision on Friday and announced its first QE programme. The BoC will buy a minimum of $5b government bonds per week initially (an annual run-rate equivalent to almost 50% of the current stock of the bond market). The BoC also established a Commercial Paper Purchase Program which will see it buy CP issued by businesses, municipalities and local governments.

PM Morrison has promised a wage subsidy and urged employers not to stand down workers. In a plan that is expected to be announced sometime this week, according to The Australian, “Australians left without work during the coronavirus pandemic are set to gain from an emergency wage subsidy that could be worth $1500 a fortnight”.

The USD fell again on Friday (BBDXY -0.6%), bringing its decline on the week to about 4%, in index terms. This was the biggest weekly decline in the BBDXY since the index was established in 2005, albeit from what was a record (post-2004) high. The fall in the USD has taken place amidst some signs of easing in USD funding pressures, including higher short-end EUR/USD and USD/JPY cross-currency basis swap spreads. USD Libor-OIS remains very elevated at 130bps, but the market prices a sharp retracement over the coming quarters (to 30bps by the middle of December).

The USD was generally weaker against developed market currencies and stronger against emerging markets. The GBP increased more than 2% on Friday, to almost 1.25, despite PM Boris Johnson and Health Secretary Matt Hancock testing positive for COVID-19 and Fitch downgrading the UK’s credit rating to AA- (outlook negative).

The AUD was the other big performer on Friday, gaining over 1.7% and ending the week at 0.6168 ( now at 0.6155). Friday’s gain the in the AUD and GBP for that matter, accelerated around the London fix time suggesting buying could have been driven by month end rebalancing flows. On the week the AUD gained 6.62% and the NZD was not too far behind, up 5.88%. The kiwi now trades at 0.6035.

The Euro gain around 1% ending the week at 1.1132. Over the weekend the Italian and Spanish PMs leaders amped up their criticism of the European Union for being slow and failing its hardest-hit members in the hour of their greatest economic need. In an interview with Il Sole 24 Ore, Italian PM Conte openly questioned the “raison d’etre” of the bloc if it cannot handle this crisis appropriately, Conte and Sanchez joined French President Emmanuel Macron in advocating a hefty joint EU response, something Northern European countries oppose.

The CAD and NOK underperformed amidst a 5% fall in crude oil prices as Russia and Saudi Arabia show no signs of compromising in their standoff over oil supply.

Central bank bond buying is starting to leave its imprint on the government bond market, with global longer-term yields falling significantly on Friday. The 10-year Treasury yield fell 16bps on the session, to 0.68%, while the German 10-year bund yield was 11bps lower, to -0.47%. The very short end of the US government curve (out to one-year) is mostly trading with negative yields, probably reflecting the amount of cash being parked in government-only money market funds. The Federal Reserve will cut back its purchases of US Treasuries from Thursday to $60b per day, from $75b previously.

There were further signs of a thawing in the global investment grade (IG) credit market on Friday, with more primary market issuance taking place. On the week, there was a record $109b of US IG new issuance and around €75b in Europe, with corporates and banks rushing to take advantage of the reopening of the primary market to raise cash. The primary market for high yield remains shut. Despite strength in global credit markets the preceding night, NZ corporate and bank credit spreads were flat-to-wider on Friday and this market remains extremely strained.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Coming in for landing in a heavy cross wind

Insight

Conditions again fell in Q2, but confidence stabilising

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.