Robust growth for online retail sales observed in June

Insight

Lower US bond yields and softer US dollar lift AUD back above 0.64

Harmful elements in the air, Symbols clashing everywhere – Siouxsie and the Banshees

This Siouxsie punk-era classic is actually about skinheads regularly invading her local Chinese restaurant and beating up the Chinese locals but seemed apt in the context of the what looks like an impending default by Hong-Listed Country Garden, China’s largest property developer.

Financial markets have remained remarkably sanguine, with global equities higher – the VIX is off almost a point – and the US dollar softer in the face of the still unfolding human tragedy in Israel and Gaza. Lower US Treasury yields are more to do with scaled-back expectations for further Fed tightening than safe-haven support on Middle-East events, and oil price are easier. The exception is gas, with European benchmark prices up another 15% to bring the rise since Hamas’ assault on Israel to 35%. This latest rise is on a gas pipe leak in Finland, where (Russian) sabotage is suspected. News of potential budget-deficit expanding fiscal stimulus in China has offered both the CNY and AUD (very) modest support, though little beyond the effect of generalised USD slippage

The FT reports Finland is investigating whether sabotage caused a leak in a (77km long) Baltic Sea gas pipeline and a break in a data cable between the Nordic country and Estonia. Sauli Niinistö, Finland’s president, said the damage to the gas pipeline and data cable was due to “external activity” but that the precise cause “is not yet known”. Finland’s foreign minister Elina Valtonen later on Tuesday said the two undersea links “have probably been damaged on purpose”. The potential sabotage echoes last year’s explosions in the Baltic Sea, which destroyed the twin Nord Stream pipeline that connected Germany to Russia (Finland shares a 1,300km border with Russia). The impact on gas prices comes just a day after Chevron was reportedly instructed by Israel’s Ministry of Energy to shut production at the Tamar natural gas platform in the eastern Mediterranean.

As noted above, Country Garden, China’s largest private developer, has warned of a potential default on its international debts in a significant blow to the country’s embattled property sector. The company, which has about $200bn in liabilities and close to $10bn in dollar-denominated debt, said in a statement to the Hong Kong stock exchange that it had missed a due payment of HK$470mn ($60mn) on some of its debts and also expected it “will not be able to meet all of its offshore payment obligations” when they are due. “Such non-payment may lead to relevant creditors of the group demanding acceleration of payment of the relevant indebtedness owed to them or pursuing enforcement action,” the company said on Tuesday.

Incoming Fed speak includes Minneapolis Fed President Neel Kashkari has just popped up on the wires, describing the recent rise in 10-yar yields ‘[perplexing’ but offering up higher growth expectations (but not, he notes, higher inflation expectations) and rising US debt issuance as possible explanation. Earlier Tuesday, Federal Reserve Governor Christopher Waller (erstwhile hawk) said the US central bank is determined to bring inflation back to its 2% target in a speech that mostly avoided the current state of markets or monetary policy. “We have reaffirmed this numerical goal repeatedly since 2012, and, in tightening monetary policy since early last year, we’ve made clear that we’re determined to bring inflation down to 2%.” Waller. The majority of Waller’s remarks were about the legacy of the economist Bennett McCallum, whom the conference was named after. He didn’t comment on the near-term outlook for interest rates.

In other central bank speak, Bank of France governor Villeroy repeated comments from last week that he sees no justification at present for the ECB to resume monetary tightening and says it should now keep its main rates at a plateau for as long as necessary. He did say though the central bank need to be vigilant oil prices (no mention of gas) amid the conflict between Israel and Hamas,.

Bloomberg reported yesterday evening our time that China is considering raising its budget deficit for 2023 as the government prepares to unleash a new round of stimulus to help the economy meet the government’s annual growth target, according to people familiar with the matter. It says policymakers are weighing the issuance of at least 1 trillion yuan ($137 billion) of additional sovereign debt for spending on infrastructure such as water conservancy projects, said the people, asking not to be identified discussing a private matter. That could raise this year’s budget deficit to well above the 3% cap set in March, one of the people said. An announcement may come as early as this month, another person said, though deliberations are ongoing and the government’s plans could change.

Economic news has been scant. In the US just the NFIB survey (Small Business Optimism) which slipped to 90.8 from 91.2, a l (91.0 expected). The earlier (Friday) release of its Hiring Plans index printed at a positive 18%, up from 17% to its highest reading in four months. Updated IMF global forecasts showed little revision to its global growth outlook, with GDP projected to slow from 3.5% last year to 3.0% in 2023 and 2.9% in 2024, well below the 2000-2019 average of 3.8%. There was more change to its inflation outlook, with a steady decline from 8.7% last year to 6.9% in 2023 and 5.8% in 2024, with the forecast for 2023 revised up 0.1ppt and for 2024 up a chunky 0.6ppts. Inflation is not expected to return to target to 2025 in most countries, the IMF reckons, underscoring the need of central banks to keep policy tight.

