Online retail sales growth slowed in May following a fairly strong April

Insight

With nothing concrete to go on, markets continue to factor-in optimism over the US-China trade talks.

https://soundcloud.com/user-291029717/high-hopes-and-a-gentle-turning-point?in=user-291029717/sets/the-morning-call

How many times, Did we give up, But we always worked things out

… But baby it ain’t over ’til it’s over – Lenny Kravitz

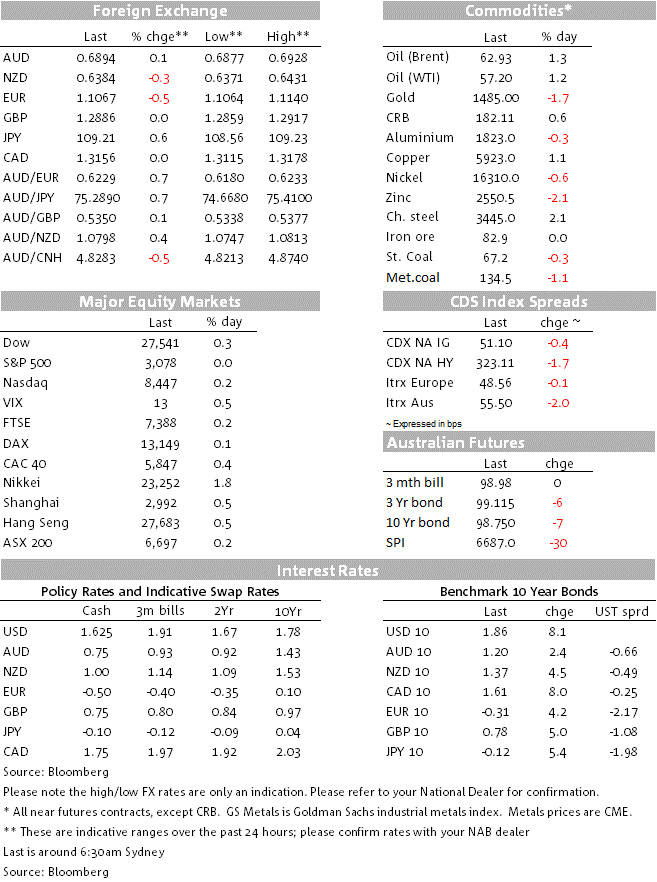

Media reports during our day yesterday suggesting the US was considering the removal of China tariffs in order to strike a Phase 1 deal boosted market sentiment. Then overnight a better than expected US ISM non-manufacturing added to the positive vibes. UST yields have led a decent rise in core global yields while the bear steepening of the UST curve also reflects an improvement on the US economic outlook. Higher UST yields have boosted the USD across the board with the AUD the only G10 outperformer. European equities closed higher while US equities consolidated recent gains.

During our session yesterday a new twist in the story was sparked by an FT article suggesting “Trump administration officials are debating whether to remove some existing tariffs on Chinese goods as a concession to seal a partial deal”. The FT reported that China was asking for the US to eliminate tariffs on $110bn in goods that were imposed in September and lower the 25% tariff rate imposed last year on $250bn of goods. This demand goes further than just suspending the fresh tariffs due mid-December on $160bn of goods.

While the US consideration of tariffs removal is good news, the big question is what does the US get in return? Media reports suggest that the US would expect more provisions on intellectual property protection for US companies, guarantees on the scale of China purchases of US agricultural products and the need for President Xi to sign the deal somewhere in the US.

The latest news have added further fuel the notion that a US -China Phase 1 trade deal looks imminent. The final decision, however lies with President Trump and what is also unclear is whether China’s position is on the removal of tariffs is all or nothing. It is clear now that the US will need to remove some tariffs in order to strike the deal, but if China doesn’t give more concessions in exchange, President Trump runs the risk of being criticise as “going soft” on China ahead of the election.

Our assumption in our FX forecast is that we won’t see a material roll back on existing US tariffs on Chinese imports at this stage. This means that USD/CNY is likely to trade in a narrow range just above the 7 mark while the AUD/USD is not seen breaking sustainably back above 0.70 through H1 2020 at least. But if we were to get a full rollback of existing of tariffs as part of a Phase 1 deal, then the positive impact on the global growth outlook and pro-growth risk sensitive currencies such as the AUD and NZD could be significant.

So on this score it is interesting to note that overnight USD/CNY traded below the 7 level for the first time since August. The strength in the CNY was driven by the optimistic view that President Trump might actually agree to roll back some tariffs, notwithstanding the fact that earlier in the session the PBoC offered 1-year MLF at 3.25% from 3.3%, first reduction since Fed 2016 and a possible harbinger of a lower Loan Prime Rate before year end.

The US-China trade positive vibes and a stronger CNY was a factor behind the move higher in core global bond yields over the course of yesterday, but then the move up in yields got an additional boost following the release of a better than expected US ISM non-manufacturing index. The headline number rose to 54.7 in October from 52.6 in September, well above the 53.5 expected. Importantly too, the sub-indices also painted a positive picture with a decent rebound in the new orders and employment components. The recovery reduces fear that the recession in the manufacturing sector is spilling over into the services sector. In other economic news, the US trade deficit was in line with expectations, falling to a 5-month low of $52.5bn. The data highlight the impact of the trade war – in the 9 months to September US imports from China fell 13.5% while exports fell 14.6%, seeing a narrowing of the US trade deficit to China from $307bn to $266bn.

US rates rose across the curve, with 2-year Treasuries up 4bps to 1.62% and 10-year Treasuries up 8bps to 1.86%, extending the significant bond market sell-off and curve steepening evident over the past month or so. Traders of the 10-year rate will be eyeing the September high just above 1.90%. A break of that level would ease a path up to the 2% mark. To the extent that rising rates reflect a more optimistic economic outlook – a possible trade war truce and the message from the more positive yield curve – US equities continue to be well supported. Previously a 35bps sell-off in Treasuries might have seen equities fall substantially, but the S&P500 made a fresh record high yesterday and today it looks set to end the day close to unchanged.

The rise in UST yields has supported the USD with the greenback making gains across the board. The DXY index is up 0.46%, reflecting declines of around 0.50% in European currencies ( EUR now at 1.1068) with similar losses recorded in safe haven currencies such as the CHF and JPY. USD/JPY now trades at ¥109.20 with the pair again reflecting its high degree of sensitivity to movements in 10y UST yields courtesy of the BoJ’s Yield Curve Control Policy.

The AUD is the only G10 currencies that has managed to outperformed the USD, up 0.13% relative to this time yesterday’s levels. The AUD traded to an overnight high of 0.6928, before reversing course as higher UST yields boosted the USD. The AUD now trades at 0.6894. Yesterday the RBA left its policy rate unchanged as expected and retained the message that the economy is on a gentle (upward) turning point. That said we would attribute the move up in the AUD to the decline in USD/CNY below 7 rather than the RBA.

The NZD also succumbed to the USD strength and the pair now trades at 0.6384, 0.14% lower compared to levels 24 hours ago. In overnight news, the GDT dairy auction price index rose by 3.7%, above our expectations for a 1-3% gain, driven by a 3.6% gain in whole milk powder and 6.7% gain for skim milk powder and yesterday QV house price data showed annual house price inflation nudging higher.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.