A private sector improvement to support growth

Insight

US stocks have fallen markedly since the Fed meeting yesterday, with the dollar also taking a hit and the yield curve flattening a little.

https://soundcloud.com/user-291029717/more-than-a-fed-response-equities-and-dollar-down-curve-flattens

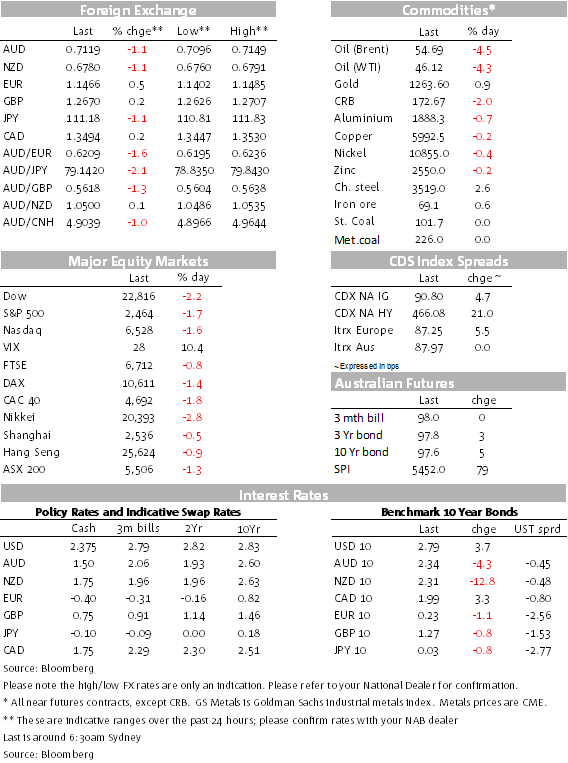

It’s another sea of red, the US main board indexes down in size again, led by the FAANG stocks though the market has tried to rally in the last hour or so. The Eurostoxx600 index declined by 1.45%, led by banks. A delayed reaction to the Fed? A little perhaps, as the 2-year Treasury yield has pushed up on net by perhaps 1-2bps since before yesterday morning’s FOMC announcement. (The Treasury curve has flattened with longer term yields lower on net since the FOMC.) A marked negative stock reaction to the FOMC would normally have been associated with an even higher dollar (maybe it has hit a wall), but the USD has lost some grip and is down pretty much across the board overnight. US energy stocks are also under-performing after yet another sizeable decline in oil prices. Congress and the Administration remain in a stand-off over funding for the Wall, Congress not giving the President money for that funding, unhelpful for market sentiment.

The USD has been on the back foot in the overnight session, losing ground across the board. The DXY is down 0.66%, a bigger beneficiary among the majors being the yen. It’s been nothing to do with yesterday’s Bank of Japan meeting when Governor Kuroda said that the BoJ has more tools for adding stimulus if needed, adding that it’s no problem if government bond yields fall into negative territory, so long as the move reflects economic fundamentals and yields remain within the BOJ’s target range. 10 year JGBs yesterday closed at 0.027%, within sight of testing the tolerance of the BoJ’s drawn at a zero 10-year JGB rate target.

Emphasising the importance of yields, the Swedish Krona took top spot after the Riksbank told a bold step and lifted rates for the first time in seven years, from -0.50% to -0.25%. The Krona is up 1.43% since late APAC time yesterday. While most analysts expected rates to remain on hold, a sizeable proportion (10 of 24 in the Bloomberg survey) looked for a hike, so not a total surprise. Swedish stocks though fell 2%, a somewhat larger fall than European counterparts. On the other side of the ledger, the CAD has not made any ground against the soggy USD.

The NZD has managed to make up some lost ground overnight while the AUD has poked its head above 0.71, after getting a mixed response from stronger than expected employment (if all part time this month) but higher than expected unemployment, dragging the Aussie lower yesterday afternoon before a muted recovery overnight. It’s trading below its overnight highs around 0.7140 as we approach year end.

The Banks of England met amidst extreme Brexit uncertainty (noted as having “intensified considerably”) and it was no surprise that it left rates on hold. Meanwhile the UK Society of Motor Manufacturers and Traders warned of the impacts of a crash out Brexit, not in months or days but in hours, warning of just-in-time major disruptions, tariffs, job losses and more. UK retail sales in November shot the lights out, up 1.2% against expectations of a 0.2% rise though the CBI Retailers survey for December slumped to -13 from +19, likely fearing the worst ahead.

In the US, the Philly Fed survey was somewhat softer than expected at 9.4, down from 12.9 and lower than the 15 expected. Jobless claims remained low in the December payrolls survey week at 214K from 206K and the 215K consensus. The Leading index in November rose was a little stronger than the flat result tipped, up 0.2% as real economy measures such as orders and building permits more than outpaced the drag from the stocks component.

The main mover was again oil on the downside, WTI trading around $46 and Brent at around $54.50, oil off north of 4%. OPEC is disclosing further transparency around the country details of the 1.2mb promised supply cut. Base metals were off smalls, LME copper down 0.25%, gold higher, getting support from the softer USD.

Chinese iron ore and steel rebar prices were higher yesterday as the PBoC announced measures to support lending to micro and private businesses through a dedicated lower-rate bank lending facility.

European bond markets were generally stronger, though Treasury yields are somewhat higher, 2s up 2.3bps while 10s are up 3.74bos to 2.79% as stocks attempt a late comeback.

This is the last Markets Today for this year. There will be no update now between Monday 24 December and the week beginning 7 January, though we will be publishing a brief bullet style note in the new year. We wish all our readers (and listeners to the Podcast) all the best for the festive season and the New Year.

There’ll be a special podcast on Monday looking back at 2018 and looking forward to 2019. There’ll be no update between Monday 24 December and 7 January. We wish all our readers and listeners to the Podcast all the best for the festive season and the New Year.

A private sector improvement to support growth

Insight

Online retail sales growth accelerated 1.1% in April

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.