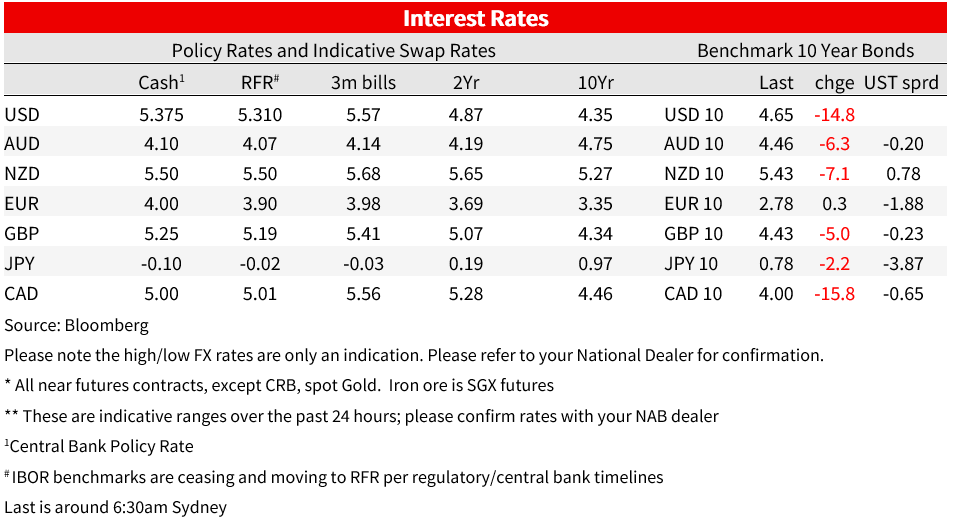

In markets, US Treasuries are showing some of the biggest movement. Treasuries opened sharply lower in yield terms at Tuesday’s Tokyo market re-open after Monday’s Japan and US holiday, 10s at +/- 4.65% from 4.80% at Friday’s post-US payrolls data close and have pretty much stayed there ever since. (currently 4.66%, down 15bps, with 2s down 10bps to 4.98%). We attribute the fall since late last week more to commentary from a number of Fed officials (Daly, Logan, Jeffries) highlighting the tightening of US financial conditions since the last (Sep 20) FOMC meeting as doing additional tightening work for the Fed. This has seen market-implied pricing for another Fed rate hike out of the combined November and December meeting slip from more than 40% last Friday to currently only about 15%. Of course, there is some circularity here – financial conditions have eased back precisely because of the Fed’s reference to them as constraining the need for more tightening, though compared to where they were as of the Sep 20 FOMC meeting, conditions are still somewhat tighter (e.g., 10s were 4.40% back then).

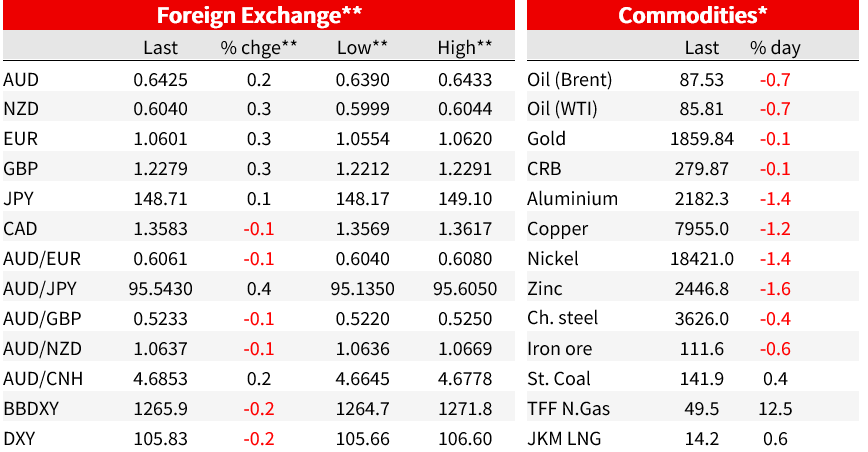

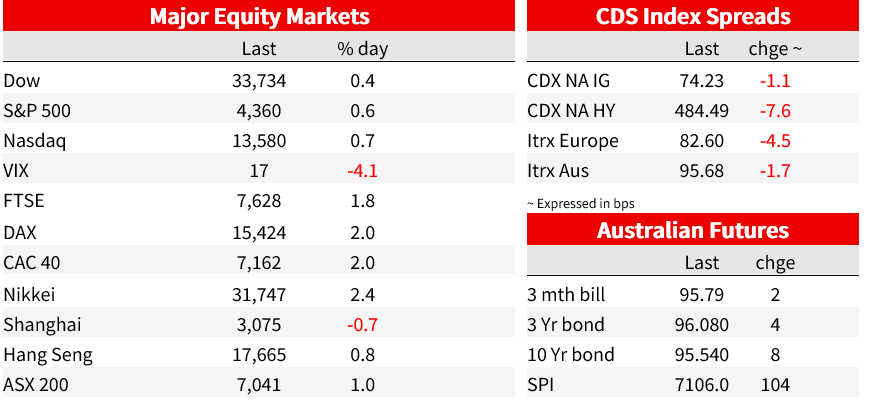

In currencies, the USD is softer across the board bar a marginally weaker USD/JPY. Responsibility lies with the pull-back in US Treasury yields – beyond those seen elsewhere, Europe especially, where Bunds ended their day unchanged, gilts -5bps – and improved risk sentiment. The S&P500 and NASDAQ are currently +0.6 and 0.7% respectively. The DXY USD index is off 0.25%, with GBP, EUR, AUD and NZD all +/- 0.2% firmer. AUD has not, therefore, derived any additional benefit beyond USD slippage from the above-mentioned China fiscal stimulus report – nor too the strength evident is yesterday’s NAB survey of Business Conditions and Confidence, albeit the latter remains in stark contrast to still very weak Consumer Confidence. At least AUD/USD has recovered from the latest fall-back below 0.64 (high of 0.6433 Tuesday).

Coming Up

Market Prices

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Robust growth for online retail sales observed in June

Insight

Coming in for landing in a heavy cross wind

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.