Online retail sales growth slowed in May following a fairly strong April

Insight

The lift in equities appears to be a case of ‘buy the dip’ with an absence of any positive news flow apart from the very second-tier Empire Fed Manufacturing Survey which surprised sharply to the upside.

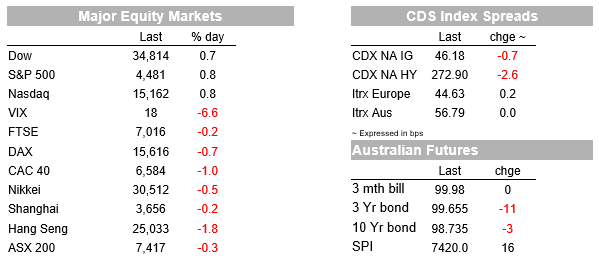

US equities rose overnight with sentiment stabilising after falls in Asia (Nikkei -0.5%; Hang Seng -1.8%) and Europe (Eurostoxx -1.1%). The S&P500 rose 0.8% with energy again outperforming (energy sub-index +3.8%) on higher oil prices (Brent +2.5% to $75.45) after a larger than expected US inventory drawdown amid ongoing production disruptions from recent storm activity. To your scribe the lift in equities appears to be a case of ‘buy the dip’ with an absence of any positive news flow apart from the very second-tier Empire Fed Manufacturing Survey which surprised sharply to the upside (34.3 vs.17.9 expected and 18.3 previously). News out of China continues to be weak with the monthly activity indicators missing and woes around Evergrande building.

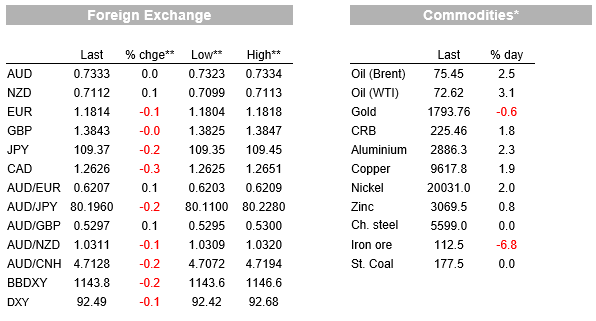

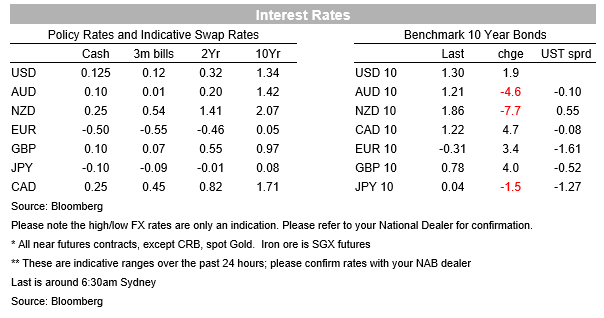

As for yields, they rose with hotter than expected CPI inflation from the UK and Canada, cementing expectations for hikes in 2022. The US 10yr is up 1.9bps to 1.30%, almost entirely reflected in the implied inflation breakeven which is up 1.6bps to 2.35%. The curve steepened with 2s10s steeper by 1.4bps. Yields in the UK (10yr +4.0bps to 0.78%) and Canada (+4.7bps to 1.22%) rose more given the CPI beat. FX in contrast has been quiet with the USD DXY -0.1%, while JPY gained with USD/Yen -0.3%. There was little movement in either EUR (-0.1% to 1.1814 ) or GBP (+0.0% to 1.3843). The lift in energy prices saw commodity currencies outperform with USD/CAD -0.3% to 1.2626 , USD/NOK -0.8% to 8.5797, and AUD was little changed at 0.73.

First to the UK and Canadian CPI figures. Core UK CPI inflation was higher than expected at 3.1% y/y against 2.9% expected. The larger than expected increase in core appears to have come from a huge 4.9% m/m rise in used car prices. The CPI beat reinforced market expectations of rate hikes in 2022, pricing a 15bps lift in Bank Rate to 0.25% in May, followed by a 25bps lift in November. Recall that last week Governor Bailey told Parliament that he was one of the four MPC members who thought that the minimum criteria for tighter UK monetary policy had been met even if he didn’t consider there were sufficient grounds to push for immediate tighter policy. Canadian CPI figures also came in hotter with headline at 4.1% y/y reaching a 18 year high, while the average of the core measures pushed up to 2.6%. Overall the data points to the Bank of Canada

tapering of asset purchases next month and markets price the first rate hike in Q3 2022.

US data was mixed with the Empire Fed Manufacturing Survey surprising sharply to the upside for no apparent reason at 34.3 against 17.9 expected. Some attribute the stabilisation in sentiment during the US session to the beat, though it is very second-tier and volatile. Industrial Production figures were also released, missing marginally at 0.4% m/m against 0.5% expected. Manufacturing output also missed at 0.2% m/m against 0.4% expected. More top-tier data comes out tonight with Retail Sales for August where expectations are not high given the recent sharp fall in consumer sentiment in response to the delta outbreak and possible impacts from recent storm activity (see below for details). The recent storm activity is also one reason for the rise in oil prices with Brent +2.5% to $75.45. The US EIA reported a sharper inventory drawdown of 6.4m than the consensus of 3.5m with Gulf Production not yet fully back online.

On the negative side, Chinese data and headlines continue to be of concern . The monthly activity figures yesterday all missed to the downside with a very sharp miss in retail sales at 2.5% y/y against 7.0% expected, as well as in industrial production at 5.3% y/y against 5.8% expected. Measured in month-on-month changes, retail sales only rose 0.2%, after a 0.2% drop in July, marking the weakest two-month period since the lockdowns of early 2020. While the delta outbreak in late July is the main culprit and which was brought under control by mid-August, the latest outbreak in Fujian province (50 new cases yesterday) will no doubt dampen activity in September and limit the extent of any bounce. The regulatory crackdown also threatens to slow the domestic growth momentum with many China commentators seeing a pivot away from maximising growth, to social order and stability. Finally the Evergrande Group is proving to be a greater headwind on the property sector with China telling banks not to expect interest payments due next week on bank loans. Evergrande is still discussing with banks the possibility of extending payments and rolling over some loans. Default risk on China’s other listed developers is also lifting.

Finally in Australia, consumer sentiment rose 2.0% m/m in September to 106.2 in the W-MI survey. Notably sentiment rose more sharply in NSW (+5.3%) as re-opening hopes build with NSW’s re-opening plan tying a substantial easing of restrictions to achieving 70% full adult vaccination. Consumer confidence overall has been very resilient to the lockdowns seen in NSW, VIC and the ACT. The rise suggests the low point in confidence may have passed with a relatively shallow trough of 104.1 compared to the sub-100 level of 75.6 in April 2020. This same pattern is replicated in the unemployment expectations question suggesting there has been little scaring in the labour market due to the prolonged lockdowns. With consumer sentiment lifting and business confidence in also resilient, it is likely activity will rebound sharply once restrictions ease.

Employment data the biggest focus domestically, while offshore US Retail Sales takes the top billing given the recent sharp fall in consumer sentiment. Details below:

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